After a particularly hard night, do you wake up and vow: never again? Guilt, maybe embarrassment, dread and self-loathing kick in. You resolve solemnly that you are not going to make that mistake again.

Repentance is part of human nature. Regret, followed by an undertaking to mend your ways, change your outlook and re-create a “new you” are normal.

But this resolve to learn from mistakes is not just a human attribute. It is also shared by institutions that have erred lamentably. The Central Bank is one such penitent.

Having failed to see one of the biggest bubbles in economic history right in front of them, the economists in the Central Bank are “born again”. Having sinned, they have become evangelical in their vigilance, seeing signs of overheating, delinquency and excess all around us.

This week came another warning of overheating. Unfortunately, without the instrument of domestic interest rates, it is quite difficult to see what the Central Bank can do about it.

Herein lies the inconsistency at the heart of Irish economic policymaking within the euro zone. Our monetary policy is dictated in Germany and, therefore, the chances of interest rates being inappropriate here are always high, because the Irish economy follows the US economic cycle more closely than the European one.

Over the course of the economic cycle, Irish interest rates are low when they should be high and might well end up being high when they should be low.

EU-wide conditions

At the moment, if the Central Bank is right and the economy is overheating, Ireland needs much higher interest rates to bear down on this effervescence. However, Irish interest rates are dictated by European-wide conditions.

In recent weeks, growth indicators on the continent have weakened considerably, suggesting low rates, still priced for a fragile continent, will remain inappropriate for booming Ireland.

Leaving Cert economics students know that low interest rates in an overheating economy are a recipe for instability.

Before we deal with this policy conundrum and investigate whether the economy is indeed overheating, let’s just define the concept. Overheating refers to a stage in the economic cycle when demand is so strong that all the idle capacity in the economy is used up and therefore inflation is likely, with prices rising everywhere.

For example, when unemployment is high, as it was a few years ago, employers didn’t need to offer high wages to coax people into a job. People needed jobs so they took them when they were offered.

Now, with unemployment reasonably low, if a company wants to expand, that employer has to offer higher wages to poach workers already in work to come work for him or her. The company can’t expand without extra workers.

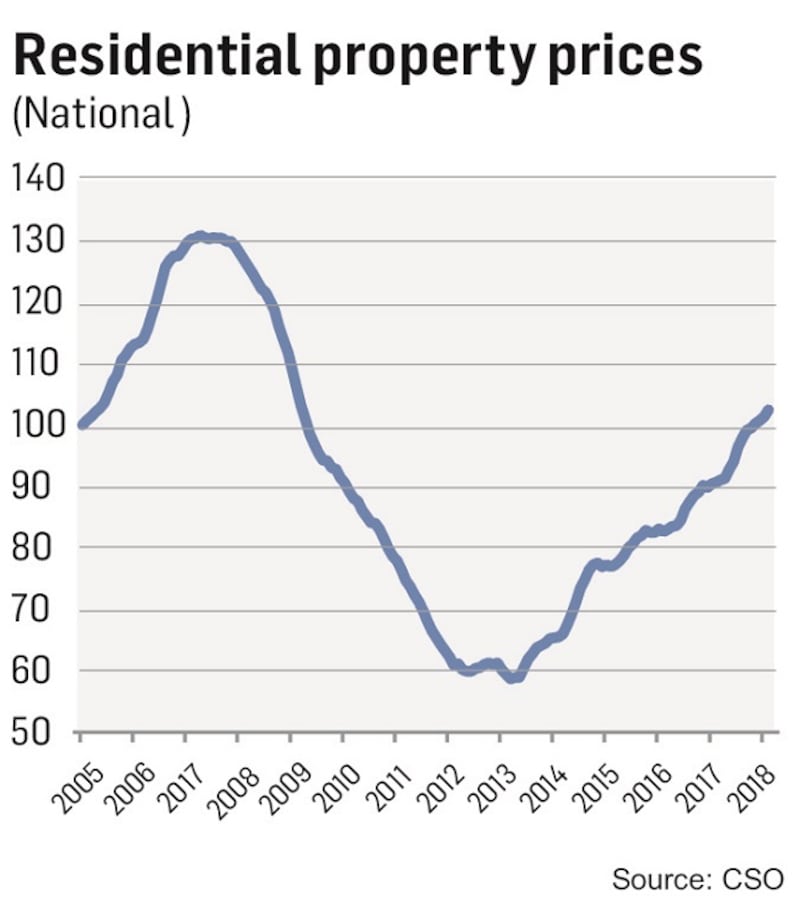

We see the same thing in the housing market. Without thousands of extra homes, the market overheats and prices rise.

But overheating isn’t just about wages and house prices. It can be captured in indicators such as traffic congestion and airport capacity.

When trying to assess overheating in the Irish jobs market, the question is: what rate of unemployment triggers wages rising?

The OECD argues that when the Irish unemployment rate falls below 8.5 per cent, Irish wages start to rise. This seems very high because it means that 8.5 per cent of the labour force either doesn’t want a job or isn’t up to working.

Favourite indicator

If we drill a bit deeper into this conundrum we see that Irish women, in general, are not working in anywhere near the same numbers as their EU sisters. For example, today only 55.9 per cent of Irish women of working age are working outside the home. At the end of 2007, this figure peaked at 57.2 per cent.

This is way below the 70 per cent plus participation rates seen in countries such as the UK, Germany and Canada.

Therefore, when seen from an overheating perspective, Ireland runs out of female workers quicker than almost any other EU country. The implication here is that getting women back to work is hugely important.

Once Ireland gave away its interest rate and exchange rates to the euro, it rendered the Central Bank nothing more than a policy eunuch

Another favourite indicator of mine is the number of part-time workers who would be prepared to work more but can’t get more work. This number measures the slack in the market.

Nearly 40 per cent of those in part-time work would like to work more. And yet, more than 16 per cent of the total workforce is still working only part-time. These facts about part-time and underemployed workers who want to work more, together with the number of women not working, suggest that the existing labour force could meet the demand without more immediate immigration.

However, a higher level of immigration is probably the most likely short-term solution.

Traffic

Of course, more immigration means more people, more demand on the housing market, which is already choked, and more traffic on the roads – a sure-fire sign of an economy bursting at the seams.

There's a great website that keeps me up to date on Irish traffic, tomtom.com.

Today in Ireland, congestion levels that capture the increase in overall travel time relative to a free-flow situation stand at 43 per cent . This means it takes 43 per cent longer on average to travel by car on Irish roads now relative to what it would take if the roads were not full with traffic.

These figures rise to 80 per cent and 86 per cent when we look at morning and evening rush hours respectively.

Traffic at our airports increased 10.3 per cent between 2015 and 2016, and 38 per cent since since 2012.

It seems clear the economy is overheating on most metrics but the question is what is the Central Bank going to do about it. Here is the mendacity at the heart of these statements from the Central Bank.

Could this be an “arse-covering” exercise (a technical term) in the event of another crash? Of course it is.

Once Ireland gave away its interest rate and exchange rates to the euro, it rendered the Central Bank nothing more than a policy eunuch when it comes to controlling inflation.

So it can bleat all it wants, but there is nothing it can do, and it knows it.