The Republic's economy – measured by gross domestic product (GDP) – is now officially 50 per cent larger than it was in 2007, before the Celtic Tiger period came to a crashing demise.

But while house prices and Dublin’s Iseq index have rebounded strongly from their crisis-era lows, and punters have flocked back to the Galway Races, most barometers have not recovered to where they were before the property and banking bust.

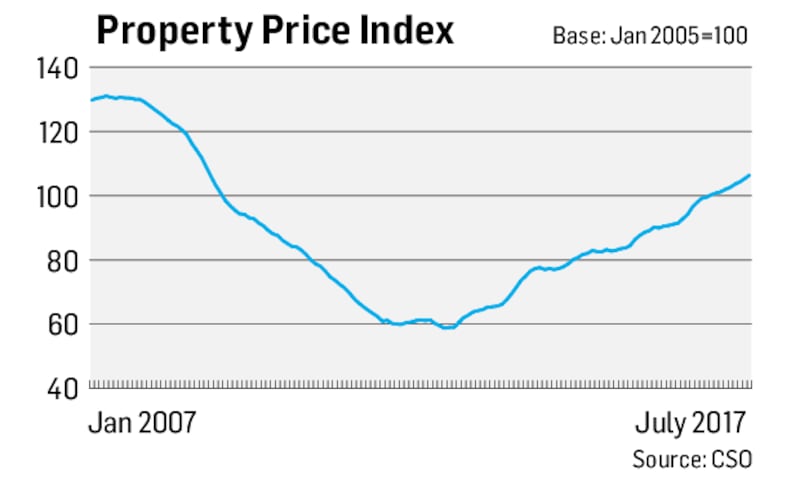

HOUSE PRICES

Irish house prices, which quadruped in the decade to early 2007, began to decline that April and would plunge by more than 55 per cent before bottoming out six years later.

While residential property values nationally have rallied by 81 per cent from their lows – with Dublin prices up almost 94 per cent – they remain nearly 19 per cent off their 2007 peak. The most recent data show that although prices across the country were rising at an annual rate of 10.4 per cent in July, inflation in south Dublin had slowed to 5.2 per cent.

MORTGAGE ARREARS

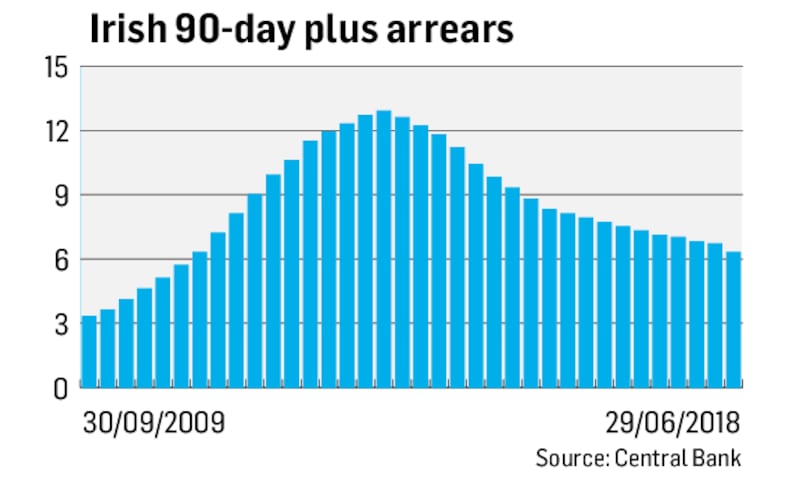

Mortgage arrears were so low in Ireland in the pre-crisis era that the Central Bank did not even feel the need to collect and publish regular data on them.

However, almost 13 per cent of owner-occupier mortgages were at least 90 days behind in repayments by 2013 – and the figure would have been much higher were banks not offering struggling borrowers temporary forbearance. Overall arrears levels have fallen dramatically from their peak, aided by more than 116,000 restructuring arrangements. Still, more than 28,000 home loans were more than two years in default at the end of June.

