The announcement had long been expected, yet when it came in January the finality was still striking: Ulster Bank would close its last remaining branches in the Republic on April 21st.

“I know that our branches and colleagues have been a central part of these communities for many years and these final months of helping customers to move to new providers will be poignant for all involved,” Ulster Bank chief executive Jane Howard said at the time.

The NatWest-owned bank will move a step closer to leaving the State when it shutters those branches on Friday. There are 63 of them, stretching from Letterkenny in Co Donegal to Bandon in Co Cork.

While the bank will remain functioning for some time to come as it winds down its business, in practical terms the closures will signal the end of Ulster Bank for consumers.

READ MORE

It has been well signposted – NatWest confirmed the wind-down in 2021, weeks after The Irish Times broke the news of its plan – and in any case its remaining branches effectively stopped doing business at the end of March. For the past three weeks, staff have been there solely to help customers switch to another lender or deal with specific problems.

[ Ulster Bank set to exit Irish market after more than 160 yearsOpens in new window ]

Numerous lenders have pulled out of Ireland since the financial crisis 15 years ago but Ulster Bank’s closure is an order of magnitude greater than anything that has come before. It was established more than 160 years ago and was the State’s third-largest bank in recent years, firmly entrenched in consumer lending in a way that few of the former players had been. It had more than €15 billion of mortgages outstanding and €21 billion in customer deposits at the end of 2020, the last year before it announced its intention to leave.

By comparison, Permanent TSB had €13.8 billion of mortgages and just over €17 billion of deposits in the same period.

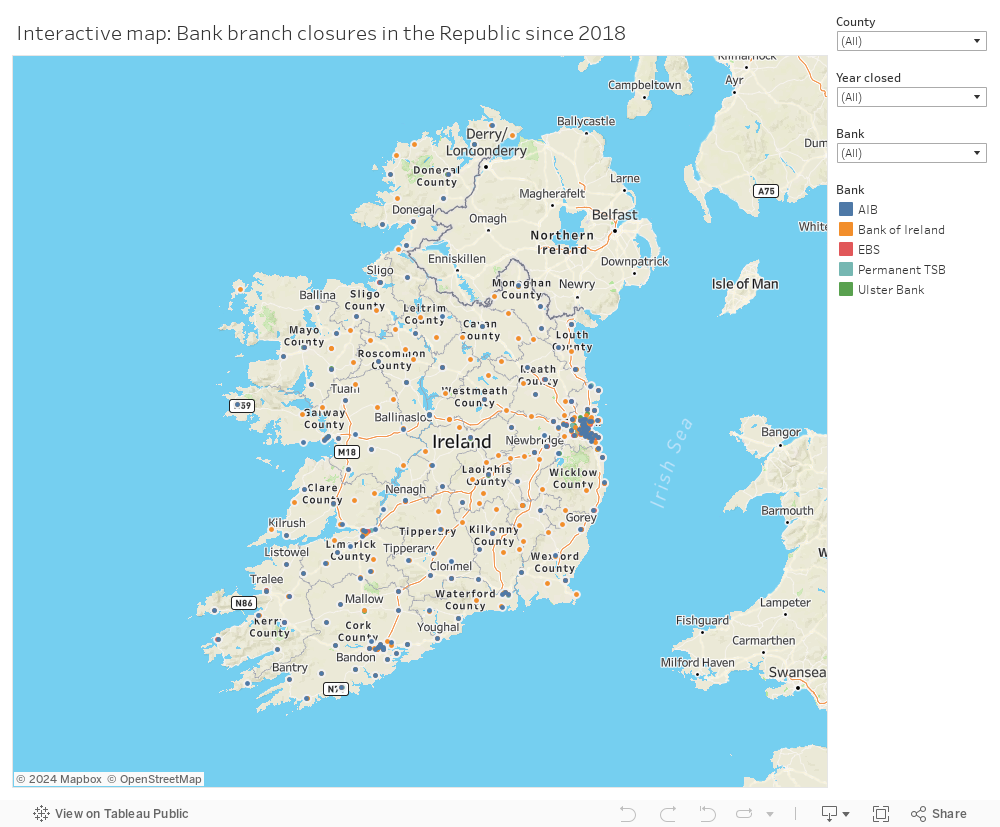

The interactive map below shows bank branch closures in the Republic since 2018, including those from Ulster Bank. You can zoom into the map to look at the closures in your area and also filter by county, year and lender. The branch location data was provided by the banks and then mapped precisely to create this visualisation. This data project was completed by Fiona Keeley, Glen Murphy and Paul Scott.

