It is time for the Government to “take a strong hand” with the banks, according to the chairman of the Oireachtas finance committee John McGuinness, who wants more interest paid to people who have money on deposit.

His comments come in the wake of those of the Minister for Higher Education Simon Harris, who says the Irish banks are “complete and utter laggards” when it comes to passing on European Central Bank (ECB) interest rate increases to savers.

Ironically, the backdrop for the latest outbreak of annoyance with the banks is the healthy profits they are making, with these profits being driven in part by the interest rate the banks are getting from the surplus customer savings they are putting on deposit with the Central Bank.

But what do the statistics from the European Central Bank tell us about interest rates in this jurisdiction and whether they are out of line with other parts of the euro zone?

READ MORE

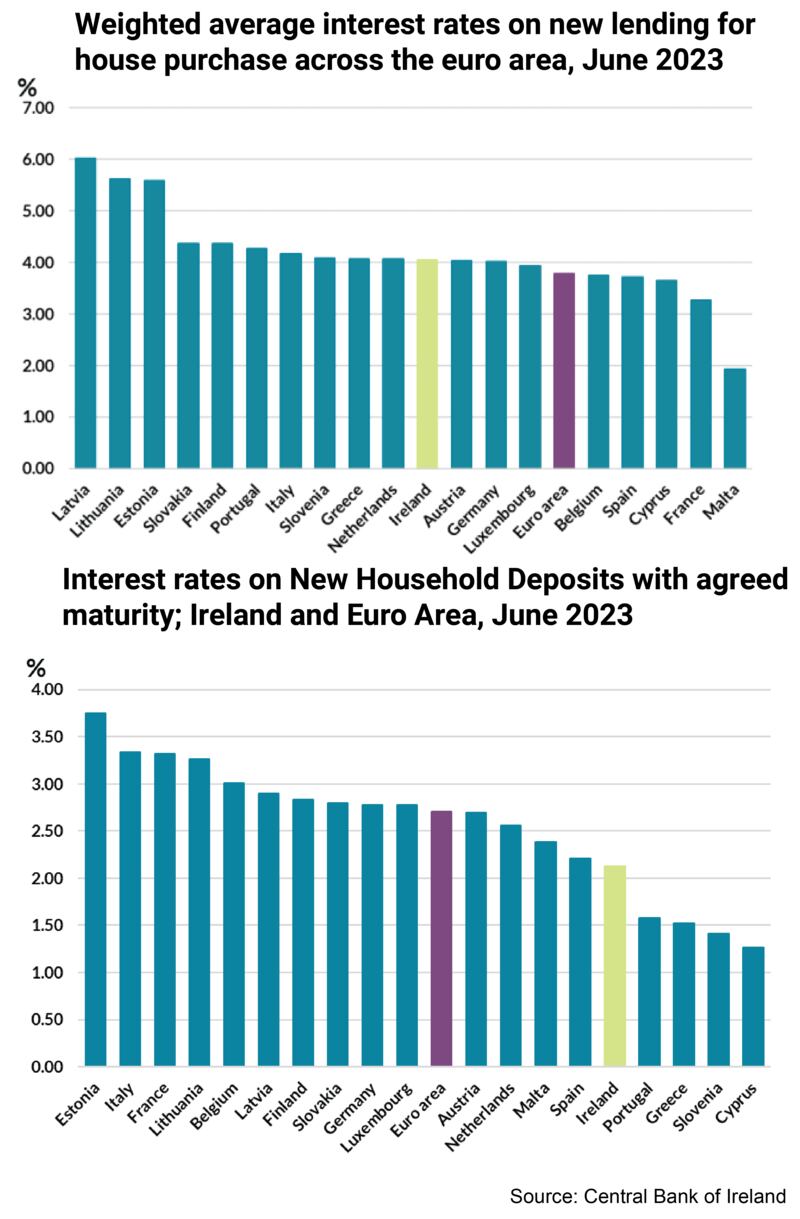

The huge amount of data available covers a range of situations but the general picture that emerges is that Irish rates, for people with mortgages and for people with money on deposit, tend in both instances towards the lower end of euro zone league tables.

