Ted Duggan endured a tough decade since losing his pub business. For years, the Co Meath man ignored his debts until a friend suggested he seek help to find a financial solution.

Duggan said that image of people drowning in debt in the television adverts run by the Insolvency Service of Ireland (ISI) was "very close to the mark" for what he went through.

“I just didn’t do anything about it. I was too afraid of the consequences of what will happen and where the hell am I am going instead of taking the bull by the horns,” he said.

Ted, a man in his late 50s, lost his pub in Clonee in 2012, the same year the government passed the Personal Insolvency Act, groundbreaking legislation enacted in the wake of the financial crash aimed at lifting the burden of debt from tens of thousands of mortgage holders.

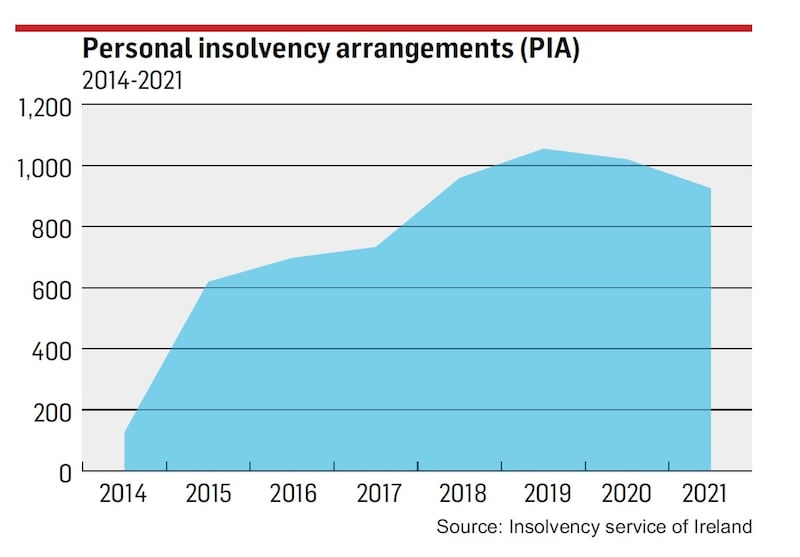

Now, a decade on, Duggan is among people who until the end of last year had benefited from 6,134 personal insolvency arrangements, the mechanism created under the Act that restructures or writes off mortgage and personal debt to give struggling borrowers a fresh financial start.

While recent PIAs such as the €2.9 million debt write-off approved for musician Frank McNamara and his wife Theresa Lowe – or the failure of the €13 million PIA proposed for restaurateur Jay Bourke this month – generated many headlines, the vast majority of the financial rescue deals agreed, inside and outside the courts, benefit everyday people such as Ted Duggan.

Letting down your family

For a long time, Duggan wouldn’t even contemplate going down the “PIA” route.

“It was always in the back of my head but a lot of it would have been down to fear: I didn’t want to go through the system; you don’t want to be a failure; you don’t want to be letting down your family,” he said.

But his health suffered from the stress; it hospitalised him three times with leg ulcers.

Even now, there is a stigma associated with financial difficulty and what he went through. He is reluctant to talk because the whole experience was “very hard” on his wife, whom he describes as “a rock”, but he is keen to get the message out: it is important to seek financial help.

“The only reason I am expressing this is that if it only helps one other person, if I thought it would take the stress out of somebody else, an ordinary person like me,” he said.

Seeing his pub business fall into decline, falling behind on payments to creditors, being “haunted” by solicitors chasing debts and living with more than €1 million in debt, Duggan said the whole period was “absolutely terrible”.

“When things changed, I didn’t change,” he said, summing up his financial decline.

The landlord of his pub put him in touch with a financial adviser who in turn recommended he contact Mitchell O'Brien, a personal insolvency practitioner based in Dungarvan, Co Waterford, who helped him take that bull by the horns.

“He was straight to the point; he didn’t give me any high hopes,” he said.

Duggan remembers well the day in November 2021 when he received the email from O’Brien telling him: “Congratulations, your personal insolvency arrangement has been approved.”

“They were lovely words; I kept looking at the email,” he said.

The original intention of the Act – to restructure debts and allow people stay in their homes – worked in Duggan’s favour. Debts of more than €740,000 were written off but, crucially, the €828,000 mortgage on the family home was written down to the current market value of €585,000.

Monthly repayments were lowered to a level that would not see Ted and his wife living below reasonable living expenses. This meant moving to interest-only repayments and extending the loan out to when Ted would be in his 90s. This was past the age of average life expectancy, but his main lender Start Mortgages approved the plan at a creditors’ meeting. Now Duggan and his family can stay in the family home with a sustainable level of debt and a protected income. Most importantly, it draws a line under the calls from debt collectors.

“It brings down your blood pressure,” said Duggan of the PIA’s approval.

