It's not a bubble say governor of the Central Bank Philip Lane, the Minister for Housing Simon Coveney and ratings agency Moody's. It is, say putative home buyers and economists like Colm McCarthy. But who is right?

Prices are undoubtedly rising – and fast – but this does not a bubble make, in itself. A bubble happens when price appreciation is unsustainable because the fundamentals – ie earnings, demand, etc – do not support it.

So is this present in the Irish market at present?

We take a look at some of the typical characteristics of a bubble and consider to what extent these are now present in the Irish market.

Chart 1: There’s a sharp rise in house prices – yes

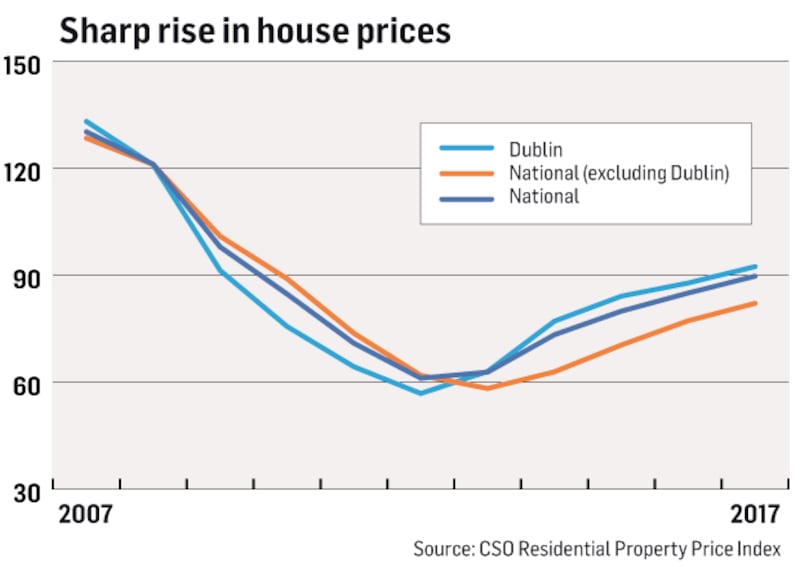

Since the nadir in around 2007, house prices have rebounded substantially. Figures for the first quarter of the year show that gains in the period were the fastest since 2007, rising by 0.9 per cent, the strongest first-quarter gain since 2007.

Moreover, expectations are that this trend will continue, with Davy Stockbrokers for example, predicting house price growth of some 10 per cent this year.

So far, so bubbly perhaps, but it should also be noted that, in many cases, price growth is coming off a low base. It is still possible to buy a three-bed semi-detached home for less than €100,000 in many parts of the State.

National house prices are still 31.5 per cent lower than their peak in 2007, while Dublin residential property prices are 31.5 per cent behind their February 2007 peak.

Now, while it’s unwise to suggest that prices should naturally return to those levels, the figures do suggest that there is plenty of scope for prices to continue to rise without touching those heady (unsustainable?) values back in the boom years.

Last month, the European Commission suggested that while demand is outstripping supply in Ireland, there was “no evidence of overvaluation in the property market”.

Bad loans are common – kind of

Thanks to the new Central Bank rules, it’s not a case of problematic new lending; rather it’s more about historical issues that continue to overhang the Irish economy, posing “financial stability and consumer protection risks” as governor of the Central Bank Philip Lane put it recently.

The impact of reckless lending during the boom continues to overhang the economy. While the volume and scale of mortgage arrears continues to improve, it still remains significant, accounting for a staggering 13.4 per cent of total mortgage balances according to latest figures.

Chart 2: There’s lots of leverage – no

Leverage causes problems. Borrowing 100 per cent of the value of a property – or in some cases even more – puts both lenders and borrowers alike at risk from a decline in property values, offering no cushion should the market move against them. Being able to borrow without a downpayment also increases the amount people can borrow and therefore the amount they can spend, which can push up the worth of properties artificially.

