Irish people do not spend more on average than those in comparable EU countries on housing. That was the perhaps surprising result of a new ESRI report. But averages hide a lot.

The report shines a light on the key divide in the Irish home-ownership market – between an older generation with its mortgage paid and younger people struggling to get into the market, either to rent or buy.

And it looks at the pressures facing those in the private rental market – the squeezed middle who do not qualify for State supports but are getting caught by soaring rental prices.

The report – Housing Affordability: Ireland in a Cross-Country Context by Wendy Disch and Rachel Slaymaker – is useful, above all, for putting the good, the bad and some ugly points of the Irish market in an international context. It is largely based on 2019 data – we know both Irish rents and house prices have increased in the interim.

If you feel you can’t afford an EV, you could be right

If our finances go flat, how will Ireland pay its bills?

The key decisions now facing Donald Trump which will have a big impact on the Irish economy

Election campaign got off to spluttering start on economic and budget issues. Here is what it all means

1. The good

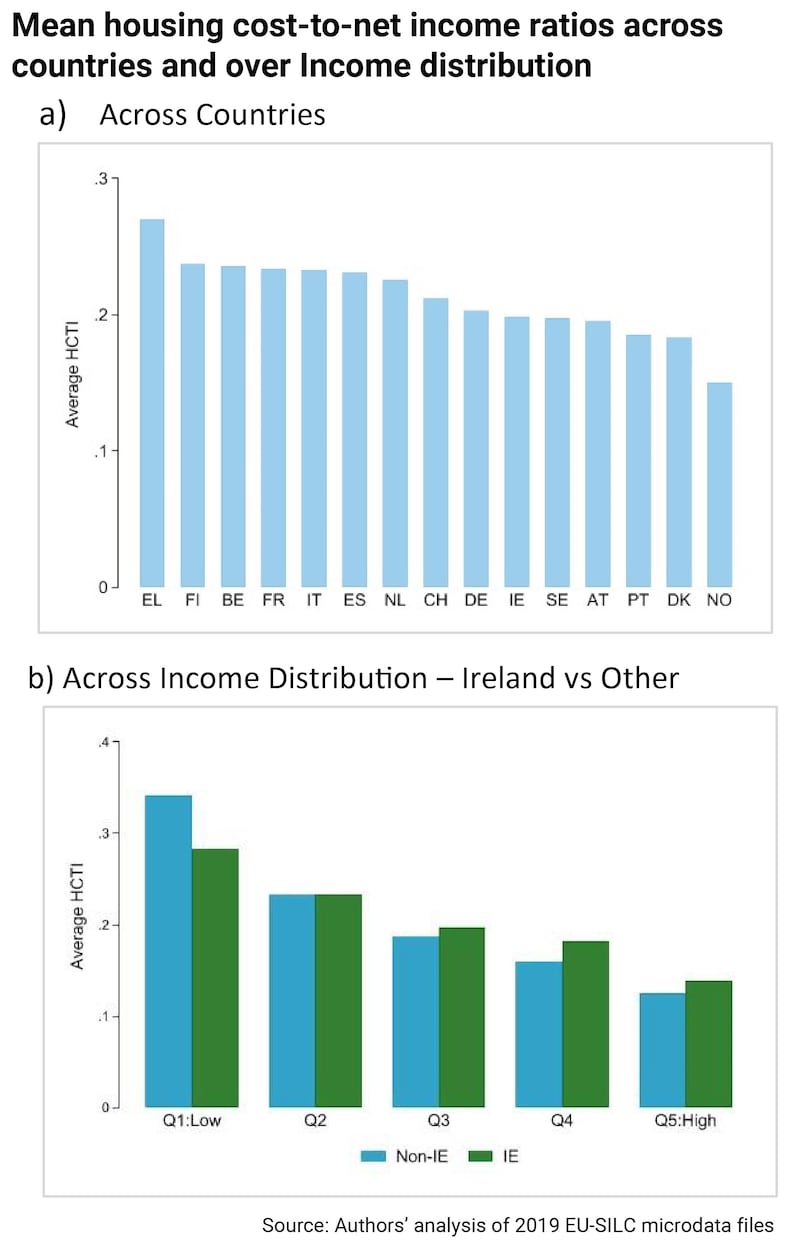

Overall the amount of money Irish people spend on housing is not out of line with that spent in 14 other European countries. On average Irish households pay one-fifth of their net income on housing payments – rent or mortgage, slightly below the average of the countries studied which is 22 per cent.

Nine of the countries have higher repayments on average while five have lower costs. As we will see below, the average hides many stories within the Irish housing market and we know that all is not well. But it does highlight a couple of interesting positives.

