So, AIB has returned to the main stock markets after seven and a half years. Why should I care?

The initial public offering (IPO) of AIB is an important milestone for the State as it seeks to recover the €20.8 billion taxpayers have pumped into the bank during the financial crisis to keep the lender afloat as it struggled with spiralling bad loans.

By selling an initial 28.8 per cent stake in AIB to stock market investors on Friday for a total of €3.4 billion, the State has now recovered a total of about €10.3 billion in cash from the bank. That includes a repayment of €6.7 billion of capital pumped into the lender, plus interest payments and fees for Government guarantees during the crisis.

Was there much demand for the stock?

Yes, particularly from large investors, though appetite from the general public was more muted as small investors needed to commit at least €10,000 to get a slice of the action. Overall, the investment banks that were running the stake sale on behalf of the Government received orders for about €13.5 billion of stock – 4½ times the amount that was on offer.

Ordinary investors who put in an offer to buy up to €50,000 worth of stock will receive all that they sought and 53 per cent for amounts above that.

If there was such demand, why didn’t the Government sell more shares?

IPOs are typically oversubscribed by investors by a multiple of the stock on offer. The key in this case is to get the right types of investors on board. The Government had set its sights mainly on luring large pension funds and asset managers who intend to hold the stock for the long term and who would be the first port of call as it seeks to sell further shares in AIB in the future.

However, it would be important to also have some short-term orientated investors, such as hedge funds, on board as well, as they would be more inclined to actively trade the stock, ensuring that there’s enough supply and demand to create a proper market.

How have the shares performed after they floated earlier on Friday morning?

The IPO was priced overnight at €4.40 per share by the Government and its advisers, bang in the middle of a €3.90 to €4.90 range that had been outlined early last week before AIB’s management began a charm offensive with potential investors. The shares rose by as much as 7.7 per cent on Friday to just over €4.74.

Doesn’t that show that the Government left money on the table and could have squeezed more out of investors?

Well, yes. But the pricing of IPOs are always a balancing act. It’s important to note that the State continues to hold a 71 per cent stake in the bank and will need a healthy market for the stock over the coming years so it can continue to sell down its holding. If the stock had fallen, it would have left a sour taste in the mouths of investors, who the Government will be reliant on in future to buy further shares. If it had jumped by 20 per cent or more, it would have led to serious questions that that the deal had been underpriced.

If I buy shares now, can I expect the stock to continue to rise?

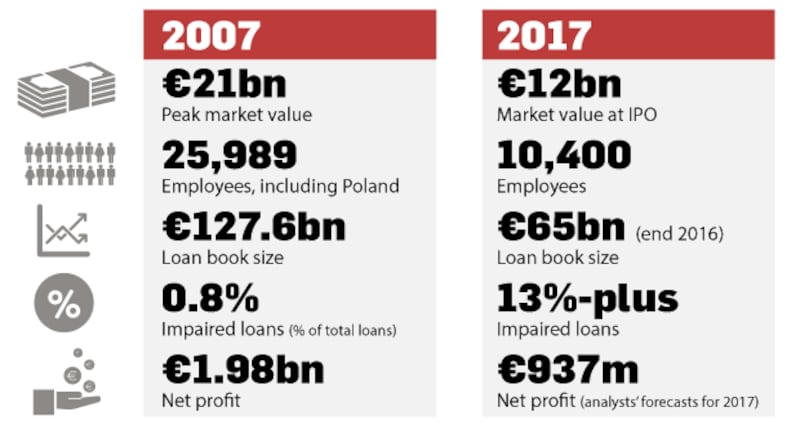

Not necessarily. The €4.70 share price that AIB rose to – valuing the bank at €12.8 billion – is in line with a target that was recently set by US investment bank Keefe, Bruyette & Woods for the stock, and also around the level at which analysts in general believe that its net assets will be worth at the end of this year. Expect to see a number of big research reports from stockbroking firms over the coming months. These will all set their own price targets.

With AIB back on the main market, can bankers look forward again to big bonuses?

A State-imposed ban on bonuses and a salary cap of €500,000 for top management at AIB has been in place since 2009, and the Government has made it clear that it has no intention of lifting either restriction. Bank of Ireland, which managed to avoid falling under Government control throughout the crisis, has a similar bonus restriction. However, it is inevitable over the coming years that executives in the country's banks will see long-term share bonus plans put back in place, as large investors like to see management with "skin in the game". Such schemes will likely have "claw-back" measures where bonuses can be retrieved in the event the company runs into trouble.

When will taxpayers recover all of the money that AIB owes?

Former minister for finance Michael Noonan has previously said that it could take up to a decade for the State to fully extricate itself from AIB. Having floated the bank on the main stock exchanges in Dublin and London, the State will be able to drip-feed shares onto the market in the coming years. It's possible that it will be outside of majority State control within three to five years.

What about the other surviving bailed-out banks? Are they a good buy now?

Bank of Ireland remains 14 per cent State-owned, and its market value is €7.6 billion. Its current share price, at 23.6 cent, is slightly below the average price target that analysts have for the stock, at 23 cent, according to Bloomberg data.

Permanent TSB is 75 per cent owned by taxpayers and its current share price of €2.90 is well below the €4.50 level of its IPO two years ago – serving as a cautionary tale to investors of how shares can go down as well as up. Analysts, on average, have a price target of €2.98 for the shares, suggesting some upside.

It is important to get independent financial advice when considering buying shares or making any investment.