Over the next eight weeks or so, thousands of people all over the country will be fleeing in search of some much-needed sunshine and relaxation. For many of us, a crucial part of preparing for a trip abroad is getting a travel insurance policy. It offers a sense of security and it can come good in the event of an unfortunate incident or illness on holiday.

However, too many of us hand over our cash without considering what we actually need it for. So if you’re in the market for a travel insurance policy this summer, here are six steps you can take to ensure you are well protected.

1 CHECK WHAT’S COVERED

So many of us buy travel insurance for peace of mind, but, unfortunately, not so many make the effort to actually read the policy and see what we’re covered for. Hence, it can be a disappointment when it becomes clear that we can’t claim for as much as we’d like.

While most people now take some form of a gadget on holiday, be it an ereader, a tablet or a smartphone, many may not be aware which of the above are covered.

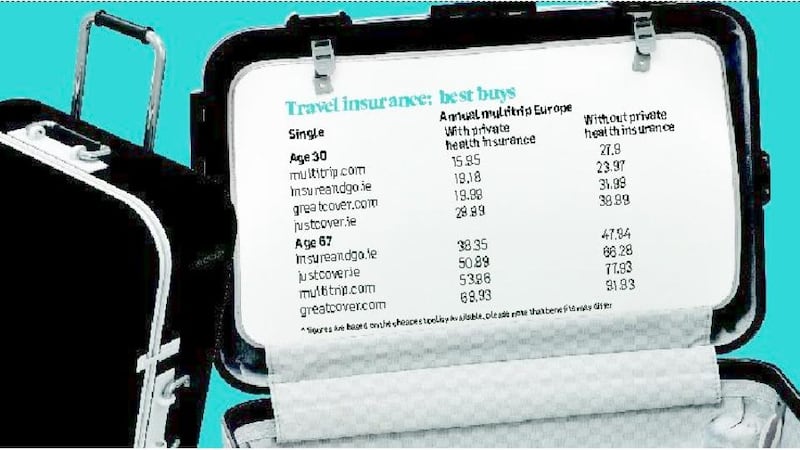

For example, according to Ciaran Mulligan, joint managing director of Multitrip.com, while iPads are covered under most travel insurance policies, mobile phones usually are not. This means that if you lose or damage your phone, or if it is stolen, you won’t be entitled to any compensation.

While some insurers are now offering mobile-phone cover as an add-on, it may be cheaper simply to take out an annual “gadget policy” if your mobile is a concern. These policies will typically cover you for between 90 and 180 days travel abroad.

But if you have such cover, don’t just leave your phone unattended on the beach while you head into the sea for a quick dip. It’s likely that in such circumstances an insurer won’t meet a claim. Policies often offer other quirks. Neither contact lenses nor spectacles, for example, are typically covered, though sunglasses are.

And if some of your goods are lost or stolen, Mulligan warns, you should get to a police station within 24 hours to report it. Any longer than that and the insurance company could consider it a fraudulent claim.

When you get to your hotel, if there is a safety deposit box, don’t ignore it, otherwise you may not be able to claim the cost of a stolen passport, for example.

“Make sure you use it, as insurers normally decline a claim on the basis that you just left it in the room,” says Mulligan, who also suggests you take a photo on your phone of your passport before heading abroad. In the event that it is lost or stolen, this should make it easier to get a new one issued.

Something else you might not be aware of is that policies typically cover you until you get to your “international point of departure”. Hence, if you’re getting a connecting flight from London to Los Angeles, your policy should cover you on the Dublin-London leg of the flight and onwards. However, should you then fly on from LA to Las Vegas, for example, and you miss a connecting flight, this won’t be covered under your policy.

2 MAKING A CANCELLATION CLAIM CAN BE TRICKY

Many of us buy travel insurance to cover us in the event that our plans change and we can’t go ahead with our holiday. However, we may not realise just how restrictive cancellation benefits are on many policies.

For example, with 123.ie, the insurer won't meet a claim for a cancellation caused by an illness or injury that you already knew about, or by the death of a relative that "you knew about and which could reasonably be expected to lead to a claim", or by you simply changing your mind about travelling.

Moreover, on its cheaper bronze policy, it offers no compensation for cancellation at all (though up to €7,000 is available on its gold policy). And remember, the cost of airport taxes isn’t usually covered under cancellation claims, so if your flight cost €150 but taxes accounted for a third of this, you may only be entitled to a refund of €100.

And hands up if you recognise this one. You’re booking an annual multitrip policy, but when do you pick the start date? The day you travel. This means that even if you have a valid reason for cancellation, you won’t be able to claim on it as the policy was not active at the time.

