The economist and author David McWilliams writes his first weekly column for The Irish Times

Unlike hosting the Rugby World Cup, the global economy is no longer an “all-or-nothing” game of nations pitted against each other where for one side to win the other must lose. It’s more nuanced.

Nor is the national economy like the national soccer team; in the global game for prosperity there are no qualifiers and no World Cup every four years. Rather there is constant competition, and two countries can win at the same time.

With the re-emergence of flag-waving and nativism in global politics, it’s easy to forget that countries and national economies can defy simple geopolitical definitions or groupings. Globalisation has allowed countries, particularly small countries, to escape the tyranny of geography.

For example, despite the political rhetoric of Ireland being at the “heart of Europe”, the truth is that Ireland isn’t really a European economy at all but an Atlantic economy, profoundly influenced by history, geography, language and culture.

Compared with any other EU country, Ireland is more exposed to Brexit, more open to American investment and more porous to Anglo/American commercial norms and innovations. In addition, our mercantile structure is held together by a shared English-language, common law system.

A trading state

Over the past two decades while we have become diplomatically and constitutionally closer to the EU, we have become economically and commercially closer to the American world. Close to 80 per cent of our total exports now come from US multinationals, and this figure is growing.

We’ve done well out of this economic promiscuity, servicing both sides with equal enthusiasm. American capital flowed in, as did European immigrants seeking better prospects.

Increasingly, Ireland looks less like a region of Europe and more like a trading hub off the continent’s west coast, akin to a medieval Hanseatic city state, an early 20th-century Shanghai or a 19th-century St Petersburg. The “trading state” has been a feature of economic history from ancient Alexandria to Dubrovnik.

Macron may have a bigger impact on Ireland than Brexit

Commercially Ireland is more akin to a trading state than a nation state. The growth of services rather than manufacturing, the fall in transport costs and the emergence of ecommerce have insured that Ireland is not on anyone’s periphery but at the centre of the globalised trading world.

However, playing this trading state game takes skill and vision.

We should aim to maintain a footloose commercial status in the face of the relentless march of harmonisation, the enemy of uniqueness.

Economic history tells us that others, usually bigger players, become jealous of the small trading state’s autonomy and move to strip it of its advantages, particularly if capital is moving consistently towards the smaller competitor. Remember, money is like water, it always moves to the place of least resistance.

To maintain this position as a home for international capital and a destination for international talent, our trading state must be deft and subtle, negotiating between the great powers rather than siding with one explicitly.

The Macron factor

Over the years, I’ve often visualised Ireland as a jockey riding two horses: the continental EU horse and the Atlantic Anglo/American horse. When both horses are riding together, the jockey’s position is tenable.

For years, both horses ran together as the EU and the Anglo/American world were on the same track economically, socially and politically. But three forces – Brexit, US president Donald Trump and French president Emmanuel Macron – have changed the nature of the race.

The Brexit arguments have been well rehearsed elsewhere. In terms of individual countries the UK is our single biggest trading partner. No other European country is as important to us.

Trump is a threat to our capital base because he wants to reduce US corporation taxes to coax American capital back home.

But while Trump wants to drop taxes, Macron wants to increase them. The greatest threat to Ireland’s trading state status is not the in-your-face, nativist, flag-wavers in Washington and London, but the behind-the-scenes, integrationist harmonisers in Brussels and, more importantly, in Paris.

Although we only do €9 billion of trade with France (which means we do more commerce in nine weeks with Britain than we do over a whole year with France), Macron may have a bigger impact on Ireland than Brexit.

Because of the dominance of the UK and the English language in Irish media, we receive a lot of UK-centric and therefore Brexit-obsessed news. However, in continental media, Brexit rarely holds the front page. For most Europeans, Brexit simply makes detached what was always semi-detached. In contrast, the EU’s own backyard has long been framed by the Franco-German relationship. And this too is changing.

