Inheritances, which average close to €100,000 in the State, are the key way in which wealth is passed between generations. New data from the Central Statistics Office (CSO) casts a fascinating light on this and its role in how wealth is divided in society – which is much more unequal than income. This will again raise questions about the taxation of wealth and of inheritances themselves, one of the touchiest subjects for Irish politicians in the arena of tax.

1. The data

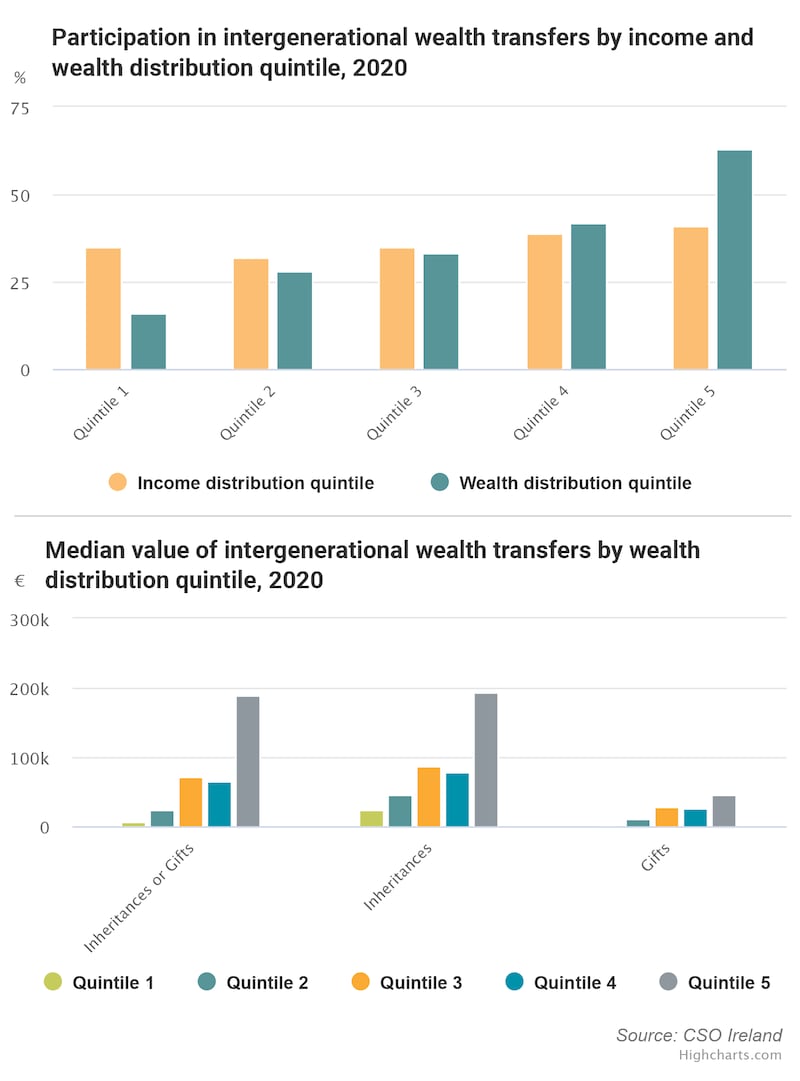

Some 36 per cent of households have received a gift or inheritance at some time, according to the new CSO figures – 30 per cent received an inheritance and 9 per cent a gift, with a small crossover of households who received both. The median value of all gifts and inheritances was €80,200, while for inheritances alone the figure was €99,200. Of households that received intergenerational transfers – inheritances or gifts – 57 per cent received money, 23 per cent inherited their home and 19 per cent got land.

Unsurprisingly, older households are much more likely to have received an inheritance – inheriting from parents accounts for 70 per cent of the total, and as lifespans extend, inheritances are received later in the life of the recipient. Not far off half the households in the 55- to 64-year-old age group received an inheritance compared to just over one quarter of those where the reference person in the house is aged under 35. And the average inheritance value for homeowners was much higher for older people. Meanwhile, homeowners were twice as likely as renters to have received an inheritance.

Not surprisingly, better-off households are much more likely to have received an inheritance – almost two thirds of the wealthiest 20 per cent of households have received an inheritance or gift, while this falls to just 16 per cent of the poorest group. Strikingly, the existing net wealth of households which had received an inheritance was €334,100, compared to €133,100 for those who had not. So, it is a case of the rich getting richer.

READ MORE

2. Wealth inequality

As the Commission on Taxation report pointed out, inequality in wealth in the Republic is much greater than income inequality, particularly after Ireland’s tax and welfare system redistributes income. Greater wealth inequality compared to income is typical internationally. In the State, the Commission quotes CSO figures showing that the top 10 per cent of households had wealth of at least €788.400, while the bottom 10 per cent had net wealth of lower than €600. Central Bank data shows the net wealth of Irish households now exceeds €1 trillion, boosted in recent years by rising property prices, lower debt and also a general rise in the price of other assets in the period of low interest rates which stretched from after the financial crash up to recently.

