It’s the big story of the autumn and yet, for dispirited savers across the State, rapid increases in European interest rates have yet to translate into a greater return on deposits.

Since July, rates have ramped up from zero to 2 per cent, but savers have seen no discernible improvement in the rates on offer to them.

According to figures from the Central Bank, rates for term deposits for Irish household savers did rise in September, but only to 0.17 per cent, from 0.06 per cent in August. This is substantially below both the ECB rate and the EU average, which was 0.69 per cent in the same month.

And it’s not just an issue in the Republic; in the UK for example, where Bank of England interest rates have jumped to 3 per cent, it has been claimed that savers have missed out on some £6.8 billion (€7.8 billion) in interest payments as banks have – as of yet – failed to pass on recent rate hikes.

READ MORE

Savers are doing well on one front – negative rates appear to be largely on the way out, with AIB, for example, abandoning its policy back in August, but that is of little interest to ordinary savers, as negative rates tended to apply only to seven-figure sums.

So what’s going on with deposits?

If you’re looking for a guide as to where savings rates currently are for Irish savers, consider AIB’s move back in October. It is one of the few announcements related to savings of late and will see the bank launch a new one-year fixed-rate product from the end of this month.

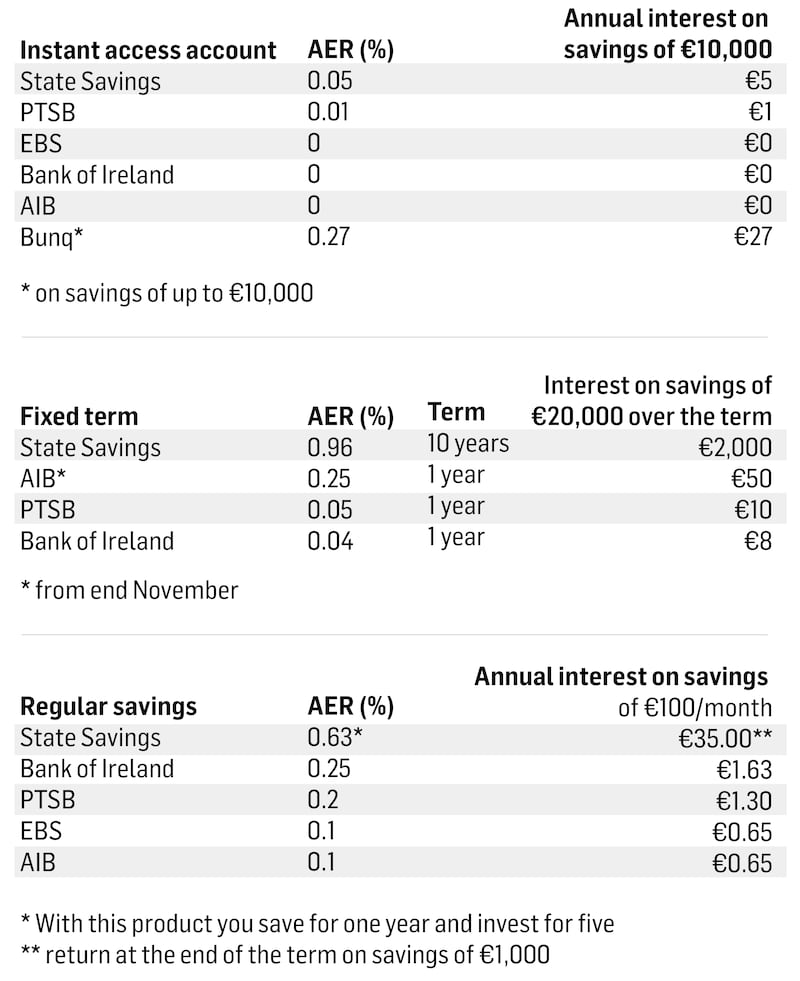

If you save on a regular basis, the best rate available is 0.25 per cent (Bank of Ireland). For instant access, forget about it

However, that launch is unlikely to generate too much excitement, as it offers a return of just 0.25 per cent on savings in excess of €15,000. This means that savings of €50,000 will earn a return of just €125 a year at a time when inflation is running at a multiple of that, eating into the value of your money.

Even with that, once this product hits the market, despite a rate which substantially lags European rates, it will be a rate leader in the Republic.

Best rate

As our table shows, if you are willing to lock your money away for a fixed term, the best rate you can currently get with a bank is a miserly 0.05 per cent with Permanent TSB, which will earn you just €10 a year on savings of €20,000.

If you save on a regular basis, the best rate available is 0.25 per cent (Bank of Ireland). For instant access, forget about it. Bunq, as discussed below, does offer a rate of 0.27 per cent but only on deposits of up to €10,000.

The only way, then, to get close to 1 per cent is to put your money into a 10-year State Savings product, which offers an AER (annual effective rate) of 0.96 per cent, which means a payout of €1,000 on savings of €10,000. While this may at first appear unattractive given the likely future direction of interest rates, you can end the term early and you won’t incur a penalty.

