Australian Fiona Arnold had no idea when she attended a party in Perth in February 1988 that she was about to meet her future husband, Sam, and follow him back to his native Ireland the following year.

“I just fell completely in love with him and that was it,” recalls Arnold, who ditched her job as principal harpist with the Western Australia Arts Orchestra to move here.

Sam was diagnosed with a low-grade brain tumour in 1991. However, he would be given the all-clear after treatment, and the couple would go on to marry and have a daughter. But the tumour re-emerged 20 years later in a more aggressive form, and he died in the Blackrock Hospice, Dublin, in August 2013. He was 49.

As Arnold coped with the loss, she also faced problems with a mortgage on their south Dublin home – not helped by the fact that they had relinquished life assurance polices while Sam was not working.

While the terms of the €400,000 loan had been eased a number of times, her lender (Start Mortgages, now owned by US private equity group Lone Star) wrote in 2015 to say her interest-only payment arrangement was no longer tenable.

After trying various avenues to find a solution, Arnold was put in contact last year with a personal insolvency practitioner, Gillian Creevey of AMI Financial Solutions in Dublin, who guided her through Ireland's fledgling insolvency regime. This resulted in her mortgage being cut to €308,000 and €112,000 of debts being written off.

“It’s given me an opportunity to start again,” the working mother said.

Financial crisis

The Insolvency Services of Ireland, set up in 2013, has delivered permanent deals for more than 5,000 debtors struggling under the weight of the financial crisis.

More importantly, its existence – alongside Central Bank of Ireland targets introduced in 2013 and pressure from the Troika – has served as a catalyst for banks to restructure almost 121,000 soured private home loans.

Banks and borrowers have been helped by a rebounding economy and housing market, and as the Republic’s unemployment rate fell over the past six years from 15.1 per cent to 6.4 per cent.

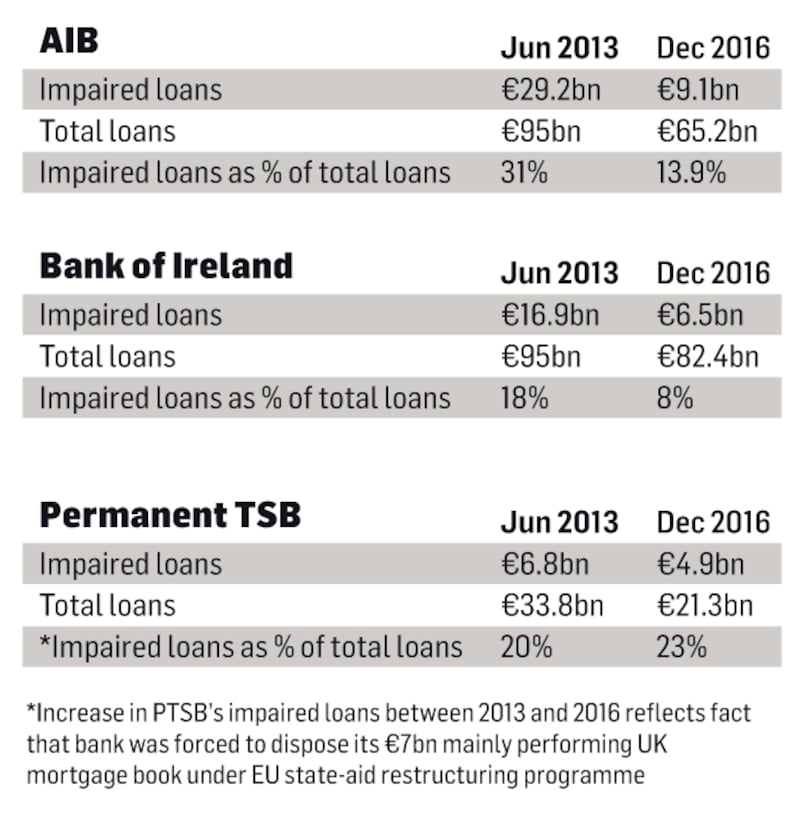

AIB, which has the largest loan book in the country, has seen its bad loans drop from €29 billion, or more than a third of all of its loans, in 2013 to €8.6 billion, or 13 per cent, as of the end of March. In the process its return to profitability since 2014 has been helped as it freed up €1.1 billion of provisions previously set aside for problem loans.

