Another landmark year, 2021 had a conundrum at its heart. Despite the pandemic dragging on longer than had been hoped, the economy has performed better.

Fears of an economic collapse in the early days of the pandemic had already proved unfounded – but the toll on the affected sectors has been immense.

As we entered this year, they again faced sweepings restrictions. Then, having declared the end of most restrictions at the end of October, the Government had to put policy into reverse, faced with a surge of infections and the Omicron variant. This means the scale of uncertainties facing the economy moving into next year are enormous – even when the worst of Omicron passes, what happens then. But to assess how 2022 might pan out, we first need to understand what happened in 2021.

The big numbers

The scores are not yet in for 2021, but we can make reasonable estimates. The underlying story confirms what first became evident in 2020 after the pandemic broke.

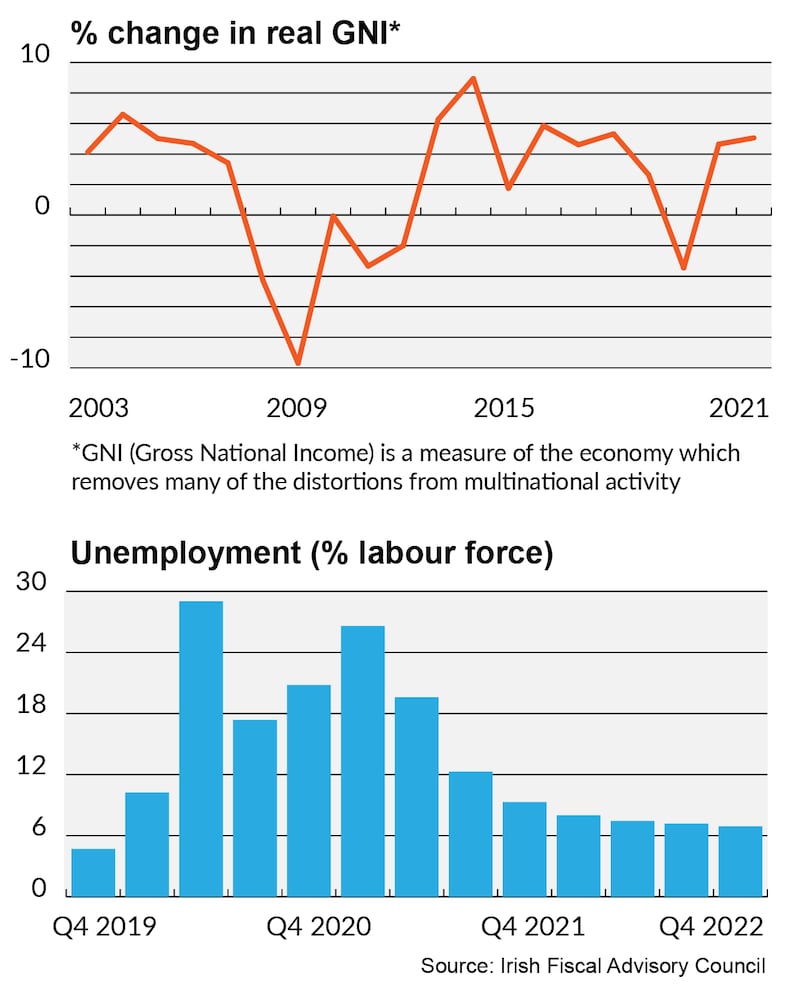

Large parts of the economy continued to operate successfully through Covid – the widespread collapse in activity and confidence anticipated when the first lockdowns happened in early 2020 did not occur. And so severe restrictions returned in early 2021, consumer spending and the domestic sectors were hit again, but the rest of the economy kept on going. This meant that forecasts for the economy at the start of the year were significantly exceeded.

Ireland’s GDP data is messed up by the accounting policies of the big multinationals. The headline figures are best ignored, though the likely rise in annual GDP of 15 per cent plus in 2021 will raise eyebrows internationally. But the breakdown tells a story. The multinational-dominated sectors of the economy – which had grown strongly in 2020 – were a further 22 per cent ahead in the third quarter of this year. The domestic sector, which suffered big losses in 2020, was running 7 per cent up year on year. One sector is powering ahead, while the other was making up some of the losses of 2020 and early 2021 but now faces tightened restrictions and more uncertainty.