BOND YIELDS

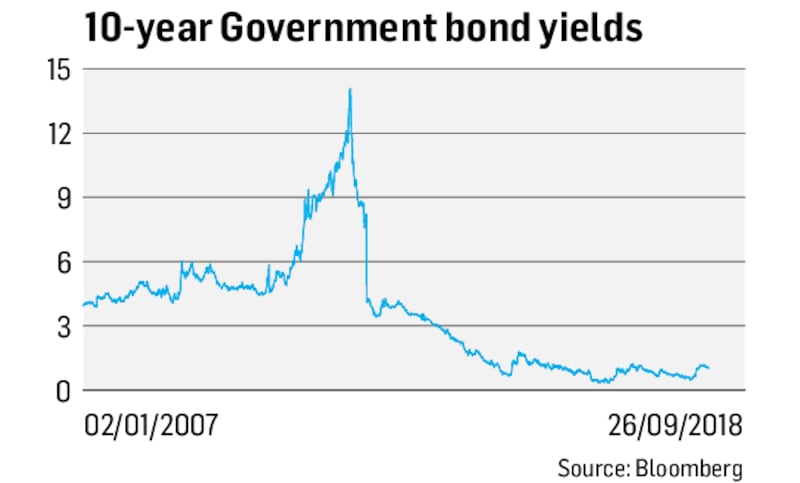

The market interest rate – or yield – on the Republic’s 10-year Government bonds was the most widely-watched benchmark for financial markets at the height of the crisis. The yield peaked at 14.1 per cent in July 2011, as investors bet the State would not be able to stand behind its ailing banks – even with the help of an international bailout.

However, the rate began to fall later that month as US fund manager Michael Hasenstab began to snap up Irish bonds and a group of North American investors made a rescue investment in Bank of Ireland. It plunged further in the years that followed as European Central Bank president Mario Draghi made good on a promise to do "whatever it takes" to save the euro.

BMW SALES

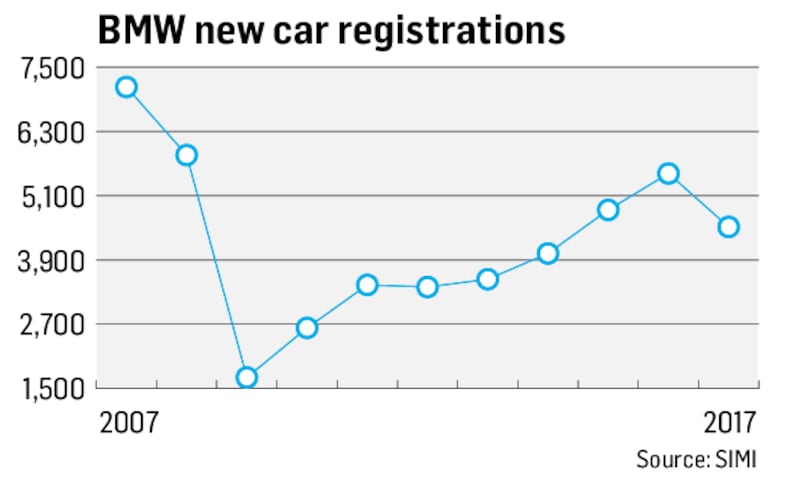

As the Republic’s economy boomed, BMW became a Celtic Tiger car brand of choice. By 2007, it was the seventh biggest selling car brand on the market, boosted by the popularity of its 3 Series and 5 Series models, a favourite of the nation’s burgeoning management class.

For the motor trade, the recession coincided with uncertainty caused by changes to the tax regime. More recently the recovery in new car sales has been hampered by the lure of UK imports on the back of weaker sterling.

UNEMPLOYMENT RATE

The country’s unemployment rate trebled to more than 15 per cent in the four years to early 2012, pushing the Government’s social welfare costs higher at a time when revenue from income tax was falling.

