The first five years of Mary’s mortgage were uneventful. She bought her house with her partner in 2010, in the teeth of the recession. Despite the economic headwinds, both were working. With two children, they wanted a permanent place to call home.

But in 2015, her partner, who drives a motorbike for work, was in a serious accident when another driver performed a dangerous U-turn. “He crashed straight into him. He had multiple broken bones and was very seriously injured.”

Without sick pay, Mary – working part-time – was the only earner. The family quickly slipped into mortgage arrears. Then the phone calls from the bank started. “It got to the stage where I didn’t answer my phone,” Mary recalls. Soon they were €10,000 in arrears.

The pressure was building. “The bank was like ‘when will you pay, what are you paying, when will you clear the arrears?”

The accident happened in autumn. Soon, the demands of children’s birthdays combined with Christmas. “You can’t turn around and say you can’t have a birthday, or Santa can’t come,” she says. Her family helped out, but the financial pressure continued.

The family fell behind on credit card payments, then electricity and gas bills – ultimately they ended up going to a neighbourhood loan shark to make ends meet. When Mary’s family found out, they cleared the debt owed to the loan shark. But the “dark times” continued after her family bailed her out.

“It compounded my depression more, because I felt like I was a big burden on my family,” she says.

Borrowers like Mary (not her real name) have been at the centre of a public debate for almost a decade. Should they face foreclosure, or forbearance? What can they pay, and what should they pay? And what is the reality of living with debt, in the shadow of repossession – and how real is the threat of losing your home?

Scale of the problem

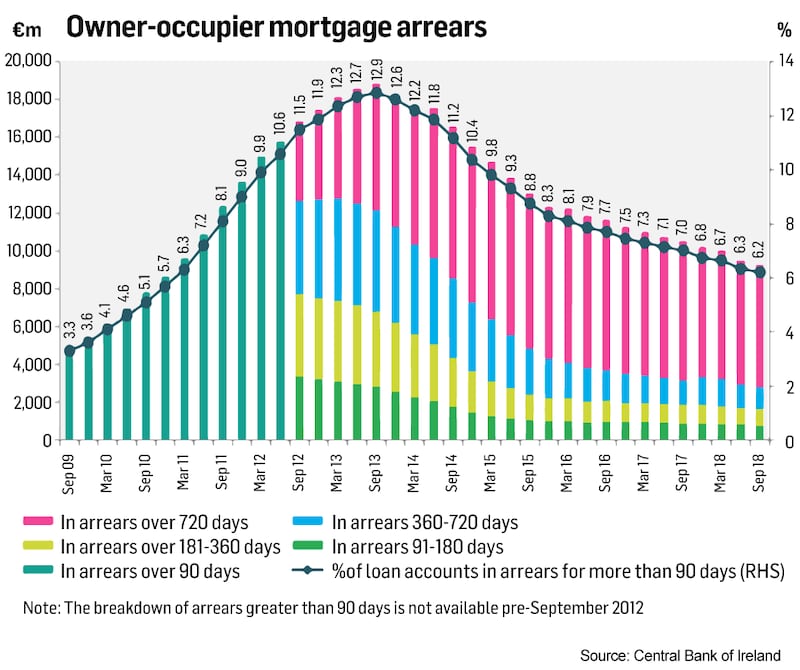

Dealing with a non-performing mortgage on a family home, and the accompanying prospect of repossession by a lender, is a daily reality for 64,510 borrowers, according to the latest statistics from the Central Bank of Ireland.

This accounts for a little less than 9 per cent of all mortgages secured on what are called principal dwelling houses – more commonly known as owner-occupier mortgages, or family-home loans.

The problem of toxic debt is still front and centre for Irish banks, who are a major outlier compared to their European peers. At the end of 2017, just under 11.5 per cent of Irish loans were classified as non-performing, compared with an EU average of less than 4 per cent.

One factor limiting repossessions is the glacial nature of putting these cases through the courts

While some research has suggested that borrowers defaulted at a higher rate when they expected that the likelihood of repossession was lower, experts say that the main cause is simple. Dr Padraic Kenna of NUI Galway recently edited a comparative study of evictions across Europe. He believes discussion of strategic default is "a diversion".

“The reason for arrears is, by and large, people lost their incomes,” he says.

Hence, as the economy has recovered, more people have been able to keep to the terms of their restructured mortgages, or, even better, clear the arrears on their accounts.

There has been significant progress tackling the size of underperforming mortgage loans in recent years. Statistics from the Central Bank show that the level of family-home mortgages in arrears of 90 days or more peaked at 12.9 per cent in September 2013 and has steadily declined to its current level of 6.2 per cent since then.

When it comes to owner-occupied mortgages, the majority of the improvement has been through adopting what the Central Bank call “cures” – split mortgages, term extensions, or “arrears capitalisation”, where unpaid amounts are added to the total figure owed.

However, this downward march has not solved all problems. There are still more than 28,000 borrowers in arrears of 720 days. While that figure is declining, progress has not been as impressive.

