If you bought a home in Ireland of late, you’re unlikely to think you got a bargain. It may surprise you, then, to learn that despite continued growth in Irish property prices, the European Commission says Irish house prices are significantly undervalued. Yes, in its latest statistical analysis, the European Commission says Irish house prices are undervalued by about 17 per cent.

Not only this, but they are considerably out of whack with the European Union; houses are overvalued in half of the countries in the EU.

So does this imply that Irish property prices still have some way to go? We take a look at what the data might mean.

European house prices

Earlier this month the commission released a number of documents as part of its autumn economic forecasts, including one on the housing market. It found that house prices across the economic area are continuing their “dynamic upward trend” since 2013, and rising sharply.

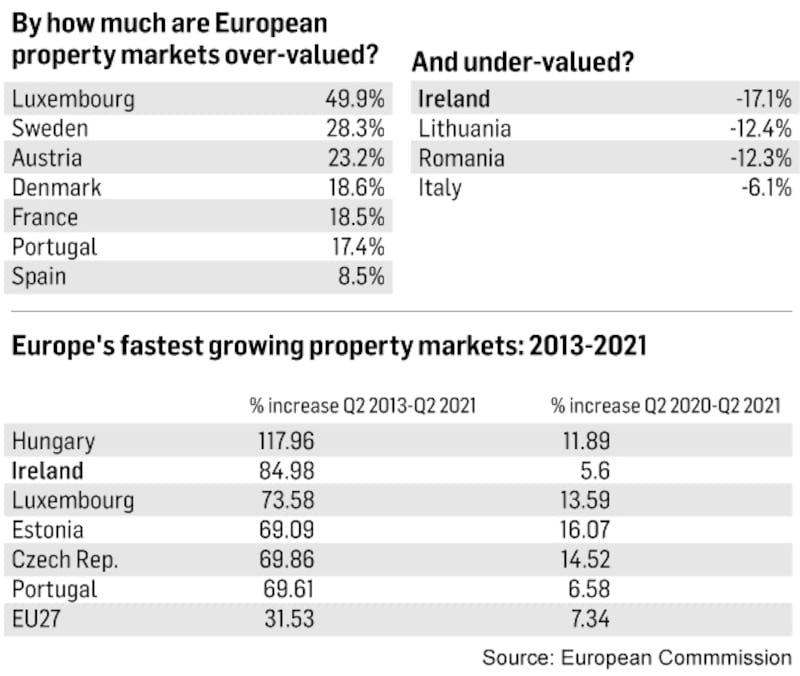

Indeed, house prices across the EU27 area are up 32 per cent between the second quarter of 2013 and the second quarter of 2021. German prices were 51.4 per cent above their mid-2013 values, compared with 40.1 per cent for Poland, 33.4 per cent for Spain, and 13.2 per cent for France. Prices decreased 7 per cent in Italy, and remained broadly stable in Greece and Cyprus.

It is Ireland however, where prices have risen at the second-fastest rate in the EU27, up 85 per cent since 2013 and second only to Hungary, where prices have rocketed by about 118 per cent.

No surprise there, perhaps.

But what might be surprising is that current price rises in Ireland continue to lag those seen across Europe – and often by a significant amount.

According to the data, price growth has ramped up in recent months, buoyed by a surge in pandemic-fuelled demand.

According to the commission, the sharp growth in house prices is being driven by “sustained demand backed by economic growth, historically high household savings and low interest rates”, while supply has been impacted by “limited construction activity”. It expects demand to remain strong, buoyed by accumulated savings and demand for increasing living space to accommodate new working habits such as working from home.

Indeed, of the total increase in prices that occurred in the EU since 2013, nearly one-fifth took place in the last 12 months alone. Prices grew at their fastest pace since 2013 in the second quarter of this year, up 7.3 per cent year on year.

And Ireland, with annual growth of 5.6 per cent in the year to June 2021, is far from one of the fastest movers. The largest increases were observed in Estonia (16.1 per cent); Denmark (15.6 per cent); and Luxembourg (13.6 per cent). However, Ireland has since started to catch up, with growth of 12.4 per cent nationally in the year to September, according to the latest CSO figures.

The overvalued – and undervalued – markets

With such sharp rates of growth – and even though the fundamentals behind house price growth may be strong – the commission says house prices are in fact overvalued in about half of EU countries.

