House prices in recent years should never have been allowed to soar to the point where they have become unaffordable for the vast majority of aspiring purchasers. Rents in the private rental sector are also unaffordable for most. Vendors seeking inflated prices for their homes have been forced to reduce them, as demonstrated by recent estate agent and auction results. Here are 10 reasons why significant falls in house prices and rents are likely to occur sooner rather than later.

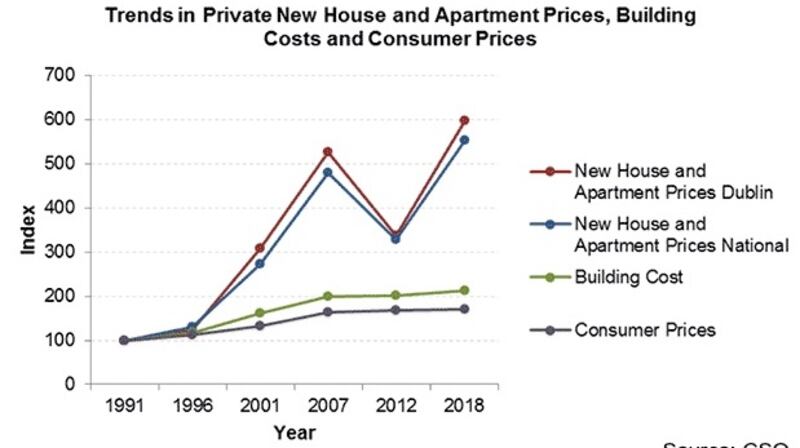

1. As recently reported by the Economist magazine, housing in Ireland is now significantly over-valued or, more accurately, over-priced. This over-pricing is reflected in new house and apartment prices that are now well above their peak in 2007. In fact, for over 20 years house prices in Ireland have been completely out of line with indicators such as the Consumer Price Index, the cost of building and average earnings. Despite falling for a short period after the crash, prices have climbed sharply since 2012. This dramatic escalation was avoidable and simply cannot be justified by Government.

2. Large increases in house prices and rents are bad for the economy and for society. If a high proportion of disposable income is tied up in rent or in repaying mortgage debt for an extended period then less disposable income is available for expenditure on employment-creating activities in retail and other consumer-related businesses. High house prices and rents are impacting on competitiveness. They affect social cohesion and have resulted in deep inter-generational inequality, in that young adults can never aspire to purchase or rent even in relatively modest areas where they were born and raised.

3. Even if they have never studied economics, consumers are beginning to appreciate the basic economic principles of demand and supply. Demand (the willingness and ability to pay or borrow for something) plays a key role. Influenced by a “herd mentality” or “irrational exuberance” similar to pre-crash days those seeking homes over recent years have been encouraged to purchase irrespective of whether such homes can be afforded on an ongoing basis. Many now realise that if sufficient numbers stop bidding or buying, house prices will quickly fall. After all, that is the logic of the market.

4. The “Help to Buy” scheme - a tax allowance introduced by former minister for finance Michael Noonan has undoubtedly contributed to demand and to the price increases illustrated in the diagram. The allowance costing over €100 million to date, including on homes in excess of €450,000, has been more than offset by increased house prices. No government can justify a continuation of this wasteful expenditure. If the scheme is terminated at the end of 2019, as stated at the time of its introduction, then this will help to reduce house prices.

5. The vast majority of mortgage exemptions, which allowed purchasers to borrow more than the standard 3.5 times income and save lower deposits, so helping to inflate demand, have now run out. The capital gains tax holiday given to multinationals will also soon terminate. Both of these changes will reduce demand and hence house prices.

6. The significant increase in supply expected from private developers has not materialised. The much-lauded “market” has failed to deliver. No government can allow this to continue. Prior to the 2008 crash, private developers built too many houses and in the wrong places. Now they are building too few and are drip-feeding small numbers of expensive homes onto the market to maintain prices. Large Irish and international investors are manipulating the market to maximise their profits at the expense of home buyers and renters. To remain in business, however, they will have to build a considerable number of homes over the next few years if only to avoid the vacant site tax. This again will dampen down prices and rents.

7. In the whole of 2017, fewer than 2,000 houses were built by local authorities and voluntary housing associations; in the first six months of 2018, just over 800 units were built (Part V provision supplied around 500 units in 2017 and 250 in 2018). Yet, it is widely accepted that at least 10,000 new units of social housing are required each year to meet existing and growing demand. Provision of additional social housing on this scale would begin to substitute for schemes such as the Housing Assistance Payment (HAP) currently paid to private landlords, including multinational landlords - schemes which are not just expensive for the State but offer no security to tenants. The competition represented by the provision of social housing on a large scale would have the immediate effect of reducing house prices and rents.

8. Local authorities are currently purchasing homes at market prices. They are therefore in competition with first-time and other purchasers, thereby increasing demand and contributing to house price increases. Government policy must change so that local authorities can concentrate on building directly rather than purchasing ito meet social housing needs. This would again reduce house prices.

9. The May 2016 Programme for Government promised a “cost-rental” scheme for those ineligible for social housing. Cost rental housing - which operates successfully in a number of European countries - would be a not-for-profit, self-financing, publicly owned initiative with rental income covering the costs. Rents would be well below the current unaffordable ones, so providing competition to private landlords. If the Government was to make a serious commitment to providing this type of housing on a significant scale it would help to reduce house prices since households would have the option of postponing purchase for a time or indefinitely.

10. The Irish economy has performed well in recent years, at least in terms of GDP (a questionable indicator especially in Ireland) and employment growth. However, we have the highest level of per capita debt in the euro zone and are unduly reliant on a small number of multinational companies. The fall in sterling has serious implications, and Brexit, whether hard or soft, will have a disproportionate and costly effect and will impact on employment. The protectionist policies being pursued by the United States are also likely to have a serious impact on Ireland as well as on global trade and growth. These new realities, largely outside our control, engender uncertainty and will adversely affect our economy. A fall in house prices and rents will inevitably follow.

Various commentators with a vested interest will argue there is no problem: there is no housing bubble and, in any case, there will be a “soft landing”. This is exactly what they were saying prior to the crash in 2008.

P.J. Drudy is Emeritus Professor of Economics in Trinity College, Dublin