No wonder, then, that State Savings has grown even stronger as a player in the savings market. State Savings currently accounts for 8.6 per cent, or some €20 billion, of the State’s gross national debt (€232.2 billion) as of end October 2022, up by €400 million from the end of 2021.

The reason for such derisory levels of compensation currently on offer for savers is a general lack of market competition, combined with banks already having substantial sums on deposit.

First of all, the number of providers offering a deposit facility has plummeted. The issue has been compounded by the fact that both KBC Bank and Ulster Bank – arguably two of the more competitive financial services providers – are in the process of shutting up shop in Ireland.

This leaves just three – yes you read that correctly, just three – banks offering a range of savings products – AIB (plus EBS), Bank of Ireland, and Permanent TSB. While An Post has a current account, a spokesman confirms that it doesn’t offer deposits itself, but does supply the NTMA’s State Savings products, the only other savings option available on the market.

So why would banks pay significantly more than their competitors?

[ Sign up for our new personal finance newsletter On the MoneyOpens in new window ]

Expect a lag

Diarmuid Sheridan, financials analyst with Davy, says savers should expect a lag between ECB increases and an equivalent impact on Irish deposit rates, given that Irish deposit rates (for most people) didn’t go as low as they could have done with the move to negative rates in recent years.

Another factor is that banks simply don’t need more deposits at present. Yes, banks are funding more from deposits, but outstanding loans have fallen at the same time as household deposits surged during the Covid years.

“Over the last 20-plus years, we’ve never seen that amount of liquidity in the Irish banking system,” says Sheridan, noting that banks now have “an awful lot more deposits than loans”.

At Bank of Ireland, for example, customer deposits increased by €1.3 billion to €94.1 billion between the end of December 2021 and June 30th, 2022, while AIB has €96 billion in retail deposits, up by €3 billion in the six months to the end of June.

However, over time, this plentiful liquidity is likely to change. Sheridan notes that as mortgage rates start to rise, deposit rates will follow. Bank of Ireland has just pushed its mortgage fixed rates up by a quarter of a percentage point, still well below recent ECB hikes, following rival AIB, which increased its fixed rates by half a point in October.

“The two go in tandem,” Sheridan says, adding: “The time will come, clearly, when they will need to [increase deposit rates] but it’s very difficult to see it in the next 12 months.”

New arrivals

Against this background of larger players departing Ireland, the Irish market has seen the arrival of some new, smaller niche providers such as Avant, which operates predominantly in the lending/mortgage market, and fintech operators such as Revolut and N26, which mainly offer payment services.

However, a decent deposit facility offer is not a short-term priority, it would seem.

The most recent arrival, Bunq, does offer interest on your deposits, and it’s one of the best rates around. However, it’s paid only up to a certain limit

The largest of the new arrivals, Revolut, does not pay interest on money held in its savings accounts, known as “vaults”, a spokesman says, although it does in other countries such as the UK and Poland. Does it have plans to do so in Ireland? It wouldn’t say.

Not so long ago, German bank N26 used to charge savers for holding their money. It had a fee of 0.5 per cent on deposits in excess of €50,000, although this was abolished in July of this year.

The changing interest-rate environment means that it is now considering a change of approach, and a spokesman says that a savings-with-interest product “is one of many features that we are exploring that could feature in our roadmap in the future”.

The most recent arrival, Bunq, does offer interest on your deposits, and it’s one of the best rates around. However, it’s paid only up to a certain limit, so is not as attractive as it may first appear.

According to a spokeswoman for the Dutch based provider, back in September Bunq increased the interest it pays on savings to 0.27 per cent. But this rate applies only to the first €10,000.

Credit unions

Another option for your savings is in your local credit union. But here, as elsewhere, you won’t find much of a return.

The Public Service Credit Union, for example, cut the rate of return on its demand deposit account to zero during the summer. Not only that, but you might have a challenge to find a credit union that will actually accept your deposits.

When interest rates shrank to historic lows and credit union members showed themselves reluctant to borrow, credit unions across the State started to impose limits on the amount of savings customers could hold with them. For example, St Francis Credit Union in Ennis, Co Clare, has a limit of €20,000 on savings, while First Choice has a limit of just €10,000 for new members.

The reasons for this were multiple but they include the fact that regulatory rules require credit unions to allocate and hold an additional 10 per cent of the value of all members’ savings in their capital reserves. So for every €100,000 of members savings received, the credit union must allocate €10,000 from their surplus to their capital reserves.

Credit unions were finding that they were then being charged by banks to hold these reserves, with many banks imposing negative rates in recent years on deposits in excess of a certain amount. Will this change as interest rates start to rise again? Not so fast, perhaps.

According to David Malone, chief executive of the Irish League of Credit Unions, “some credit unions may potentially increase their savings caps. However, this will be a decision for each individual credit union to consider.”

Next week: What to do with your savings