With bumper corporation tax revenues and an election on the cards, Budget 2024 has all the ingredients for a giveaway day – enough perhaps even to rival those bountiful budgets in the run-up to the financial crash of 2008-2009.

Yes, it may be some months away but there has already been talk around an after-tax boost of €1,000 for middle-income earners, and discussions around the appropriateness or otherwise of spending our unexpected abundance.

Typically, economic theory suggests a countercyclical approach at a time of high growth and high inflation, where taxes are not cut as this could add further “heat” to an economy. However, a general election is looming – one must be held by March 2025 though expectations are that it could now be called earlier in the wake of a potential “budget bounce”.

As a result, pressure is growing for more substantial tax cuts and higher spending this autumn at a time when soaring food prices and generally rising costs have lower- and middle-income earners crying out for some relief.

READ MORE

“It’s going to be a budget aimed at putting a bit more money back into people’s pockets, a bit for everybody type of budget,” one tax expert says, adding that, as a result, “a little bit more” than the much-commented €1,000 figure may be given back.

So where might the cuts be?

Top tax rate

With a budget aimed at offering relief mainly to middle-income earners, reducing the burden of the top tax rate is likely to be a key target.

It has long been argued that, from an ‘Ireland Inc’ perspective, hitting the higher rate of income tax at a relatively low level of earnings isn’t the best optics when marketing Ireland as a location for global talent.

“We’re very much of the view that something needs to be done,” says Olive O’Donoghue, tax partner with KPMG, pointing to the fact that Ireland’s top rate is out of alignment with many countries with which Ireland competes for the same investment and talent.

For PAYE workers, the top rate of income tax is currently 52 per cent, including the universal social charge and PRSI. If you’re self-employed, or a landlord, etc, that can rise to 55 per cent due to a 3 per cent USC surcharge. Workers hit the top 40 per cent rate at a relatively modest level of earnings – €40,000.

In the UK, the 40 per cent rate doesn’t kick in until a worker hits earnings of £50,271 a year (€58,898), while in the United States you would need to earn $539,901 or more to pay tax at the top federal rate of 37 per cent. “It’s very out of kilter,” says O’Donoghue.

As she notes, someone earning €40,000 today will give up €48.50 in tax on every extra €100 they earn, adding that such a high rate can be a disincentive to seeking promotion.

As part of any potential reform, O’Donoghue would like to see a mandatory move on indexation “across all areas of tax, and not just personal tax”. This would see tax bands rise in line with inflation on an annual basis. “We would be strong advocates for ensuring inflation is removed from the tax system,” she says.

A recent report from the OECD on income taxes showed that 17 of the 38 OECD countries already automatically adjust personal income tax systems in line with inflation. The report also highlighted that low-income households with children are most vulnerable to increases in their effective tax rates when tax and benefit systems are not fully adjusted for inflation, as is the case in Ireland.

Such a move would be expensive but it would keep take-home earnings in line with inflation; otherwise it is hard to see how proposed tax cuts would be actual tax cuts, given the levels of inflation seen in the economy of late.