All about the family home

“Anyone could have dealt with Ted’s debt issues; the challenge was to deal with the debts, while securing the family home,” said Mitchell O’Brien.

"The real difference between bankruptcy and a personal insolvency arrangement is that once a PIA is approved, the home has been secured. This can't be guaranteed in bankruptcy or insolvency schemes in other jurisdictions such as the IVA [individual voluntary arrangement] mechanism in England and Wales. In Ireland, it's all about the family home."

For many, long-term problem mortgages are not going away. The latest Central Bank statistics show there were 21,675 home mortgages in arrears of two years or more at the end of last year. Add all arrears cases, including people who fell behind in more recent times, and the figure rises to 47,062. A further 66,590 mortgages on homes were classified as restructured but 31 per cent of these were "split" with part of the debt "warehoused" to be dealt with at a later date.

These figures should make the once-in-a-lifetime PIAs more relevant as solutions to Celtic Tiger-era mortgages that are simply never going to be repaid due to age and income challenges.

Practitioners say, however, the PIA machine has slowed dramatically in the past two years. The Covid-19 pandemic carries a lot of the blame: it has led to payment breaks and Government income supports for borrowers and shut down the repossession courts for two years where legal actions by creditors might have forced some to seek more PIAs as a solution to their debt problems.

Disruption to the courts has delayed “section 115a” cases where debtors challenge a creditor’s veto against PIAs at a creditor meeting. Their number has fallen by 30 per cent to 282 in 2021.

The sale of non-performing loans by the banks to investment funds has also increased, reducing enforcement action for now. The exit of Ulster Bank and KBC will increase these sales.

Overall, the number of PIAs approved in 2021 – 925 in total – fell below 2018 levels.

Never been busier

ISI director Michael McNaughton said the number of people setting out to seek financial help was down 40 per cent on pre-Covid levels, while approved PIAs were down 12 per cent. The more active personal insolvency practitioners, who account for most PIAs, have never been busier.

Overall numbers may be down, but creditors have become more engaged and "more accepting of the system," said McNaughton. He says the traditional creditor versus debtor relationship has become less adversarial as the regime has bedded down with the system maturing and most of the players, with several notable exceptions, becoming more constructive to finding solutions, knowing the High Court rulings setting precedents on large-scale debt write-downs.

“It is dawning on creditors that it is more efficient and cheaper than the courts process with endless court appearances and all the costs that go with that,” he said.

McNaughton points out that lenders are even advising struggling debtors to talk to personal insolvency practitioners (PIPs), once regarded as adversaries, to see if they can help them find solutions, something that would have been unheard of 18 months ago. “That is another sign that the system is maturing. Creditors are not as suspicious or afraid of it as they once were,” said McNaughton.

Last month, Start Mortgages, one of the more constructive creditors embracing personal insolvency regime solutions, sent out a letter recommending a list of seven so-called PIPs, a group of financial advisers who are responsible for the vast majority of PIAs approved in the system.

McNaughton said the more engaged approach has meant that about 68 per cent of all people who sought help through the insolvency system were finalising PIAs against a first-time historical conversion rate of about 50 per cent for debt agreements.

While Covid stymied the work of the courts, pandemic-induced changes in work practices have helped. KPMG debt adviser John O'Callaghan, chairman of the Association of Personal Insolvency Practitioners, said remote meetings had allowed PIPs meet banks and the banking industry more to work on constructive solutions and become less adversarial.

“Zoom helps. Bankers do not like going into a room with enemies. Anybody will go into a Zoom with anybody – nobody is going to throw stones,” he said.

Further tweaking

Even after a decade in operation, the regime requires further tweaking. McNaughton said the ISI wants to make the system “more efficient and less legalistic”, for example by allowing the ISI to take on the administration of issuing protective certificates – the stop-the-clock measure triggered by debtors at the start of the insolvency process – rather than leaving this with the courts.

It also wants the Government to deal with the issue of “excludable debt” in PIAs where certain debts, usually tax debts due to the Revenue, are excluded preventing a universal debt solution.

A review of the 2012 Act has been sitting on the Minister for Justice’s desk since 2017. The Minister Helen McEntee has promised the sector she will look at the suggested reforms.

John O’Callaghan believes legislative changes improving the personal insolvency system needs to be pushed through, as people will be struggling with higher levels of unsecured debt as they may have prioritised mortgage payments over credit-card bills during the pandemic.

“All that needs to be handled. The legislation does need to come through to assist us, but the signs are all good and the movement is in the right direction,” he said of the system as it stands.

With the demise of his pub business, Ted Duggan has retrained as a bus driver. His advice to others who are shouldering long-term, heavy debts is to deal with the problem and seek help.

“Take the ostrich’s head out of the sand. Take it head on. That is what happens a lot of people. I am no different to anyone else,” he said.

“For a long time, I had my head in the sand. I was hoping it would go away.”

Now, 10 years later, for Ted Duggan it has.