These days however, it’s still a case that the Irish economy is de-leveraging. Loan to values (LTVs) are very much restricted by the Central Bank’s mortgage lending rules.

When first introduced, the rules allowed first-time buyers to borrow 90 per cent of the value of a property up to a value of €220,000, and 80 per cent on the balance. Everyone else had to borrow 80 per cent or less.

Figures for 2016 show that the median LTV on a a first-time buyer loan was 85 per cent, or 70 per cent for someone trading up. This is the case even though exceptions are allowable, which means that a certain proportion are borrowing more than 90 per cent.

Since then, the rules have been loosened, and now allow all first-time buyers to borrow up to 90 per cent, which means that there will likely be some increase in LTVs.

Interestingly however, as Chart 2 shows, the typical boom-time median LTV was not far off today’s LTV – 85.7 v 85.89 per cent – while the mean or average, was actually lower in 2006 (77 per cent) than it was in 2016 (78.8 per cent).

Another point is the prevalence of cash buyers, which further dampens the scale of leverage in the housing market. According to figures for 2016, about 47 per cent of all sales last year were by cash buyers.

The only caveat to note is, again, the debt hangover from the boom. Irish household debt continues to remain stubbornly high although it is on a firm downward trajectory. Irish households remain the fourth indebted across the European Union, behind Denmark, the Netherlands and Sweden.

As of end-2016, Irish households had a debt to income ratio – ie the amount of debt a household owes compared to the amount of disposable income it generates – was 140 per cent, down from a high of some 210 per cent in 2009.

In contrast in Australia, where there are very real fears that there is a property bubble – and that it might burst – the ratio is of the order of188 per cent. On the other hand, countries like France, Germany, Italy – and even Greece – have ratios of below 100 per cent.

Access to finance is cheap and easy – not really

It’s no longer easy to get a mortgage. In addition to having to meet the Central Bank’s requirements, homebuyers also have to get approved by a lender. And banks only want the most financially sound candidates.

It’s also not “cheap”, or at least not cheap relative to current norms. While rates are finally showing a welcome downward trajectory, Irish mortgages continue to cost significantly more than their European counterparts, where 20-year mortgages can be had for less than 2 per cent. And interest rates are expected to rise in the short to medium-term.

Where this may be a factor however, is the Government’s Help to Buy scheme. Introduced in January of this year, it’s understood that there have been more than 5,000 applicants to the scheme since, which allows first-time buyers bolster their purchasing capability by claiming back tax they have paid over the previous four years.

Under the scheme, putative home purchasers can get a cash-back of up to 5 per cent of the purchase price of a property, up to a limit of €20,000.

This is undoubtedly fuelling growth in demand for new build properties, and it fulfils both criteria in that half of your downpayment is, in fact, “free”, while it’s also easy to access

But where this differs from the credit binge during the boom is that, back then, credit was widely available for everyone. Help to Buy is only relevant to those who fulfil the criteria for the scheme, and who purchase a new home, which is more of a limiting factor than a credit free for all. And while the scheme may make it easier to secure a mortgage, they will still have to fulfil all the lender’s requirements in order to draw it down.

