Like a lot of Irish people her age, Elizabeth feels trapped.

“The help-to-buy scheme is no good to me because the cost of new builds is so astronomical as to make it pointless to even try.

“I’m also not eligible for the lower-income mortgages provided by the local authorities as I earn too much, but not really enough to do it on my own.”

In her early 30s and living in Dublin, she spends thousands a year on rent while trying to save for a deposit.

As a single person, she feels even more constrained by the Central Bank’s rules which limit lending to 3½ times household income. Even if a deposit could be saved, the price tag for homes in areas where she wants to live leaves them out of her reach.

The future for people like Elizabeth is uncertain; hemmed in by record rents, restrictive rules on mortgage borrowing and ever-climbing house prices, they are stuck in a rental sector that offers few protections and little certainty.

Statistics show that Ireland is undergoing a historic shift in its traditional pattern of home ownership. But what does this mean for Irish people, and who are the winners and losers from this process?

A nation of homeowners

In many ways the Irish experience of independence has been one of gradual but significant improvements in living standards. Much of this has been driven by the accumulation of property, primarily owning one’s own home.

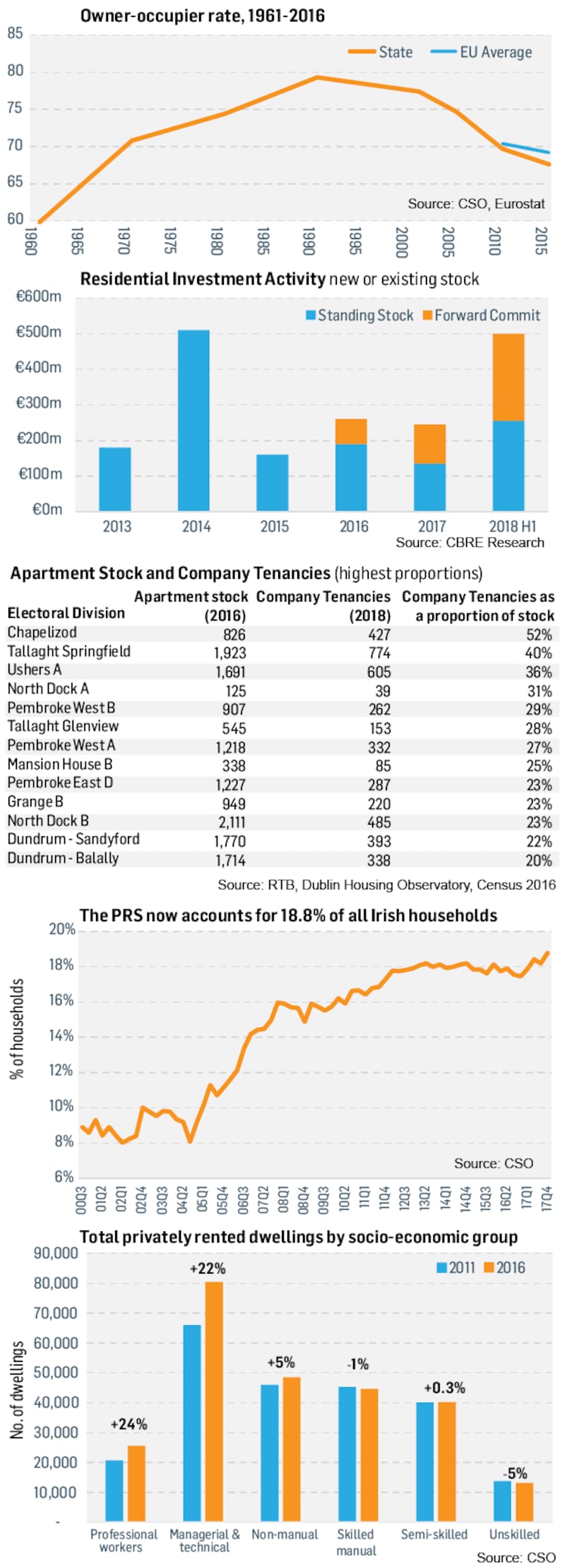

This peaked in 1991, when 79.3 per cent of Irish people were homeowners.

There is plenty of folk wisdom about what drove this; an innate yearning among a historically dispossessed people for the security of ownership; an obsession with land stemming back to the Famine years and beyond.

