They’ve been singled out as playing havoc with the Central Bank’s efforts to put some manners on the housing market.

Earlier this month, governor Philip Lane said cash buyers are limiting the regulator's ability to control house prices as they are outside the scope of the bank's prudential rules.

If they only accounted for about a fifth of the market or so, as was typically the case, it may not be so much of an issue, but figures show that more than five in every 10 purchases in the residential property market is by a cash buyer.

It’s a startling figure when considered in an international context. In the UK for example, cash buyers account for around 35 per cent of all transactions, up from 20 per cent in 2005-2006, according to Nationwide, while in London, cash buyers now represent just 19 per cent of the market.

So who are these cash buyers and how come there are still so many of them?

How many cash buyers are there?

Before the crash, cash buyers appeared to be in more scarce supply. Figures from the Central Bank show that at the pinnacle of the boom in 2006, cash buyers accounted for about 25 per cent of the 151,000 or so annual transactions. Back in 2000, there were about 28,000 cash sales out of a total of about 102,000 or about 27 per cent.

But, as transaction levels plummeted, the proportion of cash buyers soared, reaching a peak of about 63 per cent in 2013.

In that year, for example, there were fewer than 40,000 transactions, so the 25,200 cash buyers in that year is less than the number of cash buyers reported in 2000. As a Central Bank report from last year notes, “the actual number of cash-buyer transactions is not necessarily atypical of the early years of the last decade”.

So the current volumes of cash-only sales “are not entirely out-of-step” with years gone by.

“It’s a bit bouncy from quarter to quarter, but on a four-quarter moving average basis, you can see that it is gradually tapering, very very slowly,” says John McCartney, director of research at Savills.

From that high of 63 per cent in 2013, the proportion has most recently dropped to about 53 per cent.

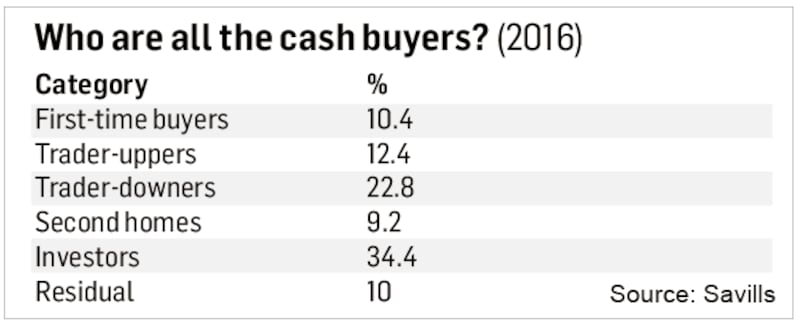

So who are they?

- They’re investors

According to figures compiled by Savills, investors are some of the main drivers of cash sales, accounting for a little more than a third of all cash sales last year. And when you consider purchases by institutional investors such as reits and property funds are excluded, the figure for the entire market is likely to be higher.

With gross yields of about 6-7 per cent now available on property in Ireland, “logic would tell you” that this will attract investors, McCartney notes.

And there is plenty of money available for property investment, with Central Bank figures pointing to household deposits of the order of about €100 billion - and rising.

“If you have €300k-€400k in the bank on deposit, what are you going to do? It’s inevitable that that cash is going to find its way into the market,” says McCartney.

Keith Lowe, chief executive of estate agents DNG, agrees. "They might have money on deposit at 0.5 per cent that's effectively losing money with inflation. So rather than keep money on deposit, they go out and buy property for a net return of 6 per cent, once they pay their tax. It starts to make sense at today's prices."

Investors will typically pay in cash for an investment, either because of the absence of buy-to-let mortgages, or because it can be cheaper and they have access to the funds.

Last year, some 89 per cent of investors bought entirely with cash according to Savills figures, “and if you went outside Dublin it would probably be even higher”, McCartney says.

