Much of today’s economic and financial discourse revolves around the impact of new technology on our lives, as if this were something new. But it’s not. The repetitive economic cycle is also old as the hills, as is speculation.

If you doubt this think about the Book of Genesis. Remember when Pharaoh awoke petrified by a dream? He dreamed he saw seven cows, “attractive and plump”, feeding by the Nile. But soon these beasts were followed by seven skinny, ugly cows, which proceeded to eat the fat cows.

Terrified, Pharaoh called for Joseph, who explained that the dreams represented the fact that seven years of plenty tends to be followed by seven years of famine. The cows represented the good times followed by the bad times. Joseph urged Pharaoh to set aside food in the good times, to feed the Egyptians when things turned down.

There in Genesis is Joseph, the first truly prudent finance minister, explaining a seven-year economic cycle, the type of which we are well used to in the western world. And, as we have these cycles, we also have people who are willing to speculate on the future trend of the economic cycle, or on new technology that will affect the trend.

For centuries speculation was forbidden in religious teaching because of what it did to human nature: it fuelled greed and fear, both of which are destabilising

Historically, because humans are social animals, and we tend to behave like a herd, religious leaders have regarded as highly dangerous anything that has driven the herd or the flock to extremes.

Speculation is one such danger, and for centuries speculation was forbidden in religious teaching precisely because of what it did to human nature. Speculation fuelled greed and fear, both of which are inherently destabilising.

As a result St Thomas Aquinas preached about the “just price”, whereby a “good man” shouldn’t knowingly sell anything for more than it is worth. Under no circumstance should he lend money for interest to anyone else to bet on the cycle.

Undermining rationality

For St Augustine, speculation – which he termed "appetitus divitiarum infinitus", or the unlimited lust for gain – was among the deadliest of the seven deadly sins. But humans love financial speculation.

The world "speculation" comes from the Latin "speculari", which means to be on the lookout for trouble. Even the Roman forum had a corner reserved for the speculari. These lads (and lassies) have long dominated markets, manipulating human nature and undermining rationality in pursuit of riches.

New technology always attracts new speculators because of its ability to influence the trend of the economy. When money is cheap the incentive to borrow, to drive up prices and sell on to the next guy, pocketing the difference, is always with us.

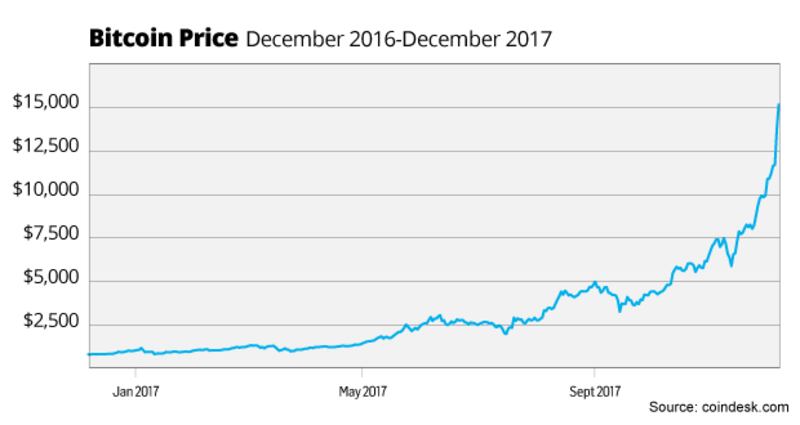

Think about what is happening with Bitcoin. The price of the cryptocurrency is rocketing based on the notion that it will ultimately replace money as we know it. This may or may not happen. But Bitcoin’s price has risen by 1,525 per cent this year.

Or consider speculation on the share prices of technology companies, some of which have yet to make a profit but are valued at billions of euro. Some will end up delivering, but many won't. Amazon's share price is up 55 per cent this year; that of its Chinese equivalent, Alibaba, is up 99 per cent.

Once speculative mania takes hold all sorts of people who normally remain aloof from these episodes are tempted to get involved on the promise of quick riches.