The reality, however, is that this was done by design, not by accident. UCD professor of social policy Michelle Norris, who is on the board of the State's new land development agency, says home ownership was the defining social policy goal of successive Irish governments.

Large-scale social housing programmes also delivered local authority homes to low earners, who were encouraged to buy long before the idea caught on in other countries

“There’s no doubt that the expansion of home ownership was built on enormous levels of State spending,” she says. It was, she argues, so massive that it is impossible to calculate a precise figure.

Grants, rates remissions, tax reliefs, interest reliefs and more interventions were prominent, while the State’s appetite for the provision of healthcare, education and a social welfare was subdued.

“It was really giving people property as a form of welfare, rather than redistributing income as they did in other countries,” she says. Periods of high inflation, such as in the 1970s, made the burden of mortgage repayments significantly easier to tolerate, while renters were generally composed of the very young or the very poor.

According to a recent research paper from the Department of Finance, "by the 1980s Irish private rental accommodation was a 'forgotten tenure', with the majority of privately rented homes being of poor quality and intended for temporary accommodation".

Large-scale social housing programmes also delivered local authority homes to low earners, who were encouraged to buy long before the idea caught on in other countries.

“Thatcher thought this was a great idea in 1981, but we introduced it in 1936,” says Norris.

A changing picture

Starting in the 1980s, the once-common bonuses for home buyers on offer from the State gradually fell away.

Councils trimmed their role offering mortgages, and banks emerged as major lenders in place of building societies. Even during the boom, the level of home ownership was declining and it continued to do so during the recession. Between 2011 and 2016, home ownership fell 2.1 per cent.

At the last census the home ownership rate was 67.6 per cent, lower than the EU average of 69.2 per cent.

"We've moved far faster than people think," says John Moran, chairman of the Land Development Agency.

"The evidence is very strong that there's a real shift," says Dr Rory O'Donnell, director of the National Economic and Social Council. "There's every reason to believe it's fairly permanent because the conditions which underpinned high levels of home ownership at early stages of the life cycle, those conditions have gone."

There is what property insiders describe as a "wall of cash" trying to get into the Irish rental sector

The traditional image of the Irish homestead, bursting at the seams with children, perhaps with a grandparent or two thrown in for good measure, has also never been less accurate.

Of 600,000 households formed since 1996, some 400,000 are estimated to comprise either one or two people. Average household sizes are now 2.75, ahead of European averages, but the Department of Finance believes “there is no obvious reason why Irish rates will not continue to converge with the European norm”.

Rent seeking

Renting is a reality for more people living in Ireland than ever before. However, the structure of that sector is still shaped by the fact it was for so long a forgotten child.

Compared with other markets, Irish renters face uncertainty on rent costs, how long their leases are and what the future holds for them.

“When you look at more developed markets, they have spent more time thinking about these issues than we have,” says John Moran.

There have been reforms in recent years – most notably rent pressure zones, and just this week, extensions to notice-to-quit periods and penalties for landlords who break the rules on termination provisions.

The surge in renters – and rents – has made for good business for a lot of overseas investors. Profits at Ires Reit, the State's largest private landlord, climbed from €65.1 million to €119.8 million last year, earning its chief executive, Margaret Sweeney, a €330,000 bonus, on top of the same sum in salary.

There is what property insiders describe as a “wall of cash” trying to get into the Irish rental sector. Estate agent CBRE has estimated that there is €7 billion of so-called institutional capital – large swathes of cash, controlled by professional money managers – chasing apartment stock in Ireland.

These investors can afford to outbid individual buyers as well. One industry analysis shows that for a notional development of 50 apartments in Dublin, a builder could expect to make just short of €17 million in sales.

However, if an investor could extract an average rent from each apartment of €2,000 a month, it could afford to pay a builder €24 million. It is no contest, and recent sales have seen large homebuilders such as Cairn Homes and Glenveagh sell entire apartment developments in one fell swoop.

Overall, large institutional landlords such as Ires Reit or American investment fund Kennedy Wilson make up a tiny percentage of the national rental market. According to the residential tenancies board, less than 5 per cent of tenancies are controlled by landlords with more than 100 tenancies in total.

There are only 19 landlords in the State with more than 200 tenancies each. But they are growing, and in certain segments the growth is more pronounced.