“If you forward-start an annual multitrip policy, you are not covered for cancellation until the start date of that policy,” says Mulligan.

3 STEP AROUND THE PRE-EXISTING TRAP

If you have an existing medical condition but already have private health insurance, getting travel insurance is a much simpler proposition, as your health insurer will cover the first part of the claim. This means that you may not have to go through a screening process.

If, however, you don't already have insurance, you will have to explain what your issues are. While the European Health Insurance Card (see below) offers protection when travelling in Europe, it won't cover the cost of sending you home, for example, so it's usually still advisable to get a travel policy.

If you have no health insurance and you’re looking to travel to the United States with a pre-existing condition, your policy may be expensive given the cost of healthcare in the US.

If you have a specific condition for which you’re finding it difficult to get cover, you could consider contacting a relevant charity, such as the Irish Heart Foundation or the Irish Cancer Society. They may be able to steer you in the right direction.

Also, Mulligan says, you should take out your travel insurance as soon as you book your holiday. While it will increase the costs, it won’t do so by a huge amount, and it will offer greater protection. For example, if you book a summer holiday in January but only take out travel insurance to start on the date you fly out, your policy won’t cover you if you develop an illness between January and your departure date.

4 DON’T LET YOUR AGE PUT YOU OFF

Some travel insurance providers won't insure you if you're older than 65, but there are plenty who still do. If you need more information about these, Age Action Ireland has compiled a list of insurers that offer cover for the older population.

However, if you recently moved into a higher age bracket, be aware that you'll likely have to pay more. With justcover.ie, for example, if you're aged between 18 and 65 you will pay €39.10 for an annual multitrip worldwide policy, including the US and Canada, provided that you have already have health insurance. This rises to €71.31 for a 66- to 69-year-old; €90.70 for a 70- to 75-year-old; and €126.40 if you're aged between 76 and 79.

While the insurer will consider claims for those aged 80 and over, through AllClear Travel Insurance, to get cover an applicant must complete an online screening; the maximum trip eligible for cover is 31 days.

Trailfinders says it charges double its regular premium for those aged between 66 and 69, and triple for those aged 70 to 75. It doesn’t offer cover for those aged 76 and upwards. Over-65s might also need private health insurance to get cover.

ACE 65+, for example, offers cover for those aged between 65 and 75. However, only those who have private medical insurance covering emergency medical expenses abroad are eligible for the product, and it can only be bought for a single trip covering 30 days. It also has strict exclusions regarding medical conditions: for example, to qualify you should not have had chemotherapy, radiotherapy, major surgery or a coronary artery bypass in the previous three months.

If you’re over 65 you will often find that the length of time a policy covers you for is restricted. With Insureandgo, to give a further example, if you are aged 66 to 86, you will only be covered for up to 31 days.

5 CHECK YOUR CREDIT CARD

If you have a credit card, you may find that this will cover the cost of your insurance, although this is a benefit that seems to be on the way out. For example, holders of Bank of Ireland’s Platinum Advantage Mastercard will automatically get fully comprehensive multitrip travel insurance when they pay for at least 50 per cent of their total fare with this card. So be sure.

6 AND FINALLY . . .

It’s free, it fits in your wallet, it gives you access to public health systems across the continent, and no one should travel without one this summer in Europe. Yes, it’s the European Health Insurance Card (EHIC).

The card gives you access to publicly available health services when travelling in the European Union or European Economic Area (Norway, Iceland and Liechtenstein as well as the EU states). With the accession of countries such as Croatia to the EU in recent years, the card can now be used in more countries than ever before.

In essence, the card means that, for example, if dental fillings are provided for free in the German public health system, you will be entitled to the same treatment while there.

The card lasts for two years, and you should receive it within about 10 days of applying, so if you haven’t done so yet, now is the time.

If you are stuck for time, your local health office can issue you with a temporary replacement certificate for a fast-approaching holiday.

If you already have a card, it can be renewed at hse.ie/eng/services/list/1/ schemes/EHIC/. This useful website also gives information on health schemes across Europe, and how you can make a claim.

If you need a doctor while you are travelling in France, for example, you're advised to find a GP who is conventionné. While you must pay the fee upfront, you will be entitled to claim some or all of this back – as well as the cost of your prescription – from the local sickness insurance office, Caisse Primaire d'Assurance Maladie (CPAM). Your reimbursement will be sent to your home address but may take about two months to arrive.

To help you navigate the local health systems, EHIC has created an app, which you can download via iTunes or Google Play, so take the time to download this before you travel.