Many restructures – including term extensions, splitting mortgages into a part that borrowers can repay and a portion that is warehoused, voluntary sales and debt writeoffs – have proved less expensive than banks had originally provided for.

Lenders have managed to restructure loans to small and medium-sized enterprises (SMEs) at a faster pace in recent years, Ed Sibley, head of supervision of credit institutions at the Central Bank, said at a press conference on Wednesday.

While most SMEs in trouble during the crisis had property loans, banks have focused on carving up such borrowings into debt that can be carried by a viable business and real-estate debt, which, in many instances, has led to asset sales and some loan writeoffs.

Still, 10 years after the housing market hit the buffers, mortgage debt remains the main problem for banks. And progress is slowing.

More complex

AIB, which is preparing to float on the main stock markets in Dublin and London this month, highlighted in documents published this week that in the past year it has experienced “an expected slowdown in [loan] restructuring momentum as...it is now primarily dealing with those cases which are of lower monetary value, more complex, more specific to an individual’s circumstances and more protracted in nature”.

The problem is the European Central Bank’s banking supervision arm, which took charge of overseeing euro zone financial institutions in late 2014, is beginning to lose patience with lenders and countries across Europe with high levels of non-performing loans (NPLs).

While domestic banks have cut NPLs from an average of 27 per cent of their loan books in 2013 to 14.2 per cent at the end of last year, they remain well above the 5.4 per cent EU average.

Banking and supervisory sources have said that rather than set crude targets for institutions across the euro zone, given that different countries have different issues, they forced banks to come up with initial plans earlier this year to tackle the crisis.

AIB has said it aims to resolve most of its remaining €8.6 billion of NPLs within the next two to three years.

The bank and its rivals face repercussions if they don’t, including more intrusive supervision, demands that they hold more expensive capital in reserve, and restrictions on shareholder dividends.

AIB chief executive Bernard Byrne signalled to The Irish Times two weeks ago that while the bank would continue to work through individual loans, particularly with borrowers willing to engage, the pace may be accelerated by selling some loans to overseas buyers of distressed debt and companies seeking to take part in the State's expanded "mortgage to rent" scheme.

An increase in repossessions in Ireland, which have remained low since the outset of the crisis much to the surprise of overseas observers, is now "inevitable" as banks seek to resolve their remaining bad loans, according to Irish MEP Brian Hayes, who was minister of state for finance between March 2011 and May 2014.

Too much time

“We took our time trying to get the balance sheets of the banks right – probably too much time. But at the outset we didn’t have a personal insolvency regime in place. We are now left with people within the NPL numbers who can work through their situation and, equally, hard cases of people who have no chance of being able to get out.”

It was understandable during the crisis that an emphasis was put on keeping people in their homes

While mortgages in default, particularly early cases in arrears, have come down steadily in recent years, long-term arrears remain stubbornly high.

Cases of owner-occupier mortgages in arrears for more than 720 days accounted for 43 per cent of all problem accounts in March, and 90 per cent of the arrears balances outstanding, according to the Central Bank. That is four times the equivalent rate for buy-to-let mortgages.

Banks and home loan activists alike say that a slew of laws and rules introduced since the onset of the downturn – including strict waiting periods and procedures lenders must go through before seeking to take legal action – have exacerbated the long-term arrears problem, and in cases allowed some to avoid engagement with their banks.

“It was understandable during the crisis that an emphasis was put on keeping people in their homes,” Hayes said, particularly as it cost taxpayers a gross €64 billion to rescue Irish banks.

“But some people are not confronting the reality of their position. But it needs to be faced up to both by borrowers and the banks. As taxpayers we need to get our money out of the banks.”

He said overseas banks would not come into the market and drive down Irish mortgage rates as long as the situation continued.

Cultural issues

The cultural and political issues at play in Ireland around repossessing family homes are encapsulated in numbers from Bank of Ireland.

“Legal repossession of a property is a last resort where all other options have been explored,” a spokesman for Bank of Ireland said. “In the year 2016, we repossessed 132 properties. In the same year new forbearance was extended to 3,497 accounts.”