The rate would have been much higher, were it not for a wave of emigration as Irish families – and recently-arrived eastern European workers – left the country in their droves. Figures recently released by the Central Statistics Office show that the number of people returning to live in Ireland in the 12 months to April overtook those emigrating for the first time since the crash.

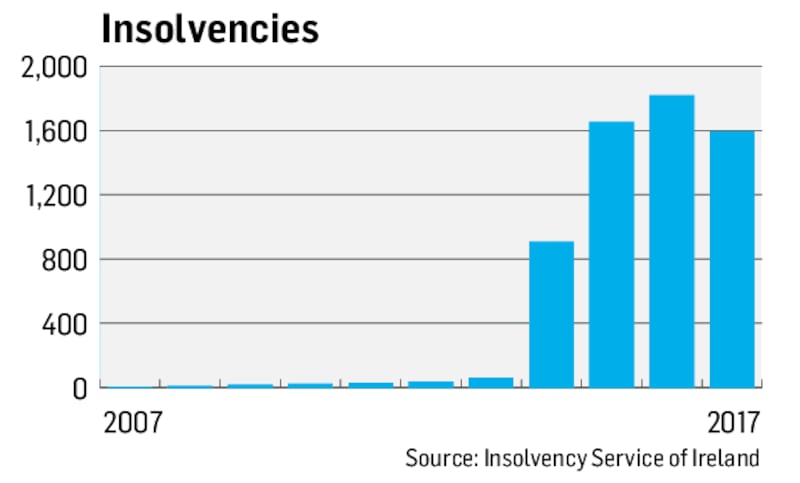

INSOLVENCIES

Personal insolvencies have soared in the decade after the property crash, boosted initially in 2013 by the shortening of the bankruptcy term to three years from 12 as well as the setting up of the Insolvency Service of Ireland, which allowed for three different categories of debt-relief arrangements to deeply distressed borrowers.

Outright bankruptcies – which account for 2,081 of the insolvencies in the last 10 years – were fuelled further by a further reduction in the bankruptcy term to one year. Many more insolvencies were averted by banks, under pressure from regulatory authorities, agreeing restructuring deals on soured loans.

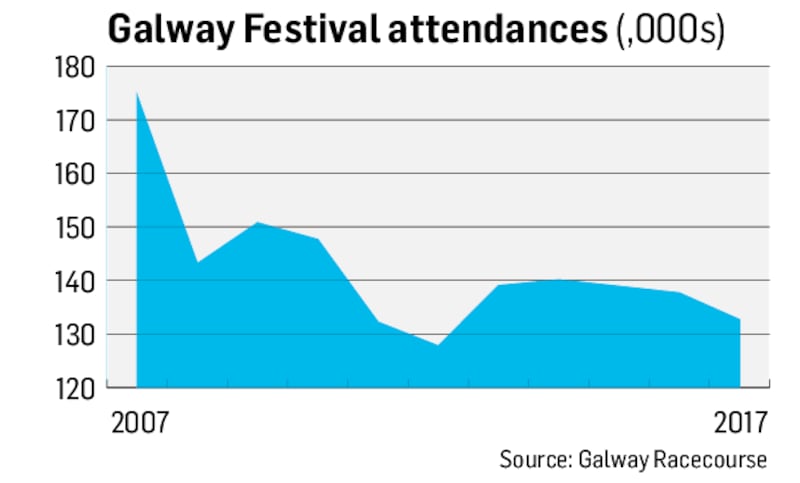

GALWAY RACES

Few places offer a better check on the pulse of the nation than a trip to the Galway Races, Ireland's biggest horse-racing festival, the favoured boomtime stomping ground of builders and home of the infamous Fianna Fáil fundraising tent.

Attendances at the seven-day festival collapsed in the wake of the property crash, though they began to build back up in the summer of 2014, months after the State exited a three-year international bailout programme. Still, this year’s number of attendees remained 39 per cent off the 2006 peak.