Even as German chancellor Angela Merkel pieces together her new coalition government, there is a sense that this will be her last hurrah. Across the Rhine, Macron realises this and sees an opportunity to remould Europe. Macron is the man of the moment and he realises he needs to construct a new rallying call to combat populism.

In the first round of the French elections, populism revealed itself on the extreme right and extreme left. In Germany, it materialised in the form of the Alternative für Deutschland (AfD) on the right. Meanwhile, the nationalist revolt in Catalonia has further undermined European harmony, which was once taken for granted, particularly in Brussels.

Further east, reactionaries and nationalists with values that run contrary to core EU positions on migration and racial tolerance are in power across a vast territorial arc from Stettin in Poland to Bratislava in Slovakia and on to Budapest. In the old imperial capital of Vienna, an anti-immigrant electoral surge has propelled the extreme right to power.

Macron sees these difficulties within the EU as the signal for regeneration of the European project, a siren call made more acute by the anti-EU developments of Brexit and Trump’s presidency. Be under no illusion: British and American nativism supports European populism implicitly and, in less guarded moments, explicitly.

The French president envisages a more integrated EU economy, more adept at combating the US and Asia.

Macron’s European regeneration means “more Europe”, that is tax harmonisation and particularly corporate tax harmonisation. It will not just be about the rate at which corporate tax is levied, but also be about the way tax is assessed. For services such as Google ads, this implies the tax will be levied in the country where the ad is placed, as opposed to where Google is domiciled, which is Ireland.

Commercially, the new Europe will be the gospel according to EU competition commissioner Margrethe Vestager, made flesh in the guise of Macron.

Ireland’s call

What do all these developments mean for Ireland – the 21st-century trading state?

We must make a choice. We can stay outside the new integrationist EU, using our veto to block any changes to our tax code, but this confrontation risks siding with tax avoiders or “corporate deserters” as former US president Barack Obama described them. In addition, “Official Ireland” is unlikely to step off the integrationist wagon even if an economically deeper Europe is not in our interest.

Is there any way Ireland can use the tumult in the years ahead to our advantage, remaining a premier destination for mobile capital, investment and talent? Can we remain a trading state, like the Hanseatic cities, ensuring our citizens are prosperous?

Yes we can.

What about proposing that multinationals take the difference between what they owe and ought to pay, roughly €9 billion, and pay this to us in shares?

It is possible but we must take the lead and redefine the relationship between the nation state and international companies. Unless you believe globalisation is about to come to a shuddering halt, investment will remain global, corporations’ supply chains will remain multinational and – as noted – money will move like water to the place of least resistance.

Here’s the way the system works now.

The multinational sets up in a country, creating jobs and paying as little tax as it can. The company gets access to the market and the country gets jobs and tax. In the case of Ireland, our attraction is enhanced by the fact that multinationals based here have the concession to trade with the EU. It’s a free pass.

We get only tax and jobs and if we don’t have the local talent to fill the jobs, educated Europeans come without needing visas or any suchlike that Brexit threatens.

Tax and wages are income, but the real question is what happens to the wealth of the multinationals? The distinction between income and wealth in economics is one of the least well understood by politicians, which is not surprising because income is short-term and so too is politics. Wealth is longer-term and inheritable.

The lion’s share of the riches made by multinationals goes to shareholders in the form of rising share prices and dividends. Only a tiny fraction goes back to workers in the form of income and to the host state in the form of taxes.

What we want

The tumult in the world gives Ireland a chance to change this system in a way that all Irish people might benefit and in a way multinationals could embrace.

We could reinvent the relationship between the state and the corporation. In so doing we could remain fully European but with an American sense of corporate innovation that would enrich all Irish citizens. Investment would flow in here, mirroring that of the successful city-states of the past.

