Do you ever think about that money you could have invested in the stock markets but instead kept on deposit? Or that inheritance you used to buy an apartment but often wondered whether you should have invested elsewhere instead?

Which assets, have performed best over close to the last three decades, stretching back to 1990?

Most assets are prone to periods of boom and bust, such as the "bust" even deposits are going through at the moment. Over the long term however, certain assets tend to outperform others.

One point to remember is the impact of inflation, which can eat away at returns. Fortunately, since 1990 inflation has been low. According to the Central Statistics Office’s measure of inflation, the Consumer Prices Index, prices we pay for goods and services have risen by just 1.96 per cent a year on average during this period.

So which assets have performed the best – and which have fared the worst?

What has given the best returns?

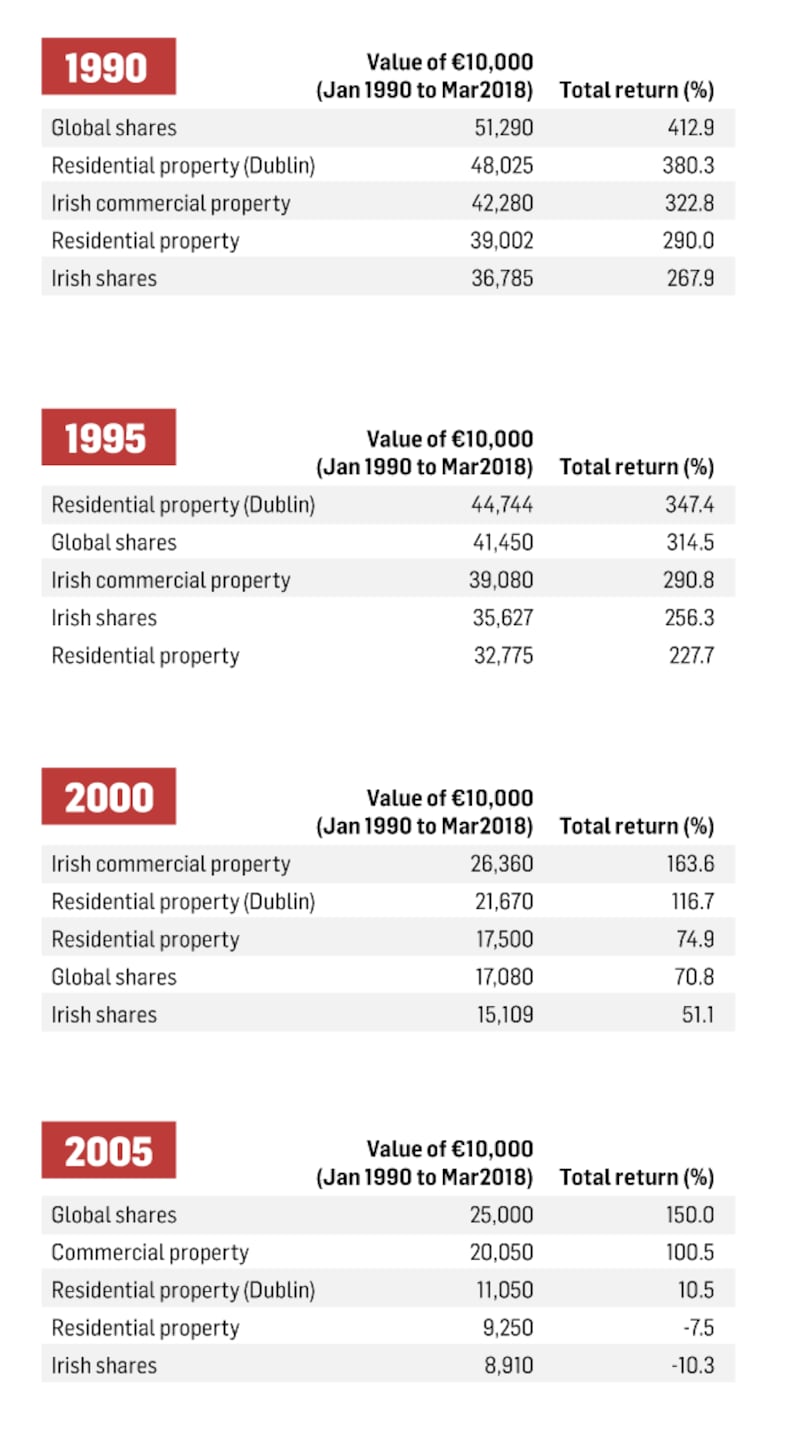

Well, like most things, it all depends on when you invested. Take Irish residential property. According to the Central Statistics Office price index, its value has risen threefold since 1990, despite collapsing after the 2008 financial crisis.

If you had invested €10,000 in residential property back in 1990, it would be worth about €39,000 today. Or to look at it another way, if you had bought a house for €60,000 back in 1990, it would be worth €174,000 today.

The performance is even stronger in Dublin, where prices are up by 380 per cent since 1990. This means that a €60,000 house bought in the capital that year would be worth about €228,000 today.