It is clear that Ireland's shift towards rental is extremely lucrative for some

Although it is still low, the Department of Finance estimates that the number of landlords with more than 200 properties more than doubled between April 2014 and December 2016. The same research suggests that corporate landlords are being concentrated geographically.

In 20 areas in Dublin city, more than 20 per cent of apartments were rented out by companies. In 2017 more than 40 per cent of all new apartments in the State were bought by firms categorised as being in the financial and insurance or real estate sectors.

Meanwhile, investors benefit from specially designed tax structures such as the Reit (Real Estate Investment Trust) regime.

John Moran, who helped design the scheme, says criticisms of it are poorly founded, but nonetheless it is expected that the Department of Finance will review the scheme in advance of the budget this year, benchmarking its generosity against other jurisdictions.

There are concerns that an overconcentration of ownership of the rental stock could lead to “monopolistic or oligopolistic” pricing power, the crowding out of first-time buyers, or a sort of inverse ghettoisation, where rich people are concentrated in enclaves of luxury apartments owned by international investors.

Although it is early days, and the impact can easily be overstated by eye-catching examples, it is clear that Ireland’s shift towards rental is extremely lucrative for some.

A time bomb

For a society like Ireland, perhaps it is unsurprising that trends such as those described above can rankle. However, there is a persuasive case to be made for institutional investment and moving away from property ownership.

“The advantages of institutional investment are manifold, broad-based and beginning to yield positive outcomes for the Irish housing system,” the Department of Finance has argued.

The construction and purchase of homes by these players supports a host of goals the Government has, from increasing density to switching the source of funds for Irish property development away from banks and towards international money markets.

Ireland, it is suggested, may end up being more like Germany, with long-term leases at affordable rents offered by large-scale professional landlords.

Each of us is worth about €140,000, and €70,000 is in housing. We have to rely on the value of those assets to see us through the ups and downs of life

The problem, critics say, is not necessarily with the shift towards rental, or who you might be renting from, but with the structure of Irish wealth itself. And the fear is that we may be storing up serious problems for the future.

"We've seen a revolution in the housing sector of renting long term, if not for ever, without addressing the socio-economic context to see whether that is feasible or not," according to Lorcan Sirr, a lecturer in housing studies and urban economics at the Technological University in Dublin. "And right now, it's simply not."

“About half of Ireland’s wealth per capita is tied up in housing. Each of us is worth about €140,000, and €70,000 is in housing. We have to rely on the value of those assets to see us through the ups and downs of life.”

The Irish experience of a house standing in for the welfare state counts for pensions, too, according to Moran. In other jurisdictions people can often expect a high percentage of their salary in pension, enabling them to keep paying some form of rent until they die.

“The way Irish people tended to deal with that is through high home ownership,” he says. Basically, housing in retirement was free once a mortgage was paid off, allowing for a massive drop in income.

We are going to have a ticking time bomb when the current generation of 25-to 40-year-olds hit retirement

The problem is that with an underfunded pension scheme, and dwindling levels of home ownership, a whole generation of Irish people face the possibility of spending their working life paying high rents with nothing to show for it when they retire – and no income to fund the roof over their heads. In the interim, many of the benefits of home ownership – such as releasing equity to fund a child’s education – will remain out of the reach of renters, who will also see other parts of their lives curtailed as large chunks of their income is handed over to a landlord each month.

“It’s very hard to see anything emerging apart from higher levels of renting. It’s problematic socially and it’s problematic economically,” says Michelle Norris. One possible solution is to engage in large-scale development of so-called “cost rental”, where rents are determined by the cost of providing the home, rather than what the market will command.

Such developments have been successful around Europe, most notably in Vienna. Earlier this week a week-long exhibition was launched by Dublin City Council and the Housing Agency on this very model.

However, these models have been common in cities like Vienna for generations. There is no guarantee that Ireland can deftly, and rapidly, make the switch.

What is clear is that the dramatic shift away from property ownership will need equally dramatic policy solutions.

“We’ve gone down a route that is promoting renting without fully analysing the potential impact of having fewer people owning their own properties,” says Lorcan Sirr.

“If we don’t start housing people affordably, we are going to have a ticking time bomb when the current generation of 25-to 40-year-olds hit retirement.”