In overall terms consumer spending and domestic demand were back at, or close to, pre-pandemic levels before the latest restrictions hit. So was employment, with 2.3 million people at work, though not far off 300,000 jobs remain supported by wage subsidies. Hours worked in the economy exceed 2019 levels; even though capacity in the exposed sectors is down, this is more than made up for in increased hours worked elsewhere.

The public finances

Finance minister Paschal Donohoe and public spending Minister Michael McGrath took no risks with the budget forecasts for this year, salting significant sums away to meet contingencies. And these were needed, as pandemic restrictions dragged on, requiring extensions of support programmes.

Fortunately the cost of borrowing for the State remained low – supported by massive money printing by the ECB. But the deficit between taxes and spending will probably be around €8 billion to €10 billion, lower than the €20 billion anticipated at the start of the year and a big positive for the exchequer While some leeway was built into tax forecasts, the surge in revenues as the year went on was ahead of anyone’s expectations.

A few factors have been in play. First, as in 2020, better-paid jobs responsible for most of the income tax were largely unaffected – those who lost their jobs or went on the PUP were largely lower-paid people who paid little income tax because of the structure of the Irish tax system. So as much of industry and the digital service sectors thrived, income taxes rose.

Second, when the domestic economy got the chance to reopen, it did so successfully. With many households having built up savings, spending rose and receipts for VAT and other indirect taxes recovered. New restrictions and uncertainty over travel will now hit spending in some sectors again – and extended supports will push up costs to the exchequer.

Third, corporation tax has been the gift that keeps on giving, with a monthly record €4 billion pulled in during the big payment month of November alone. Corporation tax receipts will likely exceed €14.5 billion this year , more than one in five of every tax euro collected. This has helped meet a lot of the pandemic bills, but does create significant uncertainties for the years ahead, particularly after a a big international corporate tax deal was agreed.

The tax deal

There is no doubt that the OECD corporate tax deal was one of the big economic news items of 2021, with very significant – and unpredictable – implications for Ireland.

Ireland benefited enormously from the first phase of OECD reform, signed off in 2015. This has meant that major multinationals restructured their operations and cut off previous use of offshore tax havens like Bermuda and the Cayman Islands. Instead they moved a lot of what are called their intangible assets to Ireland.

These fall under the heading of intellectual property (IP) assets – the trademarks, patents and copyrights derived from the design, development and marketing of major physical or digital products.This IP has been central to multinational tax planning in recent years. The relocation of these assets to Ireland has spun off into more profits being declared and taxed in Ireland.

Together with strong profits in many multinational sectors, this has been a key factor in boosting corporate tax revenues. But other finance ministers have been looking jealously at the increasing tax take here. And the OECD process carries threats to Irish revenue and to Ireland’s tax strategy.

This is why the stakes were so high when Paschal Donohoe refused to sign an outline deal reached in June. This comprised two main parts – one is a change in where multinationals pay some tax,meaning they will in future pay a bit more in their major markets.

This means more tax for big countries like France and Germany and less for smaller countries where multinationals have been headquartered, like Ireland. Accepting this part of the deal had also looked like the price of peace for Ireland.

But Donohoe objected to the second part of the proposed deal – a commitment to a minimum global corporate tax rate of “at least 15 per cent”. After a few months of high-stakes economic diplomacy the “at least” was removed and Donohoe agreed to sign up.

In truth, it would have been impossible for Ireland to stay outside a deal in the long term. So if the OECD deal is finalised – and significant uncertainties remain as to what legislation will be passed in the US and by when – then Ireland’s 12.5 per cent rate for big multinationals will be no more, though the Government plans to keep the rate for domestic companies.

With or without an OECD deal, the EU is now likely to press ahead anyway with a minimum tax plan.

