With a round number to work off and a bit of wind in the sails after finding a willing contractor and conservation engineer, it was a case of so far, so okay, regarding our renovation plans.

The mortgage broker I’d dealt with when sniffing around Dublin properties explained that my bank had a competitive fixed rate offering and should be the first port of call when seeking money to pay for it all. Almost 20 years of relatively diligent saving would count for something, right?

After booking an appointment, and being advised of the relevant Covid protocols to be adhered to, I dumped the car in a church parking lot, masked up and got absolutely soaked in a spring downpour during the short walk across.

The loan manager gave as warm a welcome as 2m distancing permitted. We discussed how the sum being sought fell within the Central Bank limits for first-timers (now four times income) and was a good chunk less than what I’d secured approval for previously.

She was happy to hear I had no loans or debts, and we calculated that the payment on the mooted “mortgage product” would be about a third less than what I was shelling out in rent for my half of a Dublin apartment.

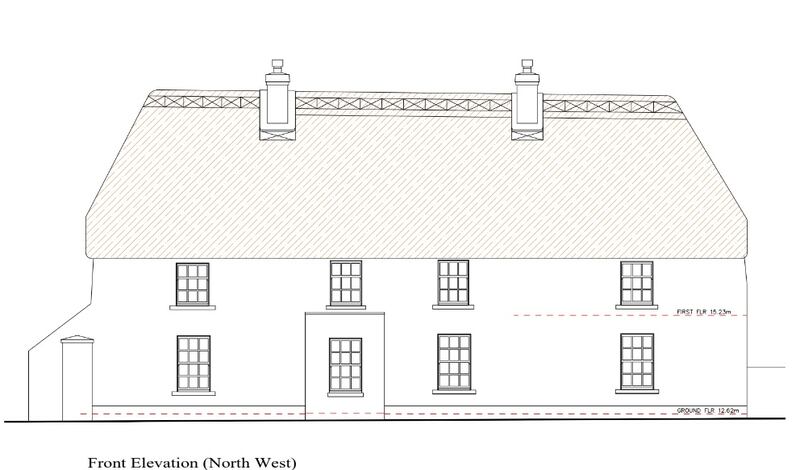

But it quickly became clear that getting approval to buy a raggedy 80sq m house in the north inner city was far easier a process than securing the green light, for less money, to take on renovating this big auld yoke in the middle of nowhere.

“A thatch? Is it insured?” she asked, thinking about the semi-regular media stories about the issue.

Luckily it was, unlike so many such houses dotted around the country, and I explained that the provider was content to keep it that way given it was a long-standing arrangement. While the premium wouldn’t be cheap, it was a bullet dodged.

I gave a rough rundown of the scope of the works required and agreed to return with a costed breakdown signed-off by the contractor and engineer, a Land Registry map showing the boundaries, and a valuation from an estate agent indicating what the house was worth then, and a projected “after repair value”.

Beyond that, we’d have to wait and see what head office made of the proposal, once all the relevant material was submitted. It wasn’t a flat no or a straight yes, but the homework prescribed would go some way to telling us if the loose sum targeted would cover it all. We hit the phones once more.

Shortly afterwards, confirmation came from Wexford County Council that the conservation works the engineer had proposed would provisionally qualify for a grant of up to €15,000 (the maximum) under the Department of Housing, Planning and Local Government’s Built Heritage Investment Scheme.

This meant that if we were to, for example, spend €10,000 on restoring the original sash windows, we’d be able to claw back up to 50 per cent once the job was done within a permitted timeframe and in a way that the council’s heritage department deemed appropriate.

Due to its protected status, the house does not require a building energy rating (BER). No harm, really, as the idea of putting double (or triple) glazing in while restoring the old windows was quickly shot down, regardless of how discreet it might have been. The shutters and curtains would have to continue doing the heavy lifting during the winter.

Elsewhere in the house, we chipped away some of the plaster that needed to be replaced — revealing stone up to a certain height and mud mixed with horsehair beyond that. We pulled down an awkwardly low wood panel ceiling in one of the upstairs rooms, which gave a clear view up under the thatch and of the extensive ecosystem of spider webs that had formed in the attic space.

A floating floor, installed to cover over a small and perilously steep set of steps running from the turn of the main stairs, into what we hoped would in time become an upstairs bathroom, was pulled up.

Quotes for the windows, drainage works aimed at halting damp issues, lime plastering and thatching rolled in, and the contractor provided costings for electrics, plumbing, a kitchen, bathrooms, floors and all the rest.

Having never spent more than €5,000 on any single thing in my life (a now 17-year-old car), seeing the numbers clocking up was mindboggling. But I had to remember that the money would, provided things went to plan, ultimately come from the bank rather than the current account.

A chartered surveyor visited, and his drawings gave a clear idea of the dimensions of the house and a means to see it as a blank canvas. His enthusiasm regarding the project was quite heartening. Less so was the estate agent putting a value on the place that was less than what we ideally would have borrowed. Once deemed to be “in repair” it was forecast to be worth the best part of two-thirds more, but that wasn’t much help at this stage.

After gathering all the requested material, I met the loan manager again and answered a few more queries. The bank’s desired loan-to-value ratio was calculated — at less than the full value of the house, of course — so the gap between what could be borrowed and what would be needed was widening.

Nevertheless, we had mortgage approval, a grant offer, the deposit I had saved for the Dublin house that I never bought, and some savings that hopefully wouldn’t need to be called upon. The cost of living (and building materials) was rising sharply and war had broken out in Ukraine — but surely that wasn’t going to drag on for too long?