It finds Luxembourg’s housing market the most overvalued across the EU27, with an average valuation gap of about 50 per cent.

It is followed by Sweden, where house prices are overvalued by 28.3 per cent; Austria (23.2 per cent); Denmark (18.6 per cent) and France (18.5 per cent).

Ireland is one of the few EU countries – along with Lithuania and Romania – where property markets are deemed to be undervalued, which puts Ireland, and its undervalution of some 17.1 per cent, significantly out of line with broader European trends.

And the trend has continued into 2021; separate figures from the European Central Bank suggest Irish house prices were undervalued by about 12 per cent in March, down from 13.7 per cent as of end-2020.

Such an undervaluation would imply that there is plenty of scope for Irish house prices to rise further.

As Austin Hughes, chief economist with KBC Bank, notes, the commission’s analysis implies that Irish house prices should be about 30 per cent higher than they are now.

So what’s going on?

Well, first of all, there is the method for calculating the data.

According to a spokesman for the commission, the Irish figure is based on a calculation involving average household income growth and the long-term average of house prices, and they also note that such calculations have “limitations”.

While none of these methodologies is perfect, “they provide an overview of recent house price developments compared with the past”, the commission says.

In the past, however, the commission’s approach has spotted the trends. In 2005, for example, it said Irish property was overvalued by 31.3 per cent, while in 2010, it said that Irish property was almost accurately priced, with a 3.5 per cent overvaluation gap.

However, there may be some factors behind the current “undervaluation”.

First up is the scale of the country’s house price crash following the financial crisis.

“Unlike most other European countries, there are relatively few countries where prices are still below 2008 levels,” says Hughes.

This means that when long-term average of prices is considered in a model, it would suggest that Irish prices still have some way to rise.

Latest figures from the CSO for September show that Irish house prices are still 7.4 per cent lower than their highest level in 2007, with Dublin prices 13.8 per cent off the February 2007 peak, and prices outside of the capital, 9.5 per cent lower than their May 2007 peak.

Secondly, according to Hughes, another factor is the introduction of macro prudential rules in Ireland.

The long-term averages of the price to income ratio, and recent growth in incomes, would suggest there is plenty of scope for house buyers to borrow more – after all, back in 2007 borrowing five times income would not have been in any way unusual.

These days, however, it has slid back to just 3½ times income under the Central Bank rules.

“This means a break in the series in the relationship between income and house prices,” says Hughes.

Affordability

But the data also points to differences at a “macro” and “micro” level.

At a macro level, the fundamentals may point to “cheap” Irish property, but at an individual, or micro level, affordability is biting hard.

Hughes notes that recent house price inflation relative to average earnings growth is already straining affordability metrics for “average” buyers.

As he notes, based on the Central Bank’s 3½ times income multiple, a single first time buyer (FTB) on average earnings of just over €44,000 would be able to borrow only in the region of €155,000, which means they would need a deposit of a staggering €163,000 to reach the average national home price of €318,000 paid by FTBs in September.

A couple, on the other hand, on average earnings, would need a deposit of about €117,000 to buy the average FTB home in Dublin, which came in at €425,700 in September.

So the likelihood is, says Hughes, that most purchasers will be those earning significantly more than the national average.

And there may be enough of this group of potential buyers to continue to support higher prices.

“There is a certain small cohort with significant characteristics who are fitting in with the macro indicators that housing is affordable,” he adds, noting that the pandemic suited some workers, whose jobs weren’t impacted and who benefited from the ability to save more.

As a result, while he expects “softer growth” going forward, he says the current upward swing in prices “probably has a bit more to run”.

Possible correction?

With such sharp price rises across the EU – not to mind the fact that the commission deems so many of them to be overvalued – forecasting a sharp correction would be understandable.

However, the commission does not see “substantial risks to macro-financial stability”.

“Though a house price correction triggered by a rise in interest rates cannot be ruled out, the price adjustments are likely to be muted in view of the strong fundamentals behind demand and existing supply side restrictions to the housing stock,” it says.

“Significant price corrections are unlikely due to strong demand and constrained supply”. And even if prices did fall, the impact would be nothing like that in the crash of 2008-2009, due to “the moderate credit cycle and subdued construction activity during this cycle”.

Hughes echoes this view in an Irish context, noting that a big difference in the Irish market today, compared with during the boom, is that there isn’t any speculative supply of property, and people aren’t overstretched, due to the lending rules.