“Never make forecasts, especially about the future.” Nobody knows who said this first. The point, however, is that we have to make forecasts, or at least guesses, about the uncertain future. Of nothing is this truer than long-term investments for delivering security in old age. The problem – inescapable, but fundamental – is that the sensible way to do this is to invest in risky assets. The risks cannot be eliminated. Someone must bear them. The question is who this should be and how it should be done.

The tragedy of trends in pension arrangements is that the attempt to force safety on private arrangements is forcing them into collapse. Worse, it has allowed the older generation of pensioners to extract all the risk-bearing capacity of private sponsors for their benefit, so moving the younger generation into permanent insecurity. This is a scandal.

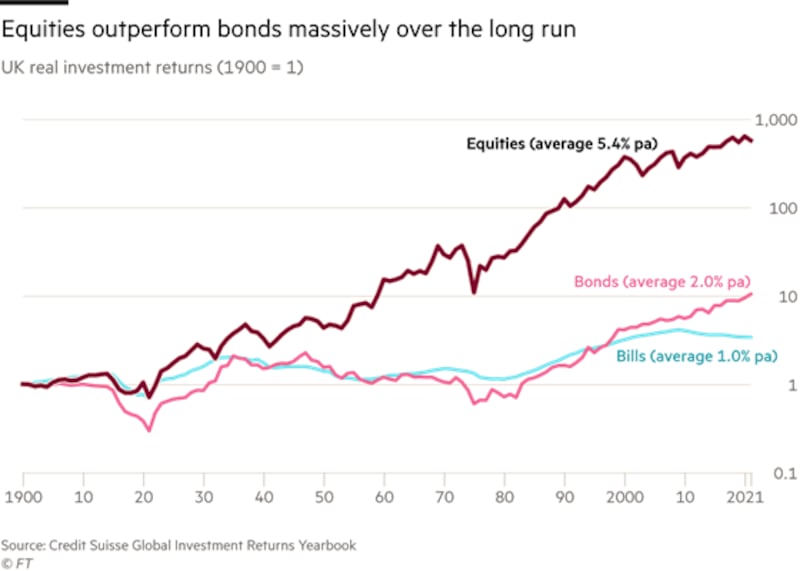

A question, however, is how risky investment in "risky" assets actually is. The evidence on this is encouraging. The work of Elroy Dimson, Paul Marsh and Mike Staunton in successive Credit Suisse Global Investment Yearbooks shows that over the past 120 years diversified portfolios of equities in the corporate sectors of high-income market economies have done staggeringly well.

The geometric mean annual real return in these economies has been 5.4 per cent. In the US the mean return has been 6.6 per cent. In the UK it has been 5.4 per cent. A pound invested and reinvested in the UK market in 1900 would have become £572 pounds by 2020, after adjusting for inflation. A dollar invested in the US market would have become $2,291, on the same basis. But a pound invested in UK government bonds would have become £10.40 and a dollar invested in US bonds would have become $12.50. The only guarantee the bond market gives is one of poverty.

Quasi religion

Economists call this gigantic divergence an “equity risk premium”. The word “risk” reflects a quasi-religious belief that this divergence reflects rational adjustment to risk. Properly risk-adjusted, expected returns were the same. But attempts to justify this belief mostly seem far-fetched.

One justification is that wars or revolutions can ruin equities. This is true. But they also destroy bonds. Moreover, the massive long-term outperformance of equities in the major markets occurred despite two world wars, communist revolutions, the Depression, hyper-inflations, the great inflation of the 1970s and the global financial crisis of the 2000s. Of course, a global thermonuclear war or catastrophic climate change would be worse. But bonds would not bring safety. Nothing would. Global disaster is not insurable.

There is a shortage of speculators able to prevent equities from remaining durably mispriced. The bankruptcy constraint binds markets

People such as the Nobel laureate Robert Shiller and the British economist Andrew Smithers argue that, while stock markets do oscillate, their returns are mean-reverting in the long run. In hindsight at least, such mean-reversion has been striking, notably in the crucial case of the US. This supports the view that holding a widely diversified portfolio of equities is far and away the best long-term investment strategy in our uncertain world. If one is as clever and skilled as Warren Buffett, the returns from attending to signals of under- and over-valuation have been staggering.