David Hall, head of the debtors advocacy group Irish Mortgage Holders' Organisation, is surprised that more repossessions have not materialised to date.

“My concern is that having all the banks condensed into a short timeframe to resolve things, it could become a lot more politically and socially acceptable to sell NPLs to vulture funds en masse.”

As of November, AIB had taken legal action against almost 7,000 of the 13,000 borrowers who are more than 90 days behind in repayments. However, over the past 12 months, Byrne said, one-fifth of these borrowers have subsequently re-engaged with the bank and sought to do a deal.

AIB also recently opened a new avenue, selling a €400 million portfolio of non-performing, buy-to-let property loans to Wall Street giant Goldman Sachs for half their original worth. Up until now the sale of mortgages had mainly been the focus of overseas banks retreating from the Irish market, such as Lloyds Banking Group and Danske Bank, and the liquidators of Irish Bank Resolution Corporation.

AIB is also known to be at the early stage of assessing the sale of another portfolio of as much as €1 billion of buy-to-let-weighted mortgages called Project Redwood.

Special purpose vehicles

In addition, banks are considering other ways to shift troubled loans off their balance sheets. Some are considering setting up special purpose vehicles (SPVs) that would house bundles of NPLs, according to sources. They would need to sell a majority stake in such vehicles to outside investors to reclassify the loans as no longer being on their books.

Potential investors would include the types of US private equity and hedge funds that have snapped up distressed assets in recent years.

Unlike direct loan sales, using SPVs would give banks an option to retain an interest in the assets and continue to service the loans.

Meanwhile, The Irish Times understands that some banks are beginning to assess the possibility of bundling portfolios of mainly NPL mortgages and selling bonds in capital markets, secured by the assets.

Lone Star and Oaktree affiliate Mars Capital have moved in the past seven months to refinance hundreds of millions of euro worth of mainly soured loans bought from Irish lenders in recent years through such so-called residential mortgage backed securitisation (RMBS) deals.

The banks would have to structure any potential RMBS deals off-balance sheet to be able to remove the loans from their accounts – or, as bankers like to phrase it, “derecognise” them. Again, the banks may remain the direct contact with borrowers after a RMBS deal.

Balance sheets

Loan sales, SPVs and RMBS deals may move the issue off banks’ balance sheets, but they remain problems for the actual borrowers – and the new owners of the debt.

“There are arguments as to whether selling loans en masse to vulture funds are appropriate or not, but from a borrower’s perspective, whether your loan is with a bank or has moved to an entity that you may not recognise, you have the same rights,” said Lorcan O’Connor, head of the Insolvency Services of Ireland.

“First, the owner of the loan can only do what your loan documentation permits. Second, whether the fund is based in Dublin, London or New York, whoever is servicing it on behalf of the fund must have a license here and adhere to strict Central Bank codes when dealing with NPLs.

“Third, there’s a statutory provision [in laws enacted in 2013] that a home owner asks a court to adjourn proceedings at any stage in order for them to be able to deal with a personal insolvency practitioner.”

Meanwhile, Hall's new venture, I Care Housing, and others, including a company called Arizun and a consortium led by investment firm Merrion Capital, are engaging with banks to see if they can buy thousands of loans that borrowers have no chance of repaying and who can qualify for the State's planned expansion of a "mortgage-to-rent" scheme.

Funding

Cathal O’Leary, chief executive of Arizun, said his firm has €500 million of funding from a major European financial institution, which he declined to identify, which would allow it to buy mortgages linked to more than 3,000 homes.

Arizun is targeting both debtors who would qualify for social housing and those that would not.

“We are determined to keep people in their homes and offer a long-term solution and remove all the debt, including arrears,” said O’Leary, adding that while the company intends to buy loans at deep discounts, many banks have already put aside more than enough provisions to cover this.

His deals would “release provisions for the banks as well as redeploying expensive capital for new lending into the economy”.

Fiona Arnold, meanwhile, is trying to get on with life. Her advice to others in similar situations is simple.

“Start engaging with your lender immediately and take the bull by the horns. It’s not the end of the world. You could be dealing with much worse situations. I know. I’ve been there.”