If wider Ireland is anything to go by, a decade after the crash, it is hard to feel confident that the lessons of what went wrong at the FAI will really be learned here at home. But they may well be taught the world over. Lecturers in law, business or sports governance might construct entire courses around the mismanagement of football's governing body during the past decade or more.

Students will, in turn, be amused, amazed and horrified by the tales of ineptitude, denial and excess. It is hard to imagine a single one of these classes will be delivered without mention of the name of former chief executive John Delaney.

The 52-year-old might be said to have divided opinion when he took effective control of the organisation a decade and a half ago but, barring a few diehards whose determination to stand by him you almost have to admire, he has managed to unite people now.

Confirmation, expected on Friday, of the final six-figure payment he extracted from his employer prior to departure is only likely to harden opinions about a man who once answered an Oireachtas committee member's question about cuts to employees' pay and pensions with the contemptible line that working at the FAI was a privilege and not about the money.

Catastrophic error

One obvious lesson that might be drawn from his time at the association is that when a catastrophic error is made by an organisation, then it is in everybody’s interests that the person responsible depart, whether voluntarily or not. There is a widely held view within business that chief executives generally take that sort of stuff less personally because they appreciate why they were getting the big bucks in the first place. But not Delaney, whose opening gambit in negotiations aimed at securing his departure this year was a bid to reach a settlement that ran into millions.

Even that might have been worth paying a decade or so ago.

With Delaney in the driving seat and the rest of the board comatose at the wheel, the association went for broke

It is actually more than that now since Delaney championed the Vantage Club premium ticket scheme that was supposed to pay the FAI's share of the cost of redeveloping Lansdowne Road. From the moment that scheme failed, everything became about pretending, firstly, that it had not failed at all and, secondly, that even if it had, it really didn't matter that much.

Clearly, the timing of the scheme was unfortunate, with recession kicking in more or less the same morning the sales team hit the phones. But the pricing – €12,000 to €32,000 – was outrageous at any point in any economic cycle.

Had the association managed to sell its 10,000 tickets at just half the lowest figure, it would have comfortably raised more than half the money it was obliged to chip in for the stadium development. The rest could have been paid off in very manageable instalments over the next 20 years.

Instead, with Delaney in the driving seat and the rest of the board apparently comatose at the wheel, the association went for broke, which is pretty much what they were in a very short space of time.

Within six months they were offering softer terms to a nation that had just woken up to the dangers of easy credit. The die was cast.

Plan B

Had the board acted then, a new chief executive might have come up with a Plan B, but, for Delaney, that would have required an admission that Plan A had failed – and he was determined not to concede that. Instead, he was allowed to embark on a decade-long exercise in face-saving which would cost the association, and all who depended on it, dearly.

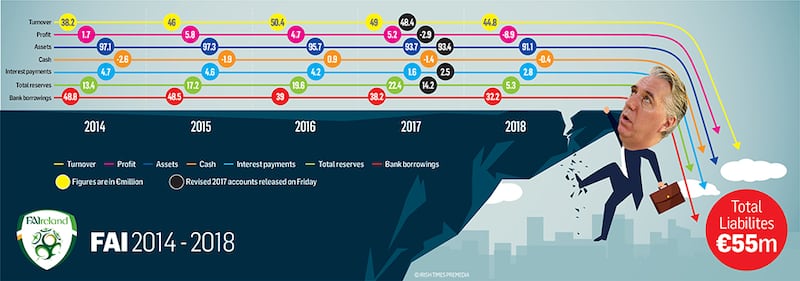

Danske, who had made the original loan for the stadium, left the market and offloaded the debt at a sizeable discount. Unable to cut a more desirable deal with a mainstream lender, the FAI suddenly owed €12 million less but at a hugely increased cost, and it paid €4.7 million in interest alone in 2014.

Delaney invariably put a brave face on it all. Each set of accounts would be presented as some sort of triumph

The figure did fall back to around €4 million per annum, about 10 per cent of turnover, then halved after a deal had been done with Bank of Ireland to move the debt again.

Long before that, though, cash flow became a nightmare, and everyone within the game suffered. Grants to affiliates would be delayed, senior clubs were made to wait endlessly for Uefa prize money, and association staff had those pay and pension cuts imposed.

Delaney invariably put a brave face on it all. Each set of accounts would be presented as some sort of triumph, and the rather ludicrous claim that the association could be genuinely debt-free by 2020 was perpetuated. In reality, the only way the debt could possibly be cleared was to draw down huge swathes of the income that should have been sustaining the association through the years beyond that, but the pattern was already clear. The 2017 accounts listed €3,065,286 in deferred income, a sponsorship deal “securitised” so as to get the money up front as well as the outstanding €390,000 of discount given to get the cash.

Dubious issues

There were, it transpired, other, more dubious issues with that year’s accounts, and a revised version is due to be presented on Friday, along with a restated set for 2016 (the accounts for 2014 had previously been restated).

The changes with regard to 2017 seem likely to include some reference to the now-infamous €100,000 Delaney paid over to his employers, then got back, while the figure entered for his remuneration is set to be revised upwards so as to take account of rent and expenses that previously went unmentioned. These latter items are key elements of a settlement with the Revenue which is expected to cost the association more than €1 million.

At the start of each and every set of those accounts Deloitte would say it was happy it had received the information required to produce accurate figures and that it believed it had done so. Apparently it was wrong.

Paul Cooke has already said that the 2018 accounts will include substantial losses, and the expectation is that there will be acknowledgement that real debt levels are higher than previously suggested. He said that people will be shocked, but there was genuine uncertainty as to whether they can be shocked after all that has happened at this stage.

It somehow seems unlikely, but we are about to find out for sure.