[ Barely one-third of adults under 40 in Ireland own a home, report findsOpens in new window ]

One is the high home ownership rates among the less well-off section of the population, with more than half of those in the bottom 20 per cent of the population by income owning properties.

On the face of it, this may seem odd, as many lower income people are priced out of the market. But the average is brought up by very high home-ownership rates among the older parts of the population, particularly the over-65s who make up half of this lowest income group. Some 86 per cent of this older group own their homes outright, have paid off their mortgage and thus have no housing costs.

The second piece of good news in the figures is the generally lower rental burden on the less well-off sections of the population.

This means a significant portion of the less well-off and older population does not face any risks from higher interest rates. Comparisons vary across different countries in this area, depending on social as well as economic factors, but in general Irish people are more likely to own and less likely to rent than elsewhere in Europe, with rental notably popular in northern European countries.

The second piece of good news in the figures is the generally lower rental burden on the less well-off sections of the population.

The availability of rental properties for this group – indeed for all renters – remains a big problem, as we know. But the extension of State supports such as Housing Assistance Payments means that many of those who are renting pay a lower proportion of their net income in housing costs than do those elsewhere in Europe.

More than half of all renters receive support and the extension of these supports after 2015 has led to an improvement in the position of lower income households.

These households pay an average of 26 per cent of their income of housing versus a European average of 36 per cent. It appears that the income-based level of rents charged in Ireland differs from the system in many other countries, where social housing rents are typically set to cover the maintenance and management of properties and to service borrowing costs relating to their provision.

The report makes the point that this does not mean all is well with low-income households, but that in most cases “ the poverty and deprivation challenges faced by these households in Ireland are primarily issues of low income rather than high housing costs.” And there is still a small group of lower-income renters who pay significantly more in relation to their income, including many single parents.

The latte levy: ‘Consumers want to do the right thing’

2. The bad . . . and the ugly

The flip sides of high home ownership amongst older people and lower rents among the less-well-off are clearly illustrated by the ESRI analysis. They are lower ownership among younger people – the familiar story of under-40s trying to get into the market – and relatively high rents among those who rely on the private rental market and do not qualify for State rental support. These are the pressure points of the Irish housing market.

In terms of home ownership, the research finds that in Ireland over two-thirds of all mortgage holders are in the 40 per cent of the population with the highest income, which is above the average of the countries studied.

The researchers attribute this in part to the Central Bank’s mortgage rules which – by limiting the size of loan in relation to income – mean that lower-income people find it difficult to buy at all. Central Bank rules are relatively tighter here than the average elsewhere.

Irish mortgage holders rank third highest for the share of income spent on mortgage repayments among the 15 countries analysed. Relatively high Irish house prices are one factor here – and so is the fact that the Central Bank rules mean better-off people are more likely to buy homes in Ireland, and this group tends to buy more expensive properties.

Despite this, however, relatively few pay more than 30 per cent of their disposable income on mortgage repayments – this is seen as a key level for sustainability.

This number will now be rising significantly as interest rates rise sharply. And the fact that over 12 per cent of households were paying more than 30 per cent of income in 2019 – when mortgage rates were low – to repay their mortgage and over 6 per cent were paying more than 40 per cent shows there are pressure points.

The researchers say that given the tighter lending rules since 2015, many of these households may have bought in the run-up to the 2008 crash. Many will be tracker mortgage holders now facing significantly higher repayment rates.

Housing markets are never straightforward, but the report gives a clear view of the problem areas here and of the key generational gap.

Stress levels are greater in the rental sector, with some 10 per cent of renting households, paying more than 40 per cent of their income in rent. In general middle to high-income renters, who do not qualify for State support, are more likely to face high housing costs than their European peers.

This is the squeezed middle of the renting sector, where significant affordability pressures have built up. By 2021, according to separate data, one in three private sector renters faced high housing costs, based on the 30 per cent benchmark.

And the final piece of the picture – not reflected by affordability data – is people who cannot afford to buy at all. Several findings, the report says, show Ireland faces particular problems here. Between 2015 and 2019, Ireland saw the largest share of young adults aged 25 to 34 remaining in their family home.

Ireland has a particularly low level of single income households, as in many cases two incomes are needed to meet housing costs. Ireland has the fourth highest rate of home ownership among over40s, but ranks ten of fifteen for under-40s, one of the biggest gaps between generations among the countries studied.

Barely one in three people under 40 are homeowners and many young people remain living at home.

Housing markets are never straightforward, but the report gives a clear view of the problem areas here and of the key generational gap.