We’ve seen down the ages mass speculation in technologies: canals, railways, electricity companies, cars, radios and, most recently, the dotcom boom and crash. All these technologies changed the world, but fortunes were made and lost betting on precisely how, when and in what form the change would take place.

The speculator typically starts with a little money and hopes to make a lot, quickly. The investor starts with a lot of money and hopes to make a little more, slowly

There is a huge difference between speculating and investing. The speculator typically starts with a little money and hopes to make a lot, quickly. The investor, in contrast, starts with a lot of money and hopes to make a little more, slowly.

All boom-and-bust cycles tend to follow similar paths and are always, as now, underpinned initially by low interest rates and cheap credit. The most expensive four words of all are: “This time it’s different.”

To understand the credit cycle better we must reject classical economics, which takes the irrational human out of the equation, and recognise the importance of the human propensity to panic, indulge in herd behaviour and believe our own propaganda.

From euphoria to panic

Credit booms go in stages. Punters oscillate from optimism and euphoria to depression and panic – a journey that leads to the destruction of wealth. Most people are what is known in financial markets as “momentum investors”, who follow the crowd, buoyed up by the excitement of it all, rather than “value investors”, who are constantly asking themselves whether prices are reflecting real value or something else.

The predominance of momentum investors has the effect of amplifying the high and low points of cycles.It is this sort of behaviour that leads to bubbles and can also push the economy out of kilter for long periods. It is simply not true, as classical economics contends, that the self-interested economy naturally rights itself and finds equilibrium.

In fact the opposite is the case. The self-interest of banks, market players and leveraged speculators can produce long inflationary periods or leave us stuck in stretches of unemployment and deficient demand. We know this in Ireland too well.

Panics can also be sparked by relatively trivial events, and the financial system can move very quickly from a position of rude health to one of fragility. The great American economist Hyman Minsky identified five stages of a credit crisis: displacement, boom, euphoria, profit-taking and panic.

At the beginning something real happens to disrupt the old order. This can be a monetary event, such as quantitative easing, or an innovation, such as the internet, Amazon or Uber.

For example, since 2008 central banks have pumped trillions of dollars into the financial system. This was the displacement moment. As interest rates fell, those with money decided to punt – and, as ever, asset prices rose as more people speculated.

In the years up to 2014 the US stock market posted double-digit gains consistently. This boom has led to gearing, as banks fall over themselves to get involved. This process drives prices ever higher. Balance sheets play tricks on both lenders and borrowers. But success breeds a healthy disregard for the chances of failure.

During the euphoric stage people emboldened by previous gains drive up the prices of ever more esoteric assets. The Bloomberg Wine & Cheese index is up 34% this year

During the euphoric stage, leverage amplifies prices and people emboldened by previous gains drive up the prices of more and more esoteric assets. A favourite of mine is the Bloomberg Wine & Cheese Index, which measures the prices of posh cheese and wine. It is up 34 per cent this year.

The giddiness in the euphoric period is also reflected by people investing in places they can hardly locate on the map. In the past 12 months the stock market of Vietnam rose 43 per cent, driven largely by Americans.

We then move towards the profit-taking period, as some some savvy players take these lofty levels as a signal to cash in their chips. A prescient few take profits.

We are already seeing this in the US stock market, which has run out of steam and is now trading sideways. Typically, this begins the process of unravelling. When the herd realises that prices are falling everyone rushes for the door, in panic. The edifice collapses, fortunes are lost, and we start again.

The five-stage cycle can take time to play out, and it never runs exactly the same as in previous cycles. But the five stages remain a handy model for analysis. You might want to speculate what stage the Dublin commercial-property market is at.

The essence of a credit cycle is a build-up of debt combined with old-fashioned human nature fuelling humanity’s pathological optimism as we end up believing our own propaganda.

As today’s financial markets go ever higher, and the gap between valuation and prices becomes more and more stretched, it would seem injudicious to ignore the repeated warnings from history and overlook our capacity for individual and collective self-delusion.

As we approach Christmas, maybe it’s time to go back to the Bible and scripture to get a clear sense of the future.