Chart 3: Affordability weakens – kind of

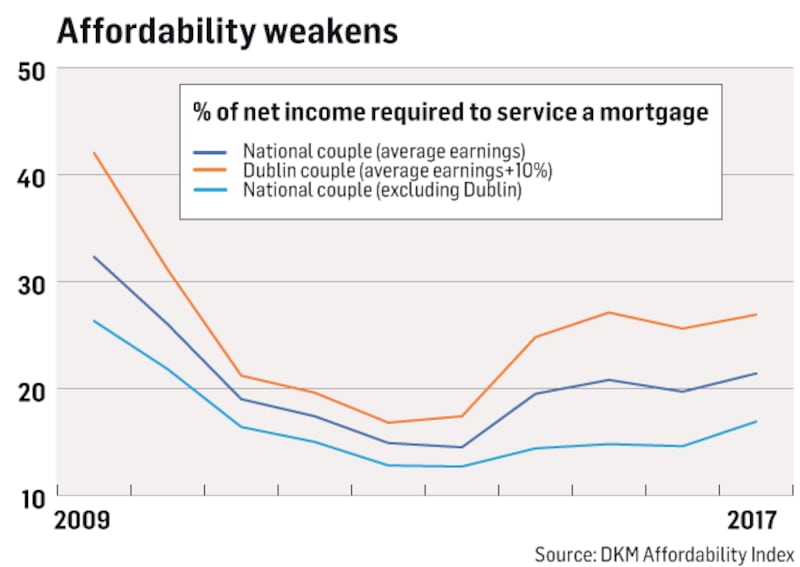

When house prices rise and are not supported by equivalent jumps in earnings and other fundamentals, affordability is stretched and problems can arise – particularly as we all know when affordability issues are masked by reckless lending.

However, while affordability across Ireland has weakened of late, it is still within the norms which suggest that about a third of a household’s gross income should go on rent or servicing a mortgage.

For example, back in 2007 the average working couple spent about 26.3 per cent of their net income servicing a mortgage outside the capital; this shrank to just 12.7 per cent by December 2012, and has rebounded to about 17 per cent.

According to DKM, the most affordable county in Ireland is Roscommon, with an average price of €73,000, which means it takes just 7.4 per cent of a couple’s after-tax income to fund a mortgage.

In Dublin, affordability is tighter – down from a high of 42 per cent in 2007, but rising again at 26.9 per cent, which puts it close the preferred debt service ratio. The least affordable area for first-time buyers is Dún Laoghaire Rathdown, where it takes almost 34 per cent of after-tax income to pay the mortgage.

Chart 4: House prices are rising faster than salaries – yes

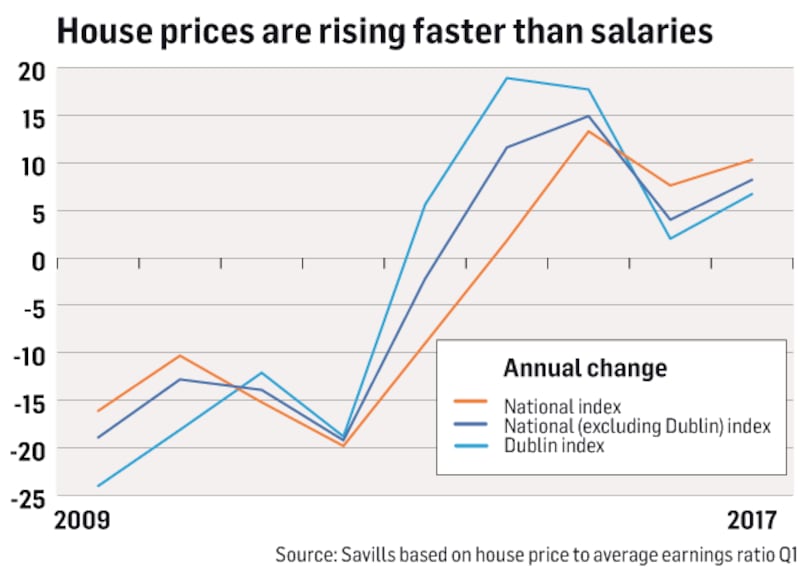

This is one potential area of concern. House prices are rising quickly but yet real incomes are stagnant at best.

As the Economist recently noted, if, over the long run, prices rise faster than the revenue a property might generate or the household earnings that service a mortgage, they may be unsustainable. Given the direction of rents of late, the former is less of an issue, but the latter is something to think about.

As data based on house price to average earnings compiled by property group Savills shows, the index was negative between 2009 and 2013 as house prices continued to fall. Since then, however, house prices have rebounded as earnings inch upwards. In the first quarter of the year, the house price to earnings ratio advanced by almost 7 per cent in Dublin, and by as much as 10 per cent nationally, when Dublin isn’t included.