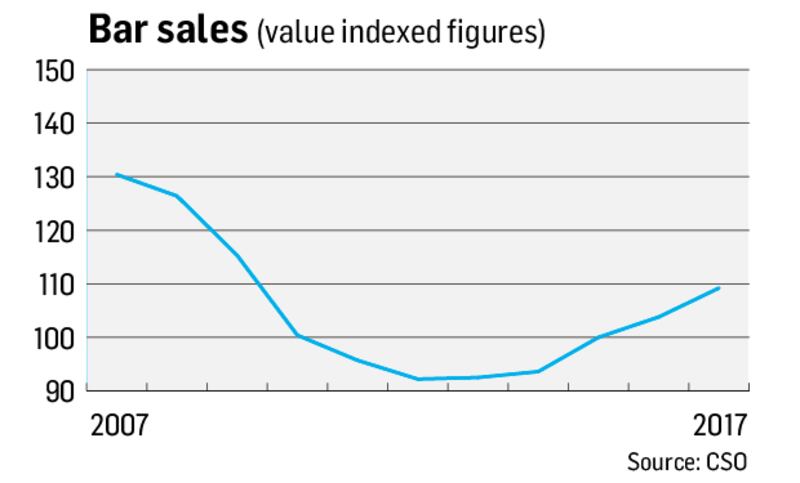

BAR SALES

As the economic tide went out in 2008, bar sales began a precipitous four-year decline. By 2012, pub revenues were a third lower than 2007 and many publicans who had borrowed heavily were insolvent.

Pubs then staged an impressive recovery as the wider consumer economy returned to black in 2014. It began first in Dublin city centre before rippling outwards, fuelled by a nationwide tourism boom. Pub sales have risen each year for the four years, and are on course for their fifth year of growth in 2018.

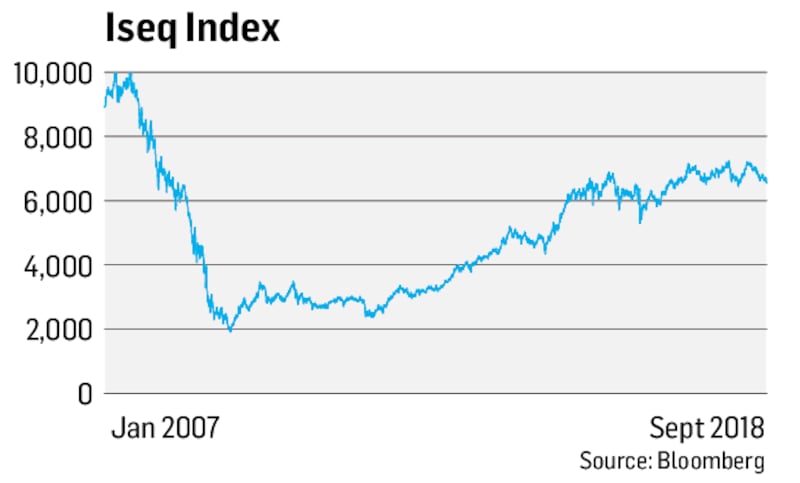

ISEQ INDEX

Dublin's benchmark Iseq stock market index raced tantalisingly close – within 20 points, in fact – to the 10,000-point level in late February 2007 as heavyweight stocks AIB and Bank of Ireland hit all-time highs, just months before house prices peaked.

The Iseq would slump by 80 per cent over the next 24 months, as banking stocks spiralled downwards, and giants of the market such as CRH and Smurfit Kappa were hit by the global recession. While US shares are currently hovering around all-time highs and the wider European market is hovering around pre-crisis levels, the Iseq remains about a third off its 2007 height.

GDP

Ireland’s gross domestic product (GDP) last year was almost 50 per cent greater than it was in 2007 – having been turbocharged in 2015 as multinationals moved massive amounts of assets, mainly intellectual property – to Ireland.

While the 2015 jump prompted Nobel Prize-winning US economist Paul Krugman to decry Ireland's "leprechaun economics", the GDP figures have also given an over-flattering picture of the health of that State's finances, pushing debt-to-GDP from a peak of 123 per cent in 2013 to below 70 per cent currently.