However if you had waited until 1995 to buy, your returns would be less, given the greater impact the bust would have had on asset values over the shorter time period. Indeed your €10,000 invested in property nationally would only be worth about €32,775, or €44,744 in Dublin.

Even if you had bought in 2000, you would still be in the money, with prices up nationally about 75 per cent since that date. And by about 117 per cent in Dublin. Fast forward to 2005, however, and we can see that many boom-time buyers are still in the red – although many Dublin buyers will have turned it around and will be up by about 10 per cent over the period.

If our investor had opted for commercial property back in 1990, they would have underperformed Dublin residential. But, crucially perhaps, their investment, while volatile from year to year, would have given them a better return over a period marked by the huge crash in property prices as commercial property recovered from much more strongly than residential.

If you consider the MSCI Irish Property Index since 1990, you will see years of huge growth – 1998 for example, when the market rose by 38.6 per cent in just those 12 months, or 2014 when it was up by 39.3 per cent. But there are also years of substantial losses. In 2008, for example, the market crashed by 35 per cent.

Investors who needed access to their money at the time had to crystallise their losses. But those who could afford to wait it out will be sitting pretty again, with the market up 100 per cent since 2005, meaning people who invested at that heady time will still have doubled their money over this period.

Stocks and Shares

What about shares? Irish shares, once the favourite of every pension fund manager in the State, have had a mixed performance since 1990. Those who invested in that year will still be well ahead, by almost 270 per cent over the period. However, those who invested later will have missed out on those early years of strong growth and will have to contend with the dot.com crash of 2000 and the market meltdown triggered by the 2008 financial crisis.

The Iseq Index is down by about 10 per cent since 2005 – one of only two asset classes that are still in the red over this period. Of course, today's index is practically incomparable with that of 2005, when bank shares accounted for as much as 40 per cent of the index.

And the winner is...

Over the long term, investing in a bucket of global shares would appear to offer the best return. Since 1990 they have risen by more than 400 per cent, beating all other asset classes in our survey.

It is also the strongest performer over the past 13 years, returning 150 per cent. The collapse of the dot.com bubble back in 2000/01 was the only period it underperformed other asset groups, significantly hitting investors who put their money into global shares at that time.

Otherwise, this asset class is the strongest performer, as tracked by the MSCI World Index which invests in large and mid-cap equities across 23 developed markets countries. However, there is a caveat. It is only possible to get euro denominated returns for the index since 2000. That means we’re talking about dollar returns since 1990. The true return for Irish investors may be more or less, depending on currency fluctuations during this period.

Since 2000, when we can get euro returns for the index, Irish investors will have seen their money grow by about 71 per cent. And even the collapse of the market following the financial crisis in 2008 hasn’t hit investors too hard over the period since 2005, with returns up by 150 per cent over this period, thanks largely to US markets reaching new highs.

And the losers?

Over the past 28 years, every asset class in our survey is up; but there is no doubting that Irish residential property and Irish shares have delivered the lowest returns.

For newer investors, and many home owners, it is the most recent figure that may be of most interest. Both asset classes are down over the past 13 years – Irish residential property by 7.5 per cent, and Irish shares by 10.3 per cent.

Are we doing the wrong thing?

While the best returns may be from global shares, it would appear that the Irish may not be so crazy after all in putting so much of their money into property. While Irish property has underperformed other assets, the Dublin market gives global shares a close run for their money, returning 380 per cent since 1990.

However, the risk for Irish investors is that they are still overly concentrated in property and thus exposed to a potential crash as happened post-2008.

Data prepared by the Central Bank shows that, as of the end of last year, the net worth of Irish households rose to a record €727 billion, eclipsing the previous Celtic Tiger peak of €720 billion, reached in the second quarter of 2007. This means that household wealth, per person, is of the order of €151,657.

But is this improvement on the back of bullish global markets? No, according to the Central Bank. About two-thirds of the improvement in our wealth is due to rising property values, it says.

Further information from the Central Bank shows that, when it comes to household wealth, our homes account for a staggering 57 per cent of our assets, – with the balance of 43 per cent invested in financial assets, such as deposits, stocks, bonds, and pensions.

It’s high but it is still less lop-sided than back in the Celtic Tiger days; at the end of 2007, for example, some 67 per cent of the average Irish household’s wealth was tied up in their home.

Of our financial assets, Central Bank figures show that just 16 per cent, or some €284 million, were invested in shares and equity at end-2017, with a further 29 per cent, or €524 million, either on deposit or held in a foreign currency.

With returns on deposits now almost negligible, it shows that, even when we try and divert money away from our homes, we tend to opt for low return, low risk options, rather than taking a strategic approach to building long term wealth in the stock markets.

The mortgage free

One other nugget the survey throws up is the number of people who must be mortgage free by now. If you consider that house prices across the State have rocketed by 290 per cent – and by more in Dublin – since 1990, there are a lot of people who, on the back of strong earnings growth during this period, will have been able to take full ownership of their property.

The 2016 Census showed that, outside urban areas, almost half of homeowners don’t have a mortgage, while in urban areas such as Dublin, Cork and Limerick, the figure is close to a third, at 29.2 per cent – the highest level since 1991.