Combined with Belgian lender KBC’s decision to get out of Ireland, it is an enormous blow to the banking sector here, and to consumers.

The physical banking footprint here is now less than two-thirds of the size it was before the crash, and the loss of Ulster Bank underlines the demise of in-person banking throughout the State.

“Banks have tried to move their branches towards service or sales centres but it’s an open question to what extent that is really necessary, given the level of digitisation across retail and small businesses now,” says Diarmaid Sheridan, an analyst with Davy Stockbrokers.

Ulster Bank is the latest in a wave of branch closures in Ireland in recent years. AIB closed 15 branches in 2021, and sought to remove cash services from another 70 last year – a move it abandoned in the face of huge public and political outcry.

Bank of Ireland temporarily closed 101 branches during the pandemic. Ultimately, 88 of those – about a third of its network – closed permanently in October 2021.

KBC closed 10 of its remaining branches, known as hubs, last month. One in Dublin will remain open until August.

[ Ulster Bank closure: Where are we now?Opens in new window ]

Those recent cuts are only part of the picture. Go back a bit further and the picture becomes even more stark.

AIB’s network has shrunk to 170 from 276 locations in 2008. It’s EBS unit has been reduced to 66 locations from 98 over that same time frame. Bank of Ireland’s network stands at 169, down from 257 in 2021.

In 2010, when owner Royal Bank of Scotland – later rebranded NatWest – merged its First Active brand into Ulster Bank, there were 146 Ulster Bank branches. Next week there will be none. Add in the likes of Danske Bank Ireland, which shuttered its 27 branches more than a decade ago, and Irish Nationwide, and the scale of the collapse in branch banking becomes clear. And that’s without including the likes of Bank of Scotland (Ireland) or Dutch brand Rabobank.

Only Permanent TSB has expanded in recent years. This year it added 25 former Ulster Bank branches, taking its network to 101, as part of a wider deal to take on about €7.6 billion of its assets.

All told, more than 400 bank branches of varying stripes have shut their doors in the past 15 years.

The reasons are obvious: with the rise of online banking, fewer than a quarter of consumers consider a branch as their “main form of contact” with their bank, according to the Retail Banking Review published by the Department of Finance in November. That has had a knock-on effect on physical banking. When Bank of Ireland announced its branch closures in 2021, then chief executive Francesca McDonagh pointed out that footfall at the units being shuttered had plunged 60 per cent since 2017.

Still, when a branch closes, it has immediate ramifications for an area – especially if it is the last bank in town.

“Both communities and staff lose out when there’s a closure,” Financial Services Union general secretary John O’Connell said. Staff lose out because branch jobs “are still well paid, terms and conditions are quite good”. Communities lose out because lending can end up being pulled back, he added.

[ Ulster Bank to close all of its branches by mid-AprilOpens in new window ]

“There’s a study in the UK that shows there’s a 64 per cent drop in lending to SMEs [small and medium enterprises] when a bank branch closes, and that’s much higher when it’s the last bank in town. So that is a huge concern for us.”

Beyond SMEs, people who do not bank online tend to be the most affected by closures. In general, that means the elderly.

“The reality is the majority of people over the age of 70 are not online and are unlikely to ever be online,” says Celine Clark, head of advocacy and public affairs for Age Action. Forcing banking exclusively online “really opens up people to potential abuse, financial abuse, and coercive control, either within family or outside of the family. It erodes people’s independence and ultimately, their dignity.”

Then there is the impact on the geographic area around a permanently closed bank.

“In many cases, these are the highest-profile buildings on a main street in a town,” says one property agent who has handled bank branch sales in the past and asked not to be named to avoid jeopardising future business. “Many bank buildings are older and are often protected structures. That can limit what they can be used for.”

Another agent says: “In practical terms, the most obvious use for most of those buildings will be as hospitality venues, and not everywhere needs another pub or restaurant. Permanent TSB most likely has taken the pick of Ulster Bank’s branches – there is a question mark, in real estate terms, around the quality of what is left.”

Ulster Bank owns 31 of the 63 branches closing this week, and rents the rest. In the past when banks sold off shuttered buildings, they have tended to drip-feed them into the market. That’s been for two reasons: they don’t want to flood the market with similar properties and so potentially drive down prices, and they also wanted to avoid any blowback at being seen to callously put “For sale” signs on lots of branches at the same time.