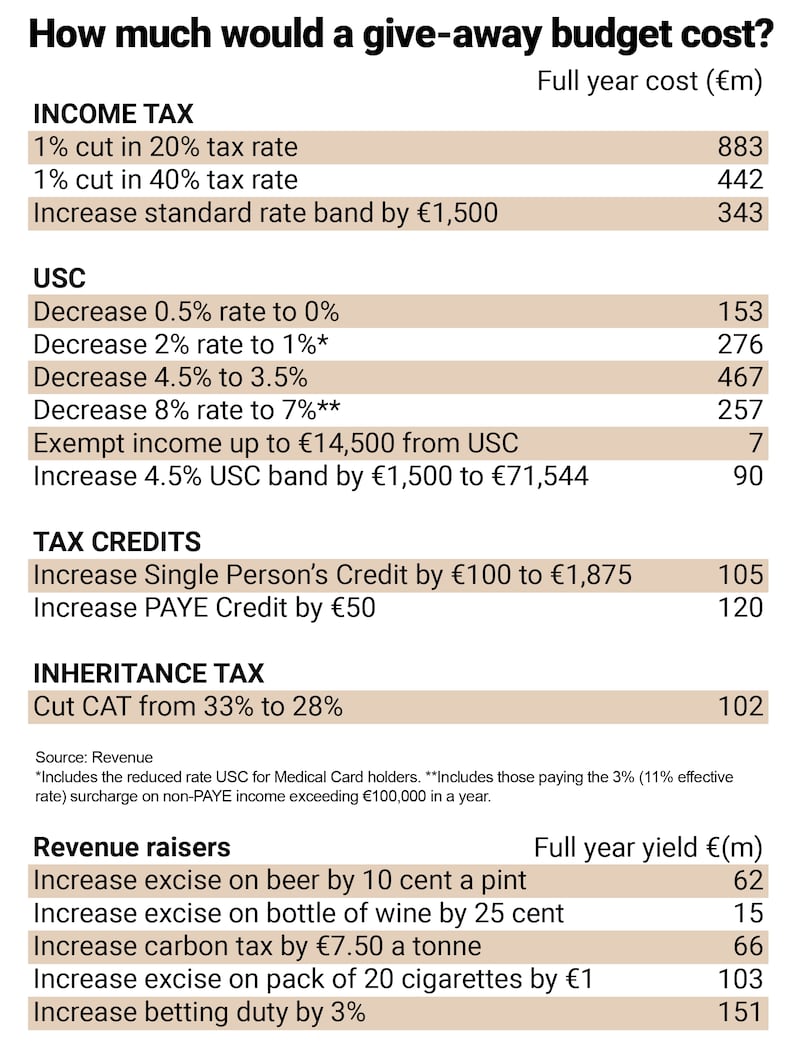

According to costings prepared by Revenue, allowing people to pay tax at 20 per cent on an additional €1,500 of earnings would cost about €343 million a year, while cutting the 40 per cent rate of tax to 39 per cent would cost €442 million a year.

Third tax rate

With average earnings now at about €52,000, an alternative approach to shifting the standard-rate tax band upwards would be to introduce a third rate of tax, at 30 per cent, a sort of a halfway house in terms of costs to the exchequer.

It would mean that those earning average incomes wouldn’t face the top rate of tax and it would make the system more progressive, as people would take longer to get into the top rate of income tax.

As one tax expert notes, however, it would be a logistical challenge to introduce because it would impact every payroll in the State. Not an insurmountable task, perhaps, but it would be a bigger change than just tinkering with the bands.

O’Donoghue agrees, adding that so many tax provisions are connected to the marginal rate of tax, including pension tax relief etc. A new rate of tax would require a significant overhaul.

USC cuts

Once a temporary tax – as income tax originally was way back when, it is now widely accepted that the universal social charge (USC) is here to stay. It may have a name change or be amalgamated into overall income tax at some point, but the charge, which is levied at rates from 0.5 per cent to 11 per cent, simply brings in too much money to be abolished altogether.

Figures for last year show that the Revenue Commissioners collected some €4.9 billion in USC – or about 16 per cent of total income tax returns. Getting rid of it would require generating a similar amount of tax revenue elsewhere – and even the bumper corporation tax receipts are unlikely, or unsustainable enough, to be able to do that.

A more likely outcome is that the burden of USC may fall.

The first option here would be to cut the rates at which USC is charged. At present, the USC band starts at 0.5 per cent on income of up to €12,012, and 2 per cent on subsequent earnings up to €22,920, rising to 11 per cent on self-employed income over €100,000.

Doing so would be expensive however. If the 4.5 per cent rate, which applies on income of between €22,920.01 to €70,044, and is therefore levied on the so-called middle-income earners, was to be cut back to 3.5 per cent, the annual cost would be almost half a billion euro, according to Revenue estimates. A hefty sum.

A cheaper approach – which wouldn’t give as much back, perhaps – would be to widen the bands. Increasing the aforementioned 4.5 per cent band, for example, by €1,500 to push it up to €71,544, would cost a little less than €100 million a year.

Getting rid of the 3 per cent surcharge for higher self-employed income might be another move. “We would want to see abolition of the 3 per cent surcharge, [it’s] only rational. We would just like to see that removed‚” says O’Donoghue.

Other tax cuts

There may also be increases to the PAYE and personal tax credits. Increasing the PAYE tax credit by €50 to €1,825 would cost about €120 million in a full year, for example.

O’Donoghue would also like to see mortgage interest relief reintroduced to try to “increase [the] ability of younger people to buy houses”; tax relief introduced for childcare; and the rent credit extended on an indefinite basis.

When it comes to inheritance tax, there could also be a widening of the tax-free threshold. At present, children can inherit €335,000 tax free from their parents; but there is a fear that this may not be enough to cover the cost of a typical family home, depending on how many children there are. It’s a long way off from 2009, when the parent-to-child threshold stood at more than €540,000.