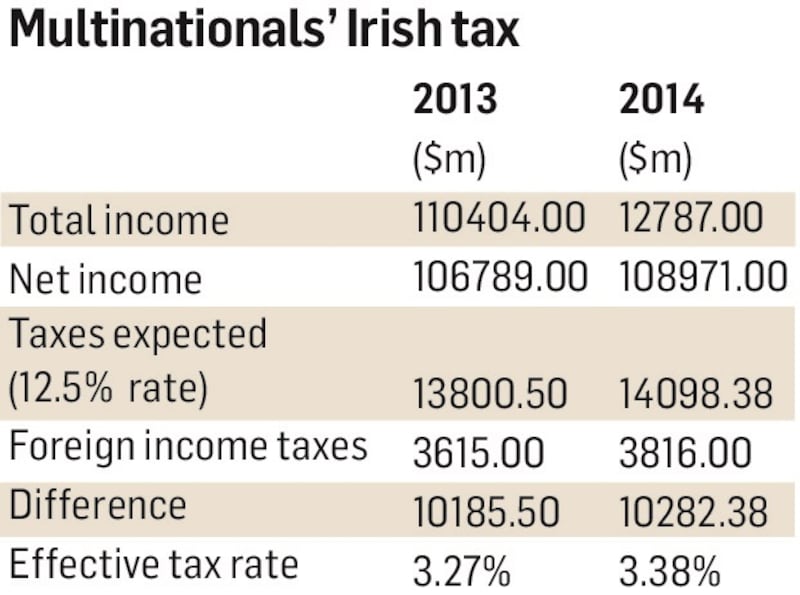

According to the US Bureau of Economic Analysis, American multinationals in 2014 made $113 billion (or €96 billion) profit in Ireland. Our corporation tax rate is 12.5 per cent, so they should be paying about €12 billion a year in tax. But they paid only €3.25 billion. This means that about almost €9 billion is missing because these companies use a myriad of loopholes to avoid even our low rates of tax.

The net is tightening, and companies such as Apple are moving money to offshore structures to avoid tax. But these companies know they are on the wrong side of global opinion, and they want a way out.

Deals are done when both sides have something to gain from reaching an agreement. Multinationals in Ireland want a new deal which minimises their immediate tax outgoings while being tax compliant.

What do we want?

We want them to stay here, but we want something more. We want a share in their wealth, not just wages and tax income.

What about proposing that multinationals take the difference between what they owe and ought to pay, roughly €9 billion, and pay this to us in shares? We then set up an Irish sovereign wealth fund with about that figure every year in the shares of multinationals based here. These are the shares of the best performing companies in the world across some of the fastest growing sectors of the global economy. This fund could grow rapidly, creating a real source of wealth for this country, which could be between €110 billion and €140 billion over a decade – €23,000 per Irish person.

In such a way, we could treat the multinational presence as akin to an oil find, as Norway has banked its oil windfall. In this way, we don’t just get income, we share in the wealth of the companies and we put aside this wealth for future generations – into a fund that can’t be used to finance day-to-day Government spending.

Nor would this fund necessarily be used to fund pensions; it could be used as a start-up fund. The Irish economy needs a vibrant start-up scene and not just a multinational sector. Pledging liquid shares of globally traded companies as collateral against investment funds for start-ups would lead to a surge in local innovation.

The attraction to multinationals is that it is exactly how they pay their workers now: in a combination of wages and share options. They would be paying the host country in a similar split between tax and share options. In addition, this initiative reduces their immediate tax bill, which drops immediately into their bottom line.

Politically, this is a form of wealth redistribution in a country with significant levels of wealth inequality. It would give all Irish citizens a stake they don’t have.

It gets us out of a potential scrap with Brussels, turning the threats of Trump and Brexit into a huge opportunity and putting us one step ahead of Europe, while keeping both feet firmly within the EU.

Geo-strategically, converting unpaid and future taxes into shares would place Ireland at the cutting edge of globalisation.

And Ireland would become a leader in framing a new relationship between the nation state and the global multinational.

David McWilliams’s column will appear every Saturday