Big threat

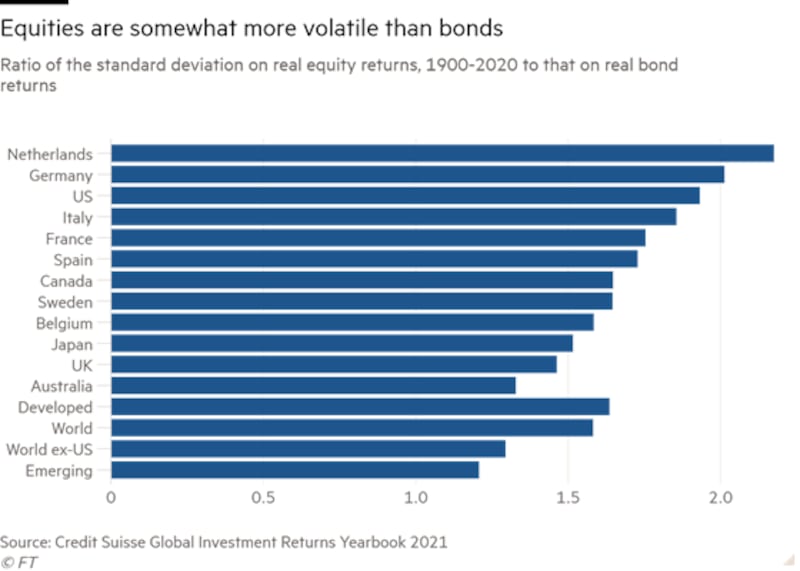

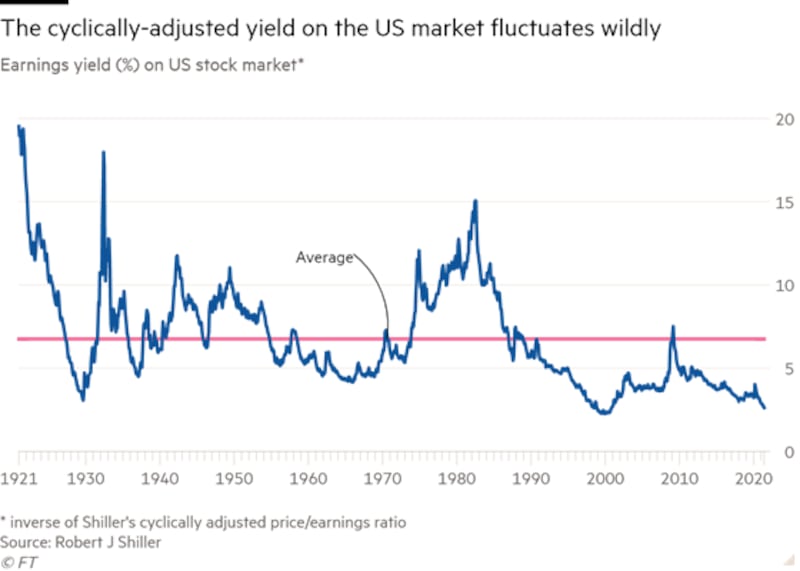

Whether one can rely on this for the future is debated. Moreover, there is an obvious problem: that of the volatility noted above. The variability of annual equity returns has been somewhat higher than that of bonds. Far more important, stock markets can deliver negative returns, from peaks, over long periods. Currently, the cyclically adjusted earnings yield on the S&P 500 is only 2.6 per cent. This is at crash-warning levels, by historical standards. Should a prolonged bear market occur, equity valuations might collapse. The valuations of the mid-1960s did not return for 30 years. The big threat, then, is that, as John Maynard Keynes allegedly said, "the market can remain irrational longer than you can stay solvent". In effect, there is a shortage of speculators able to prevent equities from remaining durably mispriced. The bankruptcy constraint binds markets.

So, equities may offer a free lunch. But you must be able to wait for the meal. This creates an opportunity and a danger. The opportunity is for an investor with a sufficiently long time horizon to make extraordinary returns. In a well-ordered world, multi-generation pension funds ought to be such investors. The danger is that such funds (and still more so individuals investing on their own) will exhaust their room for manoeuvre before their investments pay off. Fears of a huge bear market, not unrealistic at current valuations, might force them into the bond or cash traps. – Copyright The Financial Times Limited 2021