Auctions may not be as prevalent as they were back in the days of queues outside the Shelbourne Hotel, but they are still a part of the market, and “you can be sure all of those are cash buyers; you wouldn’t have time to get a mortgage to go to an auction”, says Lowe.

But what about all the investors who we hear are leaving the market due to the stringent costs of running a rental property?

McCartney doesn’t beat about the bush on this. “It’s a load of crap,” he says, adding that such a line was “self-serving” and was put out there to “effectively lobby the government against rent caps” – which didn’t work.

Drawing on data compiled by the Central Statistics Office for its Quarterly National Household Survey, McCartney has found that, in net terms, given the continued rise in numbers of people renting, “the number of units entering the market must be greater than those that have left the market”.

So the perception, which is still out there, gained momentum, and became a “stylised fact”, McCartney says. Investors are still very much in the market.

– They’re first-time buyers

With income multiples of just 3.5 per cent available for properties in Dublin, many parents are reaching deep into their pockets to help their children get on, or move up, the property ladder. And rather than just help with the deposit, many are buying the property outright.

Savills figures show that, in the second quarter of 2017, some 11 per cent of cash buyers were first-time purchasers.

Lowe has observed that more parents buy properties for their children to live in while they attend college in towns and cities around the State, while others may be cash-rich returning emigrants.

– They’re downsizers

Downsizers are another key cohort of those buying in cash, as, having sold their own house, they may then be in a position to pay cash for their next purchase. They are not as active as one might expect, however.

“The problem is that there’s no bridging finance,” says Lowe, noting that many people can’t afford to buy a new house – even if it is cheaper – without selling their own one first, unless they want to depend on the hazards of today’s rental market.

Should we be worried about cash buyers?

As the Central Bank governor noted earlier this month, macroprudential rules aimed at keeping house price growth under control will have only limited impact when as much as 60 per cent of transactions are going to cash buyers.

As he noted, there is “no fixed relation between credit conditions and the evolution of house prices”. While this undoubtedly makes sense, the question perhaps is why this wasn’t considered when the rules were first introduced. After all, a hefty proportion of cash buyers is nothing new, as the graph shows.

As McCartney notes, what’s actually happened is that people have had to stay out of the home ownership market due to difficulties in getting a mortgage, meaning pressure on the rental market has intensified. This in turn pushes rental yields up, which attracts investors who come in and compete with each other and residual owner-occupiers, and “drives price growth through the back door”.

“The rules are not going to be capable of retaining house price growth because of cash-rich investors,” as McCartney asserts.

It’s also driving inequality and access to the property market. How can a couple, or an individual, on an average salary hope to compete with a cash-rich investor when they’re constrained by lending limits and ever rising prices?

Does buying in cash give you an advantage?

It’s enough to strike fear into the heart of any home purchaser – you’re told you’re up against a cash buyer in a bidding war. So do cash buyers have an advantage?

In short, yes. When there are two buyers up for a property, the vendor “probably would favour a cash buyer as there is less chance of it falling through”, notes Keith Lowe, chief executive of DNG.

“It makes you stand out. If you can arrive in to a viewing and say my house is sold, and I’ve cash in the bank ready to buy, it puts you in a strong position,” he says.

A purchase backed with a mortgage can always fall through if the bank doesn’t agree on the valuation of the property or if the mortgage application falls through.

Lowe recalls one putative buyer who had gone sale-agreed, only to be knocked back when the bank informed him his previously approved exception to the mortgage lending rules was no longer on the table as the bank had reached its exceptions limit.

A cash offer is not subject to any of these conditions, which also means it should move much quicker, with a typical timeframe of about four weeks, compared with double or treble that for a sale backed by a loan.

It’s also cheaper; with typical mortgage rates of around 3-3.5 per cent, a purchase for a cash buyer is already cheaper by this amount, as they don’t have to service hefty interest payments.

Moreover, thanks to vendors’ preference for a cash buyer, they can often negotiate a cheaper sale price.

“Someone may bid €300k, but a cash buyer with a €298k bid may be a safer bet for them,” Lowe notes.