Neither of these imperatives applies in Ulster Bank’s case. They’re leaving altogether, so blowback is less of a worry, and a desire to be out of Ireland sooner rather than later is likely to outweigh maximising what it can make from branch sales. Industry sources expect Ulster Bank to have the bulk of its branch network up for sale by the end of the year. An Ulster Bank spokeswoman declined to comment on the company’s plans for its property portfolio.

Can anything be done to slow down branch closures in general? It is set to become somewhat harder to close a raft of them than it is in other territories. Indeed, AIB’s rollback of plans to drop cash services last year may encourage the so-called pillar banks to keep more branches open than they would ordinarily plan to, says Sheridan, given the scale of the adverse reaction to AIB’s plan at the time.

Among the banking review recommendations: lenders will need to submit assessments approved by their boards to the Central Bank before closing any branches, while the notice period for closing will be increased from two to six months. Lenders would have to give four months’ notice for withdrawing cash services, compared with one month currently.

The remaining banks are adamant that just because a branch is closing, that doesn’t mean they are withdrawing from the community altogether

The future of in-person banking is not just an Irish problem. In the UK, HSBC is closing about a quarter of its network this year. There, lenders have combined to provide banking hubs in areas where there is no stand-alone branch any more. At the hub, staff from several different banks are present on specific days of the week to provide service. The possibility of similar hubs opening here has been recommended by the banking review.

For its part, the Central Bank “expects all regulated entities to take a consumer-focused approach in respect of any decision that affects their customers”, it said in a statement. “Banks must also provide affected vulnerable customers with the assistance necessary to ensure that those customers can retain access to basic financial services.”

The remaining banks are adamant that just because a branch is closing, that doesn’t mean they are withdrawing from the community altogether.

“AIB remains committed to what is the largest branch network in Ireland,” says a spokesman, while pointing out that between its own branches and An Post, an AIB customer can access services at more than 1,000 locations across the State.

Bank of Ireland says it is investing €11.5 million in its branches this year “including extensive refurbishment and retrofitting”, a spokesman says. “Branches are still a very important part of how we serve our customers.”

An Post provides banking services for AIB and Bank of Ireland, which allows customers to carry out everyday banking transactions such as cash lodgements or withdrawals, as well as paying bills at any of the 910 post offices across the State.

“We have done that quite successfully, and we are willing and able to take more that comes our way,” says an An Post spokesman. “About 400 of our post offices are in areas where there is no local bank, and our strength is our presence in the community.”

Credit unions have been given greater powers to help fill the gap left by the departing banks. They have been able to offer mortgages since 2020, and writing in this newspaper on Monday, Irish League of Credit Unions chief executive David Malone highlighted that there are now more credit union offices nationwide than branches of AIB, Bank of Ireland, and Permanent TSB combined.

Then there’s the nonbank sector, with companies such as Finance Ireland rapidly increasing mortgage lending over the past few years, among other products.

Yet doubts remain if the An Post arrangement will be sustainable in its current form for the long term, while there are few signs so far that credit unions will fill the gap left by the departing banks.

The post office lost €37.9 million during the pandemic-hit year of 2021, its most recent available accounts. And it, too, has been closing outlets in recent years. Beyond whether its own branch network will remain intact, there are practical questions about the ability of a small community post office with one or two staff to handle anything beyond basic banking business.

“The concern is ... the capacity to deal with the volume in terms of the scale of transactions,” says O’Connell. “Think of taking in large amounts of €40,000 and so forth. That’s grist to the mill in a bank branch, but it’s a bigger challenge when you’re in the post office and people are queuing to get their pension and, and so forth.

“You can’t go into the post office and get a loan, you can’t negotiate your arrears – you need to be able to do those face to face,” he adds.

The long-term reality is that the absolute level of cash in the economy is falling, and with digital payments now accepted almost everywhere, that’s probably not going to reverse

— Diarmaid Sheridan, Davy Stockbrokers analyst

Credit unions have as much as €2.1 billion of unused lending capacity, according to the Central Bank. The sector’s loan-to-asset ratio, at 28.4 per cent, is little more than half what is usually seen as ideal.

For its part, the nonbank sector has been hammered by the increase in interest rates over the past 10 months, which have forced up their own borrowing costs dramatically. Those increases have in turn been passed on to consumers, making them less competitive in attracting borrowing customers.

Still, those are the solutions in place for now, and nobody in banking seriously believes the two largest lenders will increase their network in the future.

“The long-term reality is that the absolute level of cash in the economy is falling, and with digital payments now accepted almost everywhere, that’s probably not going to reverse,” says Sheridan. “That means one of the core necessities for maintaining a branch is becoming less compelling for the banks.”