The European Central Bank (ECB) announced on Thursday that it was increasing its main rates by 0.5 percentage points, marking the first hike in euro zone official borrowing rates in 11 years.

Its deposit rate, the rate commercial banks have to pay the ECB for excess deposits they store with the Frankfurt-based bank, has moved from minus 0.5 per cent to zero, while its main lending rate, which has been at zero since early 2016, will increase to 0.5 per cent. It also confirmed that further rate increases are on the way.

The ECB, led by Christine Lagarde, is the last major western central bank to move to raise rates to try and fight a recent spike in consumer prices globally. Inflation is being fuelled by a number of factors, including the trillions of euros that central banks pumped into markets during the Covid-19 pandemic to avert financial meltdown, an uneven reopening of economies ever since, and the effects of the war in Ukraine, which have turbocharged energy and food prices.

[ Borrowers could be facing into a season of rapid ECB interest rate hikesOpens in new window ]

[ ECB raises interest rate by 0.5 of a percentage pointOpens in new window ]

The Bank of England has raised rates five times since December, leaving its base rate at 1.25 per cent, with economists are betting that it will increase the cost of borrowing by another 0.5 percentage points next month as UK inflation hit a 40-year high of 9.4 per cent in June.

READ MORE

On the other side of the Atlantic, the US Federal Reserve has been raising rates since March. This has contributed to a recent advance by the dollar against the euro which saw the two currencies temporarily reach parity last week for the first time in almost two decades.

Why is the ECB raising rates when there’s so much talk of a European recession?

The ECB’s primary objective is to maintain price stability, which it sees as having an annual inflation rate of about 2 per cent over the medium term. As of last month, euro zone inflation was running at a record 8.6 per cent, driven by energy prices. The big fear is that inflation will become embedded in the economy, as wages chase cost-of-living increases.

There is a major concern that a combination of central bank rate hikes and households and businesses cutting back on discretionary spending, as their running expenses are rising, may tip the economy into a downturn. Indeed, Bank of America said this week that 86 per cent of global investors now expect Europe to slump into recession in the next 12 months.

But, for now, the focus is on taming inflation.

How high will ECB rates go?

The ECB said on Thursday that at future governing council meetings, “further normalisation of interest rates will be appropriate”. This means only one thing. Financial markets are forecasting that the official deposit rate could reach 1.4 per cent by the end of next year – which implies that the key lending rate will be about 1.9 per cent, if it moves at the same pace.

What does Thursday’s rate hike mean for my mortgage?

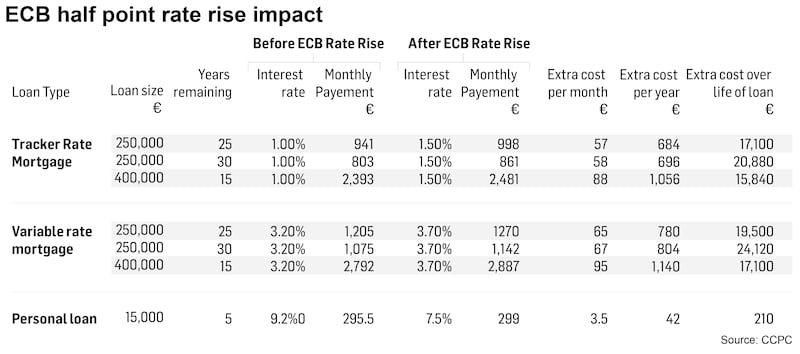

If you have been one of the lucky ones to have managed to get – and hold on to – one of those tracker mortgages that banks were doling out before the financial crash, you face an immediate increase to your monthly payments, for the first time since 2011.

So, for a tracker loan that is priced at one percentage point above the ECB rate, a 0.5 point move would move the rate to 1.5 per cent. There are still about €25 billion of tracker loans outstanding in Ireland, with buy-to-let borrowers accounting for about €3 billion of these.

A lot of savvy borrowers have moved in recent times to fix their mortgages over the long term to remove uncertainty over borrowing costs. For example, borrowers can currently fix their rates at as low as 2.5 per cent for 25 years, if their loan is worth less than 60 per cent of the value of their property.

However, it is likely that new fixed rates will increase in time. Indeed, some of the State’s non-bank lenders have already started hiking short- to medium-term fixed rates, because their own borrowing costs in financial markets have been rising recently in anticipation of the ECB move.

Because Irish standard variable rates (SVR) are fairly high already – with the average new such loan priced at 3.66 per cent in May and as high as 4.5 per cent in the case of Bank of Ireland – observers see little reason for banks to increase SVR costs for now.

What about other rates?

Banks will be expected to review their various business and personal loan rates for new loans in the coming period. But as variable personal loan rates are fairly high, with three-year loans, for example, ranging between 6.5 per cent and 14.3 per cent across the main Irish lenders, observers don’t see much movement upwards in the near term at least.

But haven’t I read headlines recently that Irish banks will be among the winners across Europe from rising ECB rates?

You have – but the main driver, initially at least, will be banks’ deposit books, not their loan portfolios.

As we all know, Irish mortgage rates are much higher than the average rates across the euro zone. This is largely down to the fact that the State’s lenders must hold much higher levels of expensive capital in reserve against home loans than most peers as legacy of the Irish property crash and arrears crisis.

Analysts expect that Irish banks’ profits will rise in the coming years on the back of rising ECB rates (barring an economic meltdown resulting in a spike in bad loan losses). This will will be driven by fact that the ECB will no longer charge banks negative rates for their excess deposits. Bank of Ireland and AIB’s combined deposits were €50 billion more than their total loans at the end of March, which had been turbocharged by household savings during the Covid-19 pandemic.

While most depositors in Irish banks have been shielded from the ECB’s negative rates policy in recent years, they have been earning nothing on money in their current or deposit accounts. That is likely to remain the case for the foreseeable future, even as the ECB moves its deposit rates well into positive territory. That’s because banks continue to have way more customer deposits than they need.

Customer deposits in excess of €1 million at AIB and Bank of Ireland are currently being charged negative rates. However, Bank of Ireland said on Thursday that it will cease this practice as of next month, lifting rates on about €15 billion of its deposits to zero.

Analysts at Deutsche Bank suggested in a recent report that while average Irish mortgage costs will rise over time, they may not be at the pace of ECB rates. They also said that it is likely that the difference between Irish new rates and the euro zone average will narrow over time.

This has already been happening as most European home loans are priced off market borrowing rates, which have ben rising ahead of ECB moves.

The average new Irish mortgage rate stood at 2.73 per cent in May, compared to 1.76 per cent across the euro zone. But while Irish rates had fallen by 0.07 percentage points over the previous 12 months, wider euro zone rates had increased by 0.49 points.