For instance, data from the European Central Bank for the end of June shows Ireland’s mortgage holders paying 3.96 per cent a year for mortgages, as against 5.58 and 5.44 respectively in Baltic nations Lithuania and Estonia, who come at the top of the table, and 3.75 and 3.64 in Spain and Belgium respectively. France comes in at 3.04 while Germany is at 4 per cent and Spain 3.75 per cent.

Slightly different figures are given for new mortgages (the Central Bank of Ireland last week said the weighted average interest rate on new mortgages at end June was 4.04 per cent) but the differences are not great and the relative ranking of the various countries remains pretty constant.

Banks take in deposits on which they pay interest, and lend out money on which they charge interest, making a profit on the difference between the two. They also source money in other ways besides customer savings but in general terms if banks are not being too rapacious those countries offering lower returns on savings should also be the countries that offer mortgages at lower rates. Does the ECB data show such a scenario?

In general it does. Data, again for the end of June, shows overnight deposits getting an interest return in Ireland of 0.07 per cent, the same rate as that ascribed to Belgium and Lithuania. Austria has a rate of 0.55, Germany that of 0.34 per cent, and France of 0.04 per cent. Portugal’s rate was zero.

So Ireland’s savers get relatively low returns from the banks, and Irish mortgage holders are charged relatively low rates of interest. The Irish banks (AIB, Bank of Ireland and Permanent TSB) have lagged many of their European peers in raising mortgage rates in the period since the ECB started hiking rates in July of last year as they make greater use of their deposits to fund loans, as against other sources of funding that apply in other jurisdictions.

More recent increases in mortgage rates have been matched by increases in savings rates, with the EU data indicating that the increase in the latter has outpaced the increase in the former.

Lithuania, at 357 basis points (if an interest rate goes from 1 per cent to 2 per cent, it increases by 100 basis points) tops the euro zone league for increases in the mortgage rate in the period from May 2022 to June 2023.

Ireland was second from the bottom for the euro zone, at 114 basis points, behind Greece (119) but ahead of Malta (29). The figure for the 20-jurisdiction euro area was 192.

The rate of increase over the same period for deposits of more than one year shows Ireland fourth from the bottom of the euro zone table at 140 basis points. This is compared to an increase for the euro zone area of 204. Top of the league comes Estonia, at 316 basis points. Bottom comes the Netherlands at 115.

It is because of the link between mortgage and savings rates that Darragh Cassidy, head of communications with Bonkers.ie, is wary of calls for significant increases in deposit rates. The banks, he says, “are holding down the interest rate on savings and, on the flip side, not hiking their mortgage rates too much.”

There is an element, he says, of being careful about what you ask for because an increase in savings rates to 3 per cent or 4 per cent could see an increase in mortgage rates to 5 per cent or 6 per cent.

“The exact same people who are calling for much, much higher deposit rates are the exact same people who would be complaining when mortgage rates go up because that is exactly what will happen. It will be one at the expense of the other,” he said.

Diarmuid Sheridan, a financials analyst with stockbroker Davy, agrees that there is a link between the rate that banks in a particular market will charge for mortgages and give for savings, although he notes that markets vary significantly, with, for instance, savings products on offer in France that don’t apply here.

“The Irish banking system has an enormous amount of liquidity,” he says. “A lot of that was built up during Covid.” Until the banks know whether those deposits are likely to hang around the uncertainty will create a downward pressure on deposit rates.

He also points towards what may be a wariness on the part of savers to put their funds into longer-term fixed deposit arrangements given current uncertainly over interest rates and inflation.

In its response to recent political criticism of the Irish banks, the Banking and Payments Federation Ireland has said its members have been slow in passing on the full effects of interest rate increases to both mortgage holders and savers. “Average mortgage rate increases in Ireland have been the second lowest when compared across other euro zone countries in the past year,” it said.

The figures support the federation’s position but, as financial commentator Karl Deeter observes, people with significant sums on deposit can be severely affected when inflation is significantly greater than deposit interest rates. “We may have forgotten how inflation is a really destructive force.”