The importance of removing the “at least” was that Ireland will still be able to offer a corporate tax rate lower than many other countries. But the impact of the OECD process and changes in US tax laws on international investment flows and the accounting practices of big multinationals remains uncertain. And the difficulty Joe Biden has faced in getting key legislation including the minimum tax rules through the Senate do complicate this for Ireland, This is a slow-burner, but a really important one.

The housing debate

If corporate tax was the big international economic issue for Ireland, housing continued to dominate the non-Covid domestic agenda. House prices – and rental costs – continue to march higher. The Government has promised a big increase in building in its new housing plan – and new home starts are picking up sharply.

However building takes time, and demand is strong due in part to Covid-19 savings – a factor seen in many international housing markets and not just here.

National house prices increased 12.4 per cent in the year to September and have now more than doubled from their 2013 trough.

Meanwhile average rent nationally now exceeds €1,500 a month and has topped €2,000 a month in Dublin. The latest Daft report for the third quarter of the year showed that the number of rental properties available for rental was just 1,460 nationwide, with just 820 available in Dublin, an extraordinarily low number.

The Government’s new housing plan, announced in September, targets a big increase in housing supply – 300,000 new homes by 2030 – part-funded by a significant increase in State spending on housing , which is due to reach €4 billion per annum on average.

There is, meanwhile, some evidence of a pick-up in building activity with housing starts rising and forecasts that some 30,000 homes could be completed next year, up from around 22,000 this year.

Higher levels of apartment building could add to both housing and rental supply. While more apartment building will help the market, the cost of building – and thus rental – remains a major issue and so likely rental trends are unclear.

Despite rising rental returns, there has been a steady trickle of private landlords away from the market. Some complain of the compliance burden – others of rent caps and some are presumably choosing to sell into a buoyant market.

Meanwhile, the longer-term goal of policy – for more people to live closer to work in smaller units beside public transport has never really been debated. And it could yet be affected by Covid-19 and the trend of working from home, already a factor in the market

The Green agenda

While Covid-19 was the most immediate economic issue of 2021, the Cop26 summit in Glasgow and a new climate action plan from the Government put a new focus on the target of reducing carbon emissions. Slowly but surely the scale of the challenge is

moving into view – and figures showing that emissions dropped by just 3.6 per cent in 2020, with much of the economy shut for long periods, underlined the challenges ahead.

The Climate Action Plan is designed to put Ireland on track to cut emissions by 51 per cent by 2030. But the scale of the transition is enormous – by 2030 the target is to have 80 per cent of electricity generated by renewables, a bedrock of the whole plan given that it requires the use of “clean” electricity across the economy.

A massive retrofitting programme is planned for homes and commercial buildings and by 2030 the target is to have nearly one million private electric vehicles on the road – meaning new purchases of petrol and diesel vehicles would by then be more or less phased out.

Next year, the targets for various sectors – ranges are suggested in the Climate Action Plan – are to be honed down to legally binding target figures. This will further intensify the debates now getting underway about what this means for different sectors – including agriculture, households, businesses and Government.

The days of climate fudge are slowly drawing to a close as we face the decisions ahead which will – like most major changes – bring costs, disruption and opportunities. All of course, within the context of the obvious point – if the world does not get to grips with this, the social and economic costs and disruption will be many times greater again.

The bottom line

2021 ends with significant uncertainties. Of course every year does. But not on this level. The potential wide and rapid transmission of Omicron adds a significant short-term risk and raises longer-term questions.

And the battered domestic sector, so resilient so far, faces increasing risks the longer restrictions go on – and the more consumer habits change.

So while we enter 2022 with the significant protection of vaccines, we are still battling Covid-19 and wondering whether the situation can be brought under some kind of control in 2022. In turn the Covid-19 situation will drive a lot of other things – policy from the ECB, for example, which is vital for Ireland and the general international economic backdrop.

The plus side is that we now know much of the Irish economy can truck on regardless, in turn creating resources for the sectors which can’t. 2022 will start much like 2021,with continued talk of restrictions and worry about infection levels. But after that is anybody’s guess.