While the data shows some ups and down between different groups, it does show the very richest – getting an increased share of wealth between 2013 and 2018. The Commission on Taxation points out that the “direction of travel” is generally that the share of wealth of the better off – the top 20 per cent – is increasing, while other groups are getting a lower share. A large number of households have benefited not only from higher house prices but also lower mortgage debt as many were hit hard by negative equity during the crash. Generally, wealth is linked to income – in other words the higher income households also tend to have higher wealth. But there are exceptions, such as households with lower incomes but a lot of built-up wealth.

The family home is the biggest source of wealth, followed by other land and property, with a rise in recent years in the holding of financial assets such as shares, particularly among better off households. The richest households have a much more diverse asset base. The better off are much more likely to own businesses, land, investment property and financial assets. The main family home is by far the biggest source of wealth for the middle income groups. The poorest sections of the community wealth-wise often do not own a house and what assets they have are in cash, vehicles and valuables.

A final piece of evidence put forward by the Commission is the big impact which an inheritance has on the position of a household, typically moving it sharply up the wealth ladder, or very sharply in the case of people inheriting businesses. In other words, inheritances are really powerful levers for lifetime wealth.

[ On the Money: Sign up for our new personal finance newsletterOpens in new window ]

3. Intergenerational equity

A significant issue now for Irish society is the increasing number of middle to lower income people who cannot afford to buy a property and thus risk entering their older years without the main asset which has been the bedrock of the Irish middle classes – the family home. In turn, their children will miss out on an inheritance. If rents were lower than mortgages, then a renting group would have the option to save and build up financial assets. However current Irish rent levels leave many with little spare income. This problem has been slowly building. The average age at which people buy a home is trending relentlessly higher – over 60 per cent of those born in the 1960s lived in a property they or their partner owned by the age of 30, while this has fallen to 32 per cent for those born in the 1980s. The risk now is that many will simply never be able to buy.

4. Taxing wealth

Taxing wealth is difficult and contentious. The commission report says that the number of OECD countries with specific taxes on wealth has fallen from 12 in 1990 to three by 2018. This is partly due to the difficulty in administering such taxes – what should be included is contentious. valuation can be difficult and the very richest often respond by moving wealth offshore. For all these reasons, the commission opted not to recommend this tax in the Republic, though it does call for other ways to significantly increase the take from inheritances, pointing out that the tax take from capital taxes here is generally low by international standards. Sinn Féin has supported a wealth tax in Ireland, at a rate of 1 per cent on net assets in excess of €1 million.

The commission recommends two main ways in which to increase tax on inheritances. One is to impose capital gains tax (CGT) on the uplift in value on assets held by a person who dies and passes them on in a will. This would be a major change in the tax system as currently this CGT gain is effectively wiped out for tax purposes when a person dies.

Post office quarrels / Drug dealing impacts city centre businesses

CEO of An Post David McRedmond joins Ciaran Hancock to discuss the ongoing row between An Post and the UK’s Post Office over the implementation of post-Brexit customs rules, which is resulting in thousands of online purchases being returned to British retailers. Later on, we hear from two Dublin city centre business owners, Stephen Kennedy of Copper+Straw cafe and Sean Crescenzi of Happy Endings restaurant. They speak about the impact that anti-social behaviour and drug dealing, in and around Aston Quay, is having on their businesses and the immediate and long-term solutions they would like to see implemented to address the issue.

In other words CGT would be levied on gains arising from the transfer of assets after a person’s death. So for example if a person had bought shares which had increased in value over the years, the gain would be subject to CGT on their death, as it would if they were still alive and had sold them. While there would be allowances in various areas – and there would be an offset in cases where capital acquisitions tax – generally known as inheritance tax – was also due, the commission believes this would lead to a more logical system.

The second key route the commission recommends to increase tax on inheritances is to reduce the tax-free allowance of €335,000 which currently applies to inheritances from parents to children or, in rare cases from children to parents. (Technically the figure is a lifetime limit, so earlier gifts also count.) The commission calls for this figure to be significantly reduced on equity grounds and to raise revenue, pointing to OECD guidelines that such reliefs should be limited.

It points out that €335,000 would be enough to put someone in the wealthiest 40 per cent of the population. Having such a high threshold is “inequitable and regressive”, it says. While it does not recommend a specific figure, it says it needs to be much closer to the next threshold down, which is €32,500 and applies to siblings, nieces and nephews. It also calls for special reliefs which apply to people inheriting farms or businesses to be sharply reduced.

These are hugely controversial political issues. The extent of wealth inequality and the need to raise new revenue in the years ahead call for change. The new CSO figures again show the concentration of wealth being perpetuated via inheritances. But this is not one which the political system will take on lightly.