The outbreak of Covid-19 presents a once-in-a-century global public health crisis. The necessary precautionary health measures taken by both the Irish and international governments to restrict the movement of people has undoubtedly had adverse implications for the economy and the housing market.

Projecting the total economic fallout and impact on the Irish housing market from the lockdown and the restrictive measures that will inevitably be in place immediately afterwards is incredibly challenging.

Furthermore, the scale of the crisis is still unclear and remains dependent on the length restrictive measures are in place both at home and abroad. Inevitably though, the impact will be wide-ranging, with price performance, transaction activity and construction output all impacted in the short term to a greater or lesser extent.

Prices held firm at the end of the first quarter, but there is some downside risk while the economy and labour market adjust. In terms of sales activity, early indications suggest some degree of a slowdown at the end of the first quarter, albeit minimal. This will become more apparent in quarter-two data with the full extent of the lockdown physically restricting the sales process. An increase in rental stock in urban areas was also noted in the immediate weeks after lockdown.

Policy measures

Once normal economic service begins to resume, it is imperative that the Government implements policy measures designed to boost activity. This is especially pertinent in the construction sector given the housing crisis will not have eased, but rather likely deteriorated further. Indeed, the 21,000 new homes built in 2019 represented an estimated shortfall in the region of 12,500 to 18,500, with this shortfall likely to expand further again this year given reduced output levels.

Our latest analysis looks at how residential values and transaction activity are expected to respond to the unfolding Covid-19 pandemic.

In the run-up to the pandemic, the market witnessed a promising opening quarter with second-hand house prices stable at 0.1 per cent, a positive outcome following six months of price deflation. However, the opportunity for this bounce to gain a foothold was delayed by the onset of the Covid-19 health pandemic, which has thrust the residential market into unknown territory.

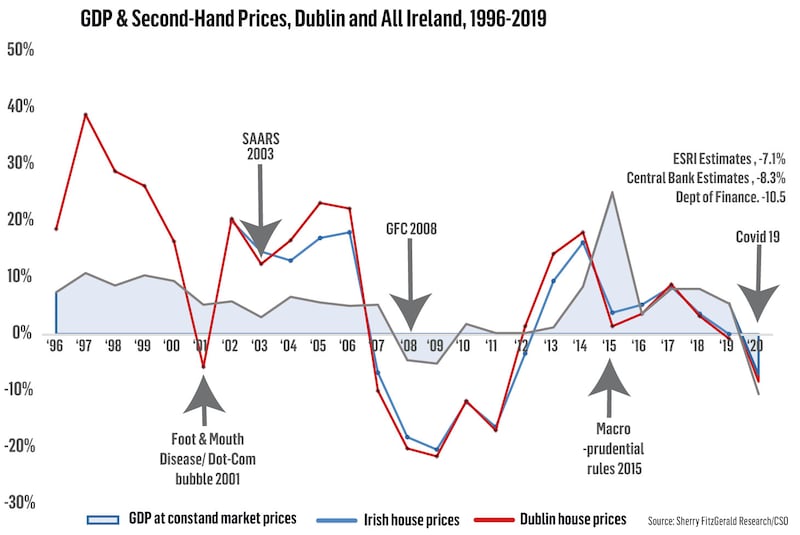

The graph here depicts previous shocks to the economy such as foot-and-mouth disease and Sars and the resultant impact on mainstream house prices. Unlike Covid-19, these shocks were not necessarily in isolation and other factors were at play. Covid-19, as an economic shock, is unprecedented in both scale and nature.

Thus far, there has been little data released on key residential-related indicators to judge the true impact of Covid-19 on the residential market. As such, projecting the future price performance is incredibly challenging. House prices could soften in the short term. However, the precise level of this contraction is highly uncertain, given the many unknowns surrounding the future path of the virus.

At this juncture, progress has been made in suppressing the spread of the virus, but the lockdown measures will remain largely in place until at least the middle of May. If the economy reopens relatively quickly after this, and the structural damage to the economy is limited, the contraction in values could be short-lived.

Favourable policy actions by the Government to date, such as a period of moratorium on mortgage payments, will have helped shield households and reduce the risk of mortgage defaults, which in the most recent housing crisis was a catalyst for house price depreciation. In addition, the introduction of a series of income-support measures such as the Covid-19 income support scheme and the Covid-19 pandemic unemployment payment of €350 per week will have helped maintain income streams and pent-up demand in the meantime, facilitating a swifter recovery in house values.

That said, there are downside risks, the major one being the unknown trajectory of the virus and a worst-case scenario of a second outbreak. Other notable downside risks include a delay in the recovery of the economies of our key trading partners. Ireland, as a small, open economy, is heavily reliant on international trade and therefore slowdowns in international economies have an impact on Ireland’s economy. In the event that the virus persists, resulting in a prolonged period of lockdown measures and economic disruption, we would expect a more protracted impact on prices.

Slowdown

Turning to transactions, early indicators suggest some slowdown in sales at the end of March, in line with the implementation of social restrictions; however, they were not particularly significant. A reduction in sales activity will inevitably become more pronounced as quarter two progresses.

Again, the severity of this will be dependent on the economic impact of the crisis. However, some disruption is already evident in lead indicators. Second-hand home listings were down 40 per cent nationally in March, year on year, with further decreases inevitable in the coming months. This will impact the sales pipeline for the latter part of the year.

With so many unknowns as to the timing and nature of the loosening of lockdown measures, it is difficult to forecast with any accuracy the impact that Covid-19 will have on the overall volumes of activity. However, taking into consideration what is known at the time of writing, there is a strong possibility that overall sales in 2020 will be down by a minimum of 25 per cent in the full calendar year.

Marian Finnegan is an economist and managing director of Sherry FitzGerald Residential