This is where the policy headaches begin. These borrowers make up 43 per cent of all accounts in arrears, but the vast majority – 90 per cent – of money owed. Around €2.4 billion is owed by this cohort, weighing down on the balance sheets of Irish lenders – as well as the householders who owe it.

"For us the problematic category is someone in arrears for two years or more. They're chronic, many have been in arrears for more than five years," says Paul Joyce, a senior policy analyst with the Free Legal Aid Centre (Flac).

What to do about these mortgages sharply divides opinion. One former policymaker, who worked on early responses to the emerging problem of toxic debt during the crash, is uncompromising. “If you’re 720 days plus, you’re gonzo; it’s not happening. You should be foreclosed and resold. It’s a completely untenable situation. There is a point where you have to say ‘this is insurmountable.’”

Joyce disagrees. “You hear people saying it’s time to get on with it – I fundamentally don’t agree,” he says. “There’s a lot of children and other dependents caught in the crossfire of financial difficulty, and suffering from all that brings.”

Whatever the right course of action, logic would suggest that a country with such a vast pool of underperforming mortgages would see high levels of repossessions as lenders move to enforce their security – the much-talked-about “tsunami” of repossessions.

But again, Central Bank data suggests that repossessions are not very high.

Since March 2012, proceedings have been issued in thousands of cases, but only a little over 8,000 properties have actually been taken into possession. Why?

Holding back the tide

One factor limiting repossessions is the glacial nature of putting these cases through the courts.

Perhaps more than anyone, David Hall has risen to national prominence over the issue of toxic debt. As founder of the Irish Mortgage Holders Organisation, he has been predicting a tsunami of repossessions for longer, and more loudly, than anyone else. He says the courts have been holding back the tide.

“That’s the only thing that’s keeping people in their homes, not the Government [but] court reluctance to execute repossession orders,” says Hall.

Since its inception, the ISI has instituted less than 8,000 debt solutions

In his recent study of the Irish mortgage market, NUIG’s Padraic Kenna said he found that “the big bulk of cases are stuck in the courts system, and they’re being sent round and around and looking for adjournments”.

He estimates that there could be up to 20,000 mortgage holders in this legal limbo. Paul Joyce of Flac says county registrars, who handle civil bills for repossession, practise a sort of ad-hoc forbearance, acting as an intermediary between borrowers and lenders.

“The general approach is to see what’s being paid . . . whether the borrower has availed of assistance, and trying to see whether a payment arrangement can be put in place to satisfy the lender,” he says.

In a 2017 report by Competition and Consumer Protection Commission, one lender said that it takes between 18 and 72 months to repossess a home in Ireland, compared with nine-12 months in the UK, and six months in Northern Ireland and Denmark.

A number of State schemes have also stemmed the flow. But the numbers using these schemes suggest they may struggle to tackle the problem of long-term arrears.

In recent years, the Government undertook a protracted reform of the mortgage-to-rent system, which sees borrowers give up ownership of their homes and become social-housing tenants in the same property. But only one new operator has come to market.

Paul Cunningham, who heads up that company – Home for Life – estimates that when the numbers in long-term arrears are combined with those in temporary forbearance arrangements, there could be up to 50,000 borrowers in difficulty.

Cunningham thinks the mortgage-to-rent scheme could be a solution and a good one. But ultimately, he estimates that in its current form it can provide for only around 10,000 borrowers.

There are options beyond mortgage-to-rent, he points out, such as personal insolvency and bankruptcy, part of a wide suite of tools administered by the Insolvency Service of Ireland. However, since its inception, the ISI has instituted less than 8,000 debt solutions.

State schemes, it seems, have been effective to a point. But they require time – and time may be something that Irish banks are running out of. This could have consequences for those who owe them money.

Bank pressure

For all that “vulture funds” dominate the headlines, the domestic banks still control more than three quarters of loans in arrears. So the issues they face, and how they tackle them, matter to Irish borrowers.

Irish banks are under increasing pressure from the European Central Bank to get their non-performing debts in line with European norms, according to Goodbody Stockbrokers analyst Eamonn Hughes.

Depending on who you ask, vulture funds are either the most mercenary financial institutions in history, or a benign force clearing legacy debts from the Irish market

During 2018, the banks, led by Permanent TSB and AIB, made huge strides to bring down their levels of non-performing debt. But the regulator, the Single Supervisory Mechanism in Frankfurt, remains concerned, according to Hughes. The ECB is concerned about what damage these distressed loans could do to the banks

“Ultimately, the regulator in our view is requiring banks to clean up as soon as possible in case the economic cycle rolls over or interest rates go up,” he says. While the banks have been able to bring down their non-performing loan levels by focusing on selling off loans not linked to family homes, they may be running out of room for manoeuvre and could push ahead with such sales soon.

“Everything is on the table,” says Hughes.

Successful moves by Permanent TSB, which saw it sell some family-home loans, may open the door to what has traditionally been a sticky political issue: the sale of family-home loans to private equity firms, more commonly known as vulture funds, by majority State-owned banks such as AIB and PTSB.

"The fact that Permanent [TSB] went ahead and did it, and for want of a better word got away with it, would indicate that there isn't the resistance they thought there would be," according to Ross Maguire, founder of debt advisory firm New Beginnings. "I do believe there will be more loan sales."

Fear of vultures

Depending on who you ask, vulture funds are either the most mercenary financial institutions in history, or a benign force clearing legacy debts from the Irish market. Sources who work for and with the funds say that their fearsome reputation is undeserved.

One source say that the firms view Ireland as the “most borrower-friendly and probably most expensive foreclosure environment in the world, which makes lenders reluctant [to enforce their security]”.

Another says the suggestion that funds will quickly move to repossess is “totally bogus. It’s either from people who are being disingenuous or don’t understand it”. “Only in extremis will they go for a repossession because they know how long it takes and how much it costs.”

Maguire says funds are more likely to restructure a loan and enjoy the reliable new income stream than sell. “The reality is that they’re not interested in your house, they’re interested in fixing your loan.”

Others, like David Hall, warn that a cohort of those in mortgage arrears, who are not eligible for social housing but cannot afford the private rental market or to restructure their homes, will lose their homes to vulture funds. “And they will become homeless.”

What is clear is that any move to repossess family homes – whether by a fund or a bank – could prove to be politically explosive

Hall rejects the idea that he has been proven wrong by the low rate of repossession. “History will judge who’s right. I’ll sleep very solidly at night and won’t take great pleasure in saying in a couple of years ‘I told you so.’”

Another debt management professional, who has worked at first-hand with the funds, agrees with Hall. “In dealing with your home, it is a different asset and a different asset class. Homes should not be sold to vulture funds,” he says.

“There’s a real inequality of arms between someone who owes €250,000 on their loans, has been making payments, and a fund.”

Research from the Central Bank suggests that there is “no material difference in the number of properties being taken into possession by unregulated loan owners compared to regulated lenders”.

This must be balanced, however, against what vulture funds have bought recently. Research from EY tracking loan purchases by the funds shows that the majority of what they have purchased in the past few years is commercial real estate or business debt. While they have mortgages on their books, the focus has been on the less complex, and more financially rewarding, world of corporate and investment debt.

In short, the available evidence suggests funds may not be as avaricious as they've been portrayed. But it's hard to predict exactly how the secretive funds (several of whom declined to speak to The Irish Times for this article) would deal with a new large-scale influx of mortgage debt, if the banks do sell up.

What is clear is that any move to repossess family homes – whether by a fund or a bank – could prove to be politically explosive, as shown by KBC’s move to repossess a farm in Strokestown, Co Roscommon, before Christmas.

In the current environment, it doesn’t have to be a tsunami to be a problem for banks, their employees, and policymakers.

Some are now suggesting that more radical solutions need to be proposed to solve Ireland’s legacy debt headache without igniting a political tinderbox.

Long term solutions

One such person is John Moran, former secretary general at Michael Noonan's Department of Finance during the most severe years of recession. He was brought in as an outsider, who had learned his trade in the private sector, to shake up a department as it sought to address its own role in the economic collapse.

For Moran, the problem of distressed debt will not simply resolve itself. “There are some problems that get better with time. I don’t think this is one of them. In 2011, it was going to get better because unemployment was going to go down and salaries recover, but we’re as good on all those parameters as we can be,” he says.

Many of the factors outlined above – pressure on banks, a sclerotic courts system and public opposition to repossessions – restrict Ireland’s room for manoeuvre in solving the problem. Meanwhile, due to the weight of non-performing loans on Irish banks’ balance sheets, mortgages are becoming more expensive, argues Moran.

“Why I am particularly worried is if you can’t solve that residual legacy [of] distressed mortgages, then everyone taking out a new mortgage is paying more, and in that event, the economy is essentially losing a huge amount of money each year.”

“Most of these legacy people find themselves still in unsustainable mortgages.”

One solution, he argues, is to seek investors that can buy the mortgages from the Irish banks, but tolerate a much lower level of repayment – perhaps as low as interest-only payments – and have no immediate interest in repossessing a home.

“For societal reasons, it makes sense for many people in this cohort to stay in their existing homes for another period of time – maybe not forever, and not for free.”

Such a solution would alleviate the pressure on the banking system, the courts, and the threat of repossession. It could also provide a solution for borrowers like Mary.

Mary’s partner ultimately received a payout from insurers arising from his accident, and in 2016, they were able to clear their arrears.

However, this proved to be a false dawn. After taking ill, scans revealed that Mary had multiple blood clots in her lungs. She was hospitalised for a month, unable to work. When she was released, she went on unpaid maternity leave.

Again, the family fell into arrears.

With assistance from the Irish Mortgage Holders’ Organisation, they agreed a forbearance period with their lender and are now back paying their full mortgage.

However, thousands of euro in arrears remain, as, ultimately, does the prospect of a lender issuing repossession proceedings. Mary says she tries not to read the newspapers because of the distress they cause her.

“I ended up with seizures from stress. I’m trying not to think too much about it, but it is in the back of my mind, and I’m going through counselling,” she says.

For borrowers like Mary, it